Budesonide Inhaler Market: Trends and Growth Opportunities

Other |

2026-03-25 07:51:12

As governments, industrial players and agricultural stakeholders sharpen their focus on low-emission biomass processing, the market for environmentally friendly carbonization furnaces is moving from niche innovation to mainstream industrial deployment. Our market model shows robust expansion through the forecast horizon (2026–2032), driven by accelerating demand for biochar and low-emission charcoal products, tighter environmental requirements in Europe and North America, and continued capacity growth in Asia‑Pacific. The global market, measured in USD million, is positioned to grow from the 2025 base to a materially larger market by 2032 at a compound annual growth rate (CAGR) of 10.25% — a trajectory that compels executive teams to reassess capital plans, technology roadmaps, and go‑to‑market strategies ahead of 2026 budget cycles.

Environmentally Friendly Carbonization Furnace Market

Timing of investment: With a double‑digit CAGR baked into our central case, organizations that delay modernization or scaling risk paying a premium for equipment and feedstock access as demand commoditizes.

Environmentally Friendly Carbonization Furnace Market

Regulatory alignment as competitive advantage: Evolving emission standards in major markets increasingly reward enclosed, low‑emission carbonization designs that incorporate advanced thermal management and emission controls. Compliance is shifting from cost center to market access requirement.

Environmentally Friendly Carbonization Furnace Market

Product diversification and value capture: Biochar use cases — from soil amendment to water treatment and industrial carbon inputs — are expanding. Companies that secure offtake channels and tailor furnace capabilities for specific product specifications capture more margin across the value chain.

Geographic feedstock dynamics: Abundant agricultural and forestry residues in certain regions create pockets of competitive processing economics. Strategic planning must balance proximity to feedstock, labor, and export logistics against regulatory and offtake considerations.

Consolidation and strategic assets: Market concentration metrics indicate a market that is not highly concentrated at present but trending toward selective consolidation — creating strategic opportunities for acquisitive players to secure IP, capacity and long‑term offtake agreements.

This PW Consulting study is structured to serve executives and deal teams making 2026 investment and operational decisions. The full report provides:

A transparent market model (historical 2020–2025, forecast 2026–2032) with scenario outputs for conservative, central and accelerated adoption paths;

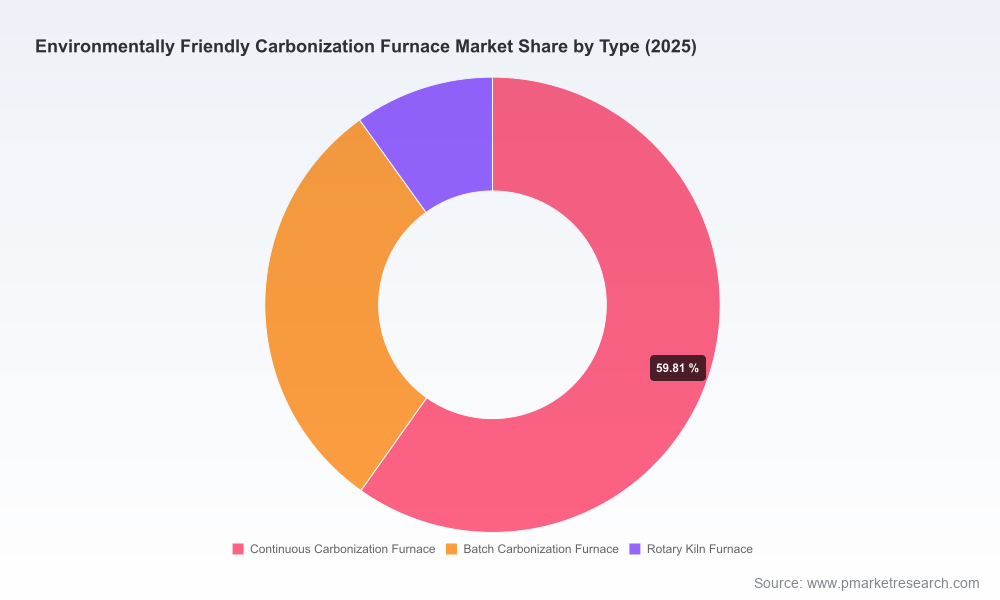

CapEx and OpEx benchmarking for typical continuous, batch and rotary kiln configurations, with sensitivities tied to feedstock moisture, throughput and product yield;

Technology scorecards comparing thermal efficiency, emissions profile, modularity and automation readiness across leading and emergent designs;

A regulatory and permitting matrix aligned to major markets, showing time, cost and technical controls required to achieve compliance;

Supply‑chain maps and vendor shortlists constructed for three strategic profiles: modular on‑farm deployments, industrial scale processors, and mixed asset integrators;

Commercial diligence tools including sample offtake contract templates, carbon accounting methodologies and a 24‑month project commissioning checklist;

Playbooks for M&A and partnership screening, including practical red flags and integration considerations for acquiring technology or production assets.

Note: This summary intentionally highlights the types of practical deliverables and strategic value contained in the full report. Detailed segment tables, regional splits and vendor financials are reserved for subscribers and purchasers of the complete dataset.

The competitive dynamics are evolving along three vectors: product evolution and automation, asset consolidation, and niche specialization for specific feedstocks and end‑markets.

Product evolution and automation: European firms with cross‑regional facilities have invested in upgraded continuous systems that emphasize thermal control and product consistency. Recent announcements in 2026 reflect a step change in automation (advanced control suites) that improve thermal efficiency and reduce operator dependency — an important differentiator for buyers seeking predictable quality and low emissions.

Scale via strategic asset plays: North American technology operators focused on high‑temperature pyrolysis and biocarbon are actively acquiring industrial assets to secure scale and long‑term offtake. These transactions reveal a trend: ownership of integrated processing facilities accelerates route‑to‑market for higher‑value biocarbon products and specialist remediation services.

Field and modular solutions: US and China‑based suppliers continue to commercialize compact, on‑site kilns for decentralized biochar production targeted at agricultural customers and small industry, preserving a market for lower‑CAPEX, rapid‑deployment solutions.

For executives, the practical takeaway is threefold: (1) prioritize capital toward systems that demonstrably meet future emission tests and produce consistent product quality; (2) evaluate M&A targets not only for capacity but for offtake and IP; (3) maintain flexibility between modular deployments and larger centralized facilities depending on feedstock logistics and product end‑markets.

Major equipment re‑engineering and automation upgrades announced in 2026 by leading European equipment providers signal that buyers will increasingly evaluate software and control packages, not just mechanical design.

Acquisitions of biocarbon facilities and IP in 2026 by North American technology firms demonstrate the premium placed on immediate production capability and long‑term offtake — useful precedent for companies considering inorganic growth to accelerate market entry.

Pilots combining high‑temperature pyrolysis with environmental remediation (e.g., PFAS remediation pilots) indicate emerging two‑play commercial models where environmental services and biocarbon production can be co‑monetized.

Re‑score your technology stack against emissions performance and automation capability; prioritize upgrades that shorten commissioning time and reduce operator risk.

Model multiple feedstock scenarios (local, regional, imported) and stress‑test project IRR to moisture, logistics and yield sensitivities.

Pursue strategic M&A or offtake partnerships to secure market access and accelerate scale — prioritize assets with proven permits and long‑term offtake frameworks.

Embed a regulatory compliance roadmap into every project timeline — approvals and emissions testing can dictate project cadence and cost.

Run pilot projects for higher‑value product lines (e.g., engineered biochar, high‑temperature biocarbon) to validate product spec and commercial channels before full‑scale CAPEX.

Negotiate supplier contracts that align equipment warranties with measured emissions and product quality KPIs; include performance incentives.

Establish a carbon accounting and verification process early; credible third‑party verification materially enhances offtake pricing and grant eligibility.

Maintain strategic optionality — design plants and contracts that allow capacity scaling or modular redeployment as market dynamics evolve.

This briefing is designed as a strategic preview. PW Consulting’s complete Environmentally Friendly Carbonization Furnace Market report includes the granular regional and application splits, vendor scorecards, sensitivity‑tested financial models and downloadable scenario calculators that corporate development, strategy and procurement teams require for execution. Those granular segment tables and company‑level financials are not reproduced here to preserve the commercial value of the full deliverable.

To obtain the comprehensive dataset, model files and a tailored executive briefing, visit PW Consulting’s report page or contact our industry team. For 2026 planning cycles, teams that pair these market insights with disciplined technical diligence and rapid pilots will be best placed to convert market growth into sustainable commercial advantage.

For detailed analysis of this topic, please visit the official page:Environmentally Friendly Carbonization Furnace Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com