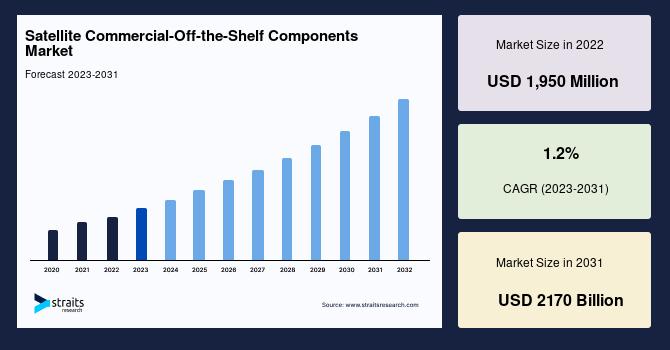

衛星商業-オフの部品の市場規模に達すUSドル、総額2,170百万円による2031によるコスト効率の高いスペースの製造

Causes |

2026-04-24 10:48:55

PW Consulting today publishes its definitive market study, Electronic Grade Adhesives Market: Strategic Roadmap 2026–2032. Built from five years of historical tracking and an actionable forward-looking framework, the report synthesizes market evolution through a 2025 base year and delivers a data-driven forecast that matters for boardrooms planning for 2026 and beyond. At the macro level, the global market reached roughly USD 6.38 billion in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of about 6.32% through the 2026–2032 horizon, reaching approximately USD 9.8 billion by 2032. That trajectory creates a clear, time-bound set of choices for materials suppliers, electronic OEMs, and private capital.

Electronic Grade Adhesives Market

Accelerated product complexity: Miniaturization, heterogeneous integration and higher thermal-power densities are compressing development cycles and elevating material performance requirements.

Electronic Grade Adhesives Market

Cost and supply volatility: Raw-material cost swings and regulatory pressure are creating margin risk for formulators and pricing risk for manufacturers—actions taken in 2026 will determine competitive position into the next decade.

Electronic Grade Adhesives Market

Selective consolidation: The adhesive market exhibits measurable concentration at the top, yet ample white space for specialist players; strategic M&A, partnerships and focused investment can be highly accretive.

Compliance as product strategy: Regulatory shifts are no longer compliance-only concerns; they are catalysts for product repositioning and value-capture through low-impurity, halogen‑free, and REACH-aligned formulations.

Executive dashboard: Single-page KPIs showing market trajectory, scenario outcomes and a quick-read heat map for supply risk and demand drivers.

Scenario modeling suite: Three rigor-tested demand and margin scenarios (baseline, upside, stress) with embedded sensitivity levers for raw-material inflation, duty regimes and volume shifts—suitable for immediate board-level use.

Supplier and technology scorecards: Comparative matrices evaluating scale, technical competence, innovation roadmap, geographic footprint and time-to-qualify for electronics OEMs.

Commercial playbooks: Pricing strategies, contract clauses for pass-through and hedging templates, and channel segmentation approaches for adhesives in high‑reliability electronics.

Regulatory & formulation tracker: Practical pathways for replacing SVHC-linked chemistries and for achieving region-specific compliance with minimal requalification burden.

M&A and investment filter: A prioritized list of capability-led targets, with LTV/IRR sensitivity and integration risk flags calibrated for the adhesives value chain.

Pilot-to-scale checklist: Process-replication guidance, test protocols and supplier qualification milestones to reduce NPI time and scrap risk.

The headline growth rate masks important structural dynamics. Demand is being driven by advanced semiconductor packaging, denser printed circuit board assemblies and a step-change in requirements from automotive and industrial electronics for thermal management and long-term reliability. At the same time, the production cost base is under pressure.

Epoxy resin feedstock showed renewed tightness in early 2026. Northeast Asia epoxy resin pricing moved higher (notably an increase from late‑2025 levels), reflecting firm demand in electrical laminates and electronics-related sectors together with higher bisphenol A and epichlorohydrin costs; Europe likewise experienced incremental feedstock cost pressure. These trends are amplified by geopolitical and logistics volatility, creating episodic input-price spikes that materially affect formulators with light inventories.

Regulatory drivers are equally consequential. The EU’s continued classification activity—most notably moves that push bisphenol A toward substance-of-very-high-concern status in certain use cases—has already accelerated reformulation programs across the industry. In parallel, trade determinations and tariff policy shifts in 2025 have altered sourcing economics for some resin lines, changing the calculus for footprint strategy and supplier contracts.

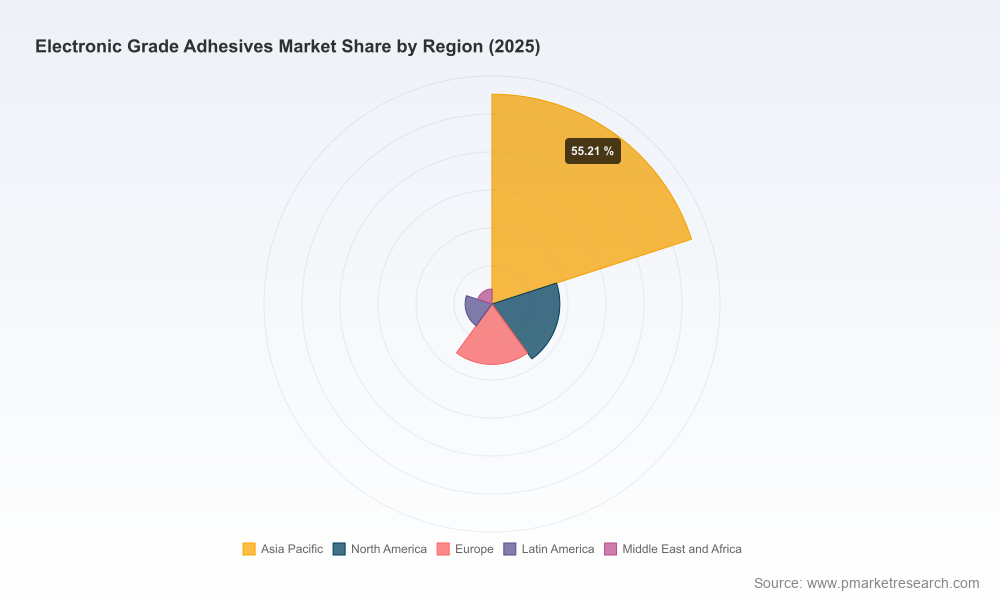

The market is served by a mix of global diversified chemical players, specialty formulators and agile, equipment-linked firms. Market concentration metrics show that top-tier groups control a material share of market volume, yet nearly half of the addressable demand remains outside the largest five suppliers—creating strategic opportunity for focused innovators.

Henkel: A leader in underfills, die attach and thermal materials, Henkel’s expanded application engineering labs and recent capacity investments signal a play for high‑reliability and EV-related thermal management growth.

3M: Strength in structural and fast-cure chemistries positions 3M to capture miniaturization and automated assembly benefits—its channel partnerships extend commercial reach into precision assembly segments.

Dow, Momentive, Shin‑Etsu and Wacker: Silicone and thermally conductive specialists who are leveraging primerless and low‑VOC formulations to target harsh‑environment and optically sensitive applications.

H.B. Fuller and Sika: Engineering-adjacent players increasingly combining adhesive chemistry with systems integration for automotive and industrial electronics.

Dymax, DELO and other light‑cure innovators: Fast‑curing solutions with low outgassing are becoming essential for high-volume, high-density assembly lines.

Regional semiconductor materials specialists (e.g., YINCAE, NAMICS): Focused on underfill, liquid encapsulants and die attach systems that meet the fine‑pitch, thermal and reliability needs of advanced packaging.

Recent corporate moves underscore these strategic options: expansions of application and manufacturing capacity, a new R&D facility focused on next‑generation packaging, and distribution partnerships accelerating adoption of optimized one‑part epoxies. Taken together, these actions illustrate how leading players are converting technical differentiation into commercial scale.

Lock in raw‑material strategy now. Use blended procurement (spot + contract), indexed pass‑through mechanisms, and local buffer inventories to dampen price shocks. Prepare dual‑sourcing for critical resin streams and quantify the cost of qualification delays.

Prioritize formulation roadmaps for compliance and differentiation. Move early on halogen‑free and low‑impurity epoxy chemistries where regulation is tightening—early movers reduce downstream requalification costs and secure OEM preferred‑supplier status.

Invest selectively in application engineering. Shorten qualification cycles by deploying local process replication labs and co‑development pilots inside key customer locations; this has outsized returns when winning design‑in at the PCB and packaging level.

Pursue capability-led M&A and partnerships. Targets should be evaluated against time-to-market for high-reliability adhesives, IP on thermal/ conductive chemistry, and channels into high-growth end markets. Integration plans must prioritize supplier continuity and customer requalification roadmaps.

This report is deliberately calibrated to move executives from insight to execution. Beyond the executive summary and market forecast, clients receive bespoke modules that can be adopted immediately:

Commercial simulation packs that model margin under alternate raw‑material and tariff scenarios.

Supplier scorecards and negotiation playbooks to reduce qualification timelines and secure long‑term supply at predictable cost.

Regulatory impact maps with step-by-step reformulation pathways and recommended test protocols to meet REACH and regional registration needs.

M&A diligence templates and integration checklists specifically tuned to adhesives and electronic materials assets.

Importantly, the report adheres to a “trailer” principle: it provides the analytical backbone and executable tools needed for 2026 decision-making while preserving proprietary segment-level tables and customer-by-end-market data for subscribers. That balance ensures senior teams can quickly understand strategic levers and then access the full data set to operationalize decisions.

For materials manufacturers, the immediate task is to stress-test product roadmaps against the report’s scenarios and to finalize procurement hedges before Q3 procurement cycles. For OEMs, the priority is to engage application engineering partners and accelerate joint‑qualification programs with suppliers that have both technical depth and scale. For investors, the landscape favors buy-and-build strategies focused on niche, high‑value adhesive chemistries and application engineering capabilities.

PW Consulting is offering tailored briefings and scenario workshops for C-suite and investment committees through Q3 2026. To request a tailored executive briefing or to review the full dataset and segment-level analytics, please visit our report landing page or contact our advisory team for an engagement proposal.

For detailed analysis of this topic, please visit the official page:Electronic Grade Adhesives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com