Fresh Pears Market Analysis: Global Trends and Growth Opportunities

Food |

2026-05-08 06:56:29

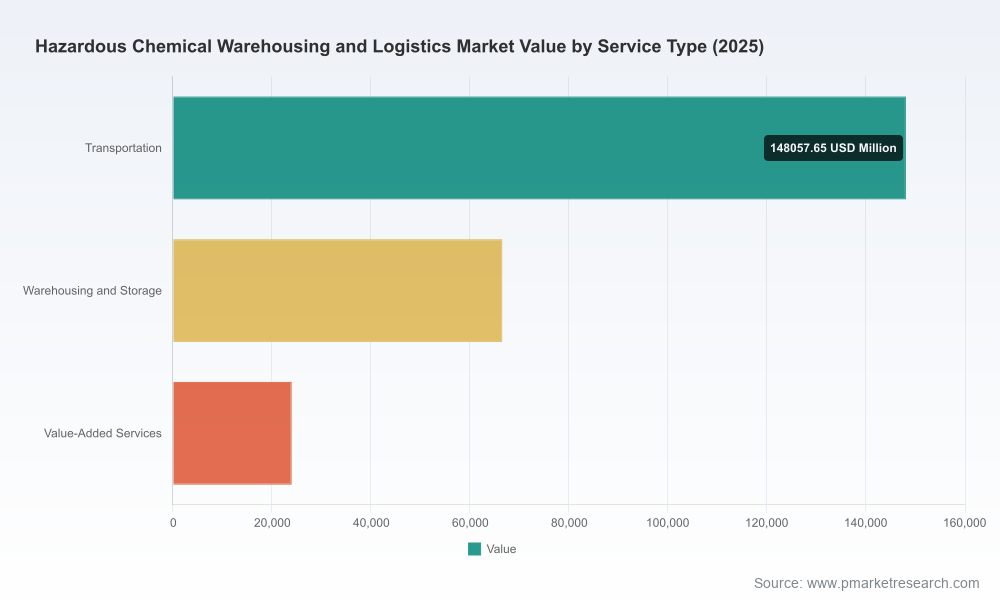

PW Consulting today releases a strategic preview of our full market study on Hazardous Chemical Warehousing and Logistics, designed to inform executive decision-making as companies plan budgets, compliance programs, and network investments for 2026. Our analysis synthesizes macroeconomic trajectories, regulatory inflection points, competitive moves and operational playbooks into a single, actionable advisory. The market is sizable and growing: after reaching approximately USD 238,525 Million in 2025, our model projects a compound annual growth rate of 6.12% across the 2026–2032 forecast window, with the total market approaching USD 361,506 Million by 2032. For executives weighing capacity investments or strategic partnerships, the timing could not be more consequential.

Hazardous Chemical Warehousing And Logistics Market

Regulatory convergence and updates. Multiple international and national regulations updated their rules effective January 2026 and are driving immediate operational changes. Notable items include the IATA Dangerous Goods Regulations (67th edition), IMDG Code amendments, and a fully operative ADR cycle for road transport across Europe. U.S. rulemaking and OSHA updates are also aligning workplace requirements with international practices. These changes increase the compliance burden on warehousing and multi-modal transport providers and alter packaging, labeling and documentation workflows.

Hazardous Chemical Warehousing And Logistics Market

Technological acceleration in visibility and safety. Providers are rapidly deploying advanced tracking, telematics and safety analytics that enable real‑time monitoring of hazardous shipments — an operational capability becoming as important as physical capacity.

Hazardous Chemical Warehousing And Logistics Market

Market structure and investment signals. Industry participants are investing in low-carbon transport solutions, rail and tank-container capabilities, and specialized sample-fulfillment networks. Recent initiatives — including certified hydrogen fuel trucks for chemical transport, new ISO-tank rail services, acquisitions to broaden sample fulfilment networks, and launches of liquid chemical vessels — signal both competitive differentiation and modal diversification.

Our objective is to move clients from awareness to operational readiness. The full report is built as a management toolkit that goes beyond descriptive market sizing to provide practical modules you can apply to 2026 planning cycles:

Regulatory impact playbooks: concise, tiered checklists that translate new IATA/IMDG/ADR/OSHA provisions into site-level actions — from labeling templates to training syllabi and audit protocols.

CapEx and TCO models: scenario-driven investment templates for adding hazmat racks, bunded storage, tank capacity, or converted cold/hazard cells — including sensitivity to throughput, insurance, and regulatory inspection cycles.

Network-design heuristics: decision matrices for choosing between warehousing expansion versus outsourced partnerships, and for selecting modal mixes when rail/sea options become more attractive.

Operational blueprints: emergency response templates, supplier qualification scorecards for chemical carriers, sample-fulfillment SOPs, and a harmonized labeling/GS1 implementation guide.

Digitalization and safety KPIs: recommended telemetry, integration schemas for dangerous-goods data, and performance indicators tied to compliance outcomes and insurance impacts.

The hazardous chemical logistics market remains fragmented, offering opportunities for both global integrators and focused specialists. Our concentration analysis indicates a low top-tier concentration — the top three global providers capture roughly mid‑teens percentage of the market, and the top five account for under one‑quarter — a structure that sustains regional specialists and niche service providers alongside large global networks.

From an industry architecture perspective, three provider archetypes dominate strategic thinking:

Global integrators (supply chain platform players) that bundle compliance, multimodal transport, warehousing and digital tracking into an enterprise-grade offering. These firms leverage global footprints and compliance centers of excellence to serve multinational chemical producers.

Container and tank specialists that own or manage tank fleets, intermodal services and liquid-handling capabilities. Their advantages are in bulk liquid handling, tank-cleaning ecosystems and terminal-to-terminal logistics.

Regional and niche providers that compete on specialized services — hazardous sample fulfilment, pharma-grade hazard handling, temperature-controlled hazmat storage, and market-specific compliance expertise.

Key players across these archetypes are actively reshaping their offerings. Providers such as DHL Supply Chain, DB Schenker and Kuehne + Nagel continue to emphasize integrated hazardous logistics and global compliance services with real‑time tracking and multimodal solutions. Tank- and intermodal-focused companies like Bertschi and Hoyer are reinforcing liquid bulk capabilities, while specialist operators — including companies focused on hazardous sample fulfillment, temperature‑controlled hazardous storage, and chemical distribution logistics — are consolidating niche networks through acquisitions and targeted service launches.

Recent industry developments underscore these strategic moves. Notable examples include the launch of Europe's first ADR-certified hydrogen truck for chemical transport, new liquid-rail ISO-tank services, vessel deployments for liquid chemical transport, strategic acquisitions to expand sample‑fulfillment capabilities, and new tracking/safety technology introductions. These actions collectively point to three immediate industry trends: rapid regulatory-driven compliance deployment, modal diversification (rail/sea/road), and digital safety/visibility as a minimum competitive requirement.

Executives should view 2026 as a year to convert compliance and operational risk into strategic advantage. Key implications we counsel leaders to consider:

Turn compliance into a revenue differentiator. Being able to demonstrate turnkey compliance for complex shipping lanes — including newer items such as hydrogen-capable ADR vehicles and updated battery rules — will unlock premium customers and reduce cost overruns from incidents and delays.

Prioritize visibility investments. Real-time tracking and dangerous-goods telemetry reduce detention and claim costs, and materially improve incident response times. These tools should be evaluated not as cost centers but as insurance-reducing, margin-protecting investments.

Re-evaluate network modality. The combined effect of IMDG/rail service investments and regional cabotage constraints makes modal optimization a source of cost and carbon savings. Scenario planning with rail/sea options should be part of every 2026 network review.

Design capacity with flexibility. Invest in convertible storage cells and modular bunded areas that can be reconfigured as product mixes shift or as regulatory reclassification occurs.

Use M&A and partnerships to fill capability gaps. Bolt-ons for sample fulfilment, tank fleet access and regional compliance centers buy time and reduce greenfield risk.

Run a regulatory gap assessment mapped to your top 10 trade lanes and 20 highest-risk products.

Implement a telemetry pilot for hazardous shipments covering at least one multimodal corridor.

Develop a two-speed CapEx plan: urgent compliance fixes (Q1–Q2) and transformational investments (H2 onward).

Create a supplier qualification fast-track for tank and rail partners to accelerate modal shifting.

Audit insurance and incident-cost exposure; translate reductions from improved visibility into reinvestment budgets.

Design an emergency-response joint exercise program with carriers and port terminals.

Institute an ESG lens for hazmat operations — focusing on decarbonization of freight and safer storage practices to meet customer procurement demands.

Prepare commercial propositions that monetize compliance and visibility (e.g., premium guaranteed‑compliance lanes, SLA‑backed safety services).

The complete PW Consulting Hazardous Chemical Warehousing and Logistics report contains the full forecasting model, scenario analyses, vendor benchmarking matrices, operational templates and regulatory impact assessments referenced in this preview. Our work integrates proprietary demand forecasts, indemnity and insurance sensitivity analysis, and practical checklists that can be deployed immediately by operations and risk teams.

We deliberately present this preview as a strategic “trailer”: it demonstrates the depth and applicability of our analysis while reserving full segment-level detail, regional breakouts, and company-by-company revenue benchmarks for the full report and subscriber portal. That approach ensures you receive high-fidelity, actionable material when engaging with our analysts and access the sensitive segmentation and contractual intelligence necessary for contracting, bidding and capital allocation decisions.

For a briefing tailored to your portfolio or geography, contact PW Consulting to schedule a bespoke executive workshop. Our analysts can overlay your asset base and product mix onto the PW market model to produce a short-form strategic playbook within seven business days.

Download the full report and supporting toolkits to obtain the detailed segmentation, regional forecasts and company-level analyses necessary to finalize 2026 budgets and partnership decisions.

In an industry where compliance, safety and capacity interact with rapidly changing regulations and technology, 2026 will be a decisive year. PW Consulting’s study equips leaders with the market-scale perspective, operational templates and strategic options to turn regulatory challenge into competitive advantage. Visit our report page to access the full intelligence suite and speak with the authors about implications for your business.

For detailed analysis of this topic, please visit the official page:Hazardous Chemical Warehousing And Logistics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com