How Trade Promotion Management Software is Transforming Retail Strategies

Networking |

2026-07-13 09:47:54

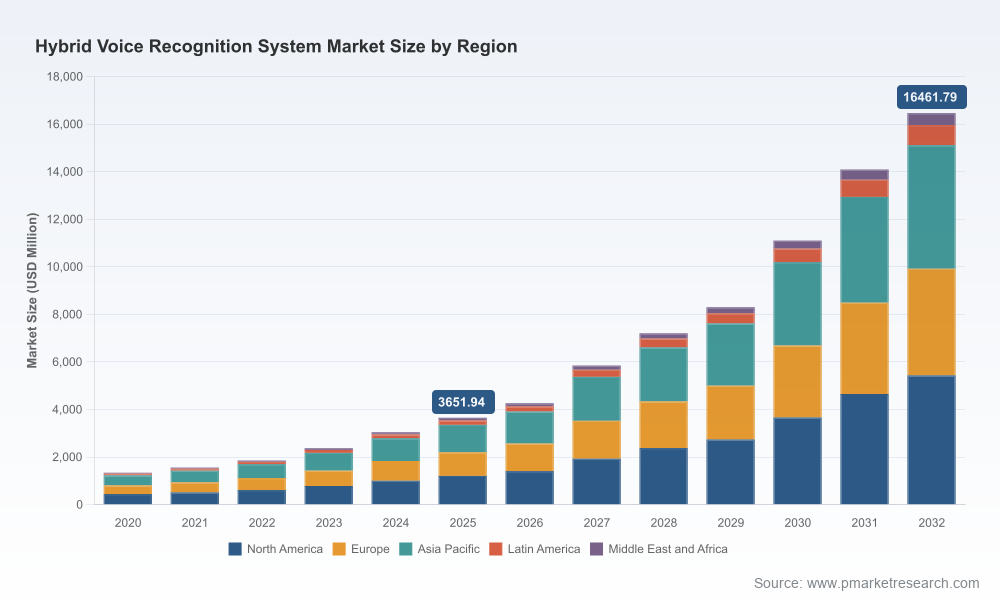

As organizations plan technology investments for 2026, Hybrid Voice Recognition has moved from a niche capability to a mission-critical platform class. PW Consulting's latest market study shows this transformation in clear numbers: the global Hybrid Voice Recognition System market grew from roughly USD 1.34 billion in 2020 to about USD 3.65 billion in 2025, and — sustaining a compound annual growth rate (CAGR) of approximately 23.95% over the 2026–2032 forecast window — is projected to exceed USD 16.46 billion by 2032. These macro dynamics create both urgency and opportunity for enterprises across regulated industries, mobility ecosystems, consumer technology, and the emerging IoT fabric.

Hybrid Voice Recognition System Market

Acceleration toward distributed inference. The market’s rapid expansion reflects a shift in architecture priorities: organizations are increasingly balancing cloud-scale intelligence with on-device and edge inference to meet latency, privacy, and resilience requirements.

Hybrid Voice Recognition System Market

Regulation as a feature, not a constraint. GDPR, HIPAA, and other compliance regimes already shape architectures for voice data. Companies that bake data governance, consent management, and certified security controls into hybrid deployments will gain a measurable commercial advantage.

Hybrid Voice Recognition System Market

Consolidation but not monopoly. Market concentration data indicate that leading vendors command a meaningful share of market value, yet there is room for specialized players to win in verticalized niches and regional ecosystems. This duality favors both platform partnerships and targeted M&A activity.

This report is designed as a decision-support tool for C-suite and line-of-business leaders evaluating voice AI strategies for 2026. It combines quantitative forecasting, qualitative competitive assessment, and executable playbooks — without exposing the raw segmentation tables in this communication. Key actionable elements include:

Investment-grade market sizing and trend analysis: historical performance, baseline 2025 metrics, and forward-looking projections through 2032 that allow CFOs to model total cost of ownership and ROI for hybrid voice programs.

Vendor positioning maps and capability matrices that identify winners by architecture, privacy posture, industry focus, and partner ecosystem — enabling procurement teams to shortlist candidates rapidly.

Deployment playbooks: reference architectures for cloud-edge integration, latency-sensitive in-vehicle systems, and privacy-preserving healthcare implementations, including data-flow diagrams, API considerations, and recommended vendor pairings.

Regulatory and security checklists aligned to GDPR, HIPAA, SOC 2 Type II, ISO 27001, and NIST AI RMF guidance — actionable items that reduce compliance friction during pilot-to-production transitions.

M&A and partnership due-diligence templates that assess technology lock-in, dataset portability, and model governance — tailored for private equity, corporate development, and strategic investment teams.

The hybrid voice recognition market reflects a mix of global cloud platforms, specialist vendors, and vertically focused incumbents. Our analysis highlights strategic postures rather than raw market shares, enabling enterprise buyers to match vendor capabilities to use-case risk profiles.

Large cloud platforms (Google, Microsoft, AWS): These providers offer deep neural-model scale, extensive language coverage, and integration into broader AI and data ecosystems. Their hybrid offerings emphasize cloud-native model updates combined with edge SDKs for latency and offline resilience — attractive for enterprises seeking broad multilingual support and managed operationalization.

Platform-specialists (Nuance, Cerence, SoundHound): Firms with focused stacks bring domain expertise — for example, automotive or clinical workflows — and often provide pre-trained models and integration bundles tailored to regulated environments. They are preferred where domain-specific accuracy and OEM / supplier relationships matter.

Regional and R&D-driven players (iFLYTEK, Baidu, Speechmatics): These vendors are strong where language-specific modeling, local data residency, or partnerships with telcos and device manufacturers are decisive. Their roadmaps often prioritize multilingual and domain-adapted models for high-growth markets.

Embedded and edge innovators (Sensory, SoundHound): Low-power, on-device inference capabilities enable voice UX in constrained environments — wearables, automotive clusters, and smart appliances — and are complementary to cloud-based analytics.

Enterprise analytics and workforce vendors (Verint, IBM): Emphasis here is on integrating voice recognition with customer engagement, transcription accuracy for compliance, and analytics pipelines that deliver operational insight.

Recent product and partnership moves validate these dynamics: early 2025 launches expanded cloud-edge platforms for automotive OEMs, a mid-2025 release targeted multilingual hybrid engines for healthcare deployments, and strategic partnerships with telecommunications operators are enabling 5G-enabled edge rollouts. For procurement teams, these signals point to a near-term premium on vendors that can demonstrate production-scale hybrid solutions and telco/edge partnerships.

Architecture trade-offs: hybrid solutions balance traditional DNN-based hybrid models and emerging end-to-end architectures. The practical choice is use-case driven — hybrid DNNs remain advantageous in low-resource and multilingual contexts where modular adaptation is required; end-to-end models can yield higher accuracy in well-resourced, closed-domain settings.

Model governance: enterprises must operationalize version control, bias monitoring, and dataset lineage for voice models. We map MLOps patterns specific to hybrid stacks in the report, including edge model deployment strategies and rollback mechanisms for safety-critical contexts.

Security and privacy by design: compliance with GDPR and HIPAA is not optional. The market favors vendors able to demonstrate SOC 2 Type II or ISO 27001 certifications and clear approaches to consent capture, data minimization, and on-device anonymization.

Start with risk-tiered pilots. Segment use cases by latency sensitivity, privacy exposure, and model adaptability. Deploy minimal-viable hybrid pilots in each risk tier to validate architecture choices before scaling.

Prioritize vendors that can show production references in your sector and provide modular deployment options (cloud-only, edge-only, or hybrid) to avoid lock-in.

Embed compliance and security gates into procurement. Require explicit documentation of data residency, consent flows, and third-party audits as part of RFPs.

Invest in a small internal center of excellence for voice AI. Over 2026 you will centralize model governance, dataset labeling, and a partner integration function to accelerate time-to-value.

Explore telco and 5G edge partnerships where low-latency and localized processing materially change the customer experience — our report highlights when and where this pattern matters.

Rapid growth does not eliminate risk. Material pitfalls include over-reliance on single-vendor models, underestimating data governance complexity, and misaligning architectural choices with operational constraints (e.g., firmware update cycles in automotive). Mitigations include multi-vendor pilots, contractual rights for model portability, and staged rollout plans linked to compliance milestones.

Board-level briefings: use the market trajectory and concentration analysis to frame capital allocation decisions and justify strategic hiring into AI/edge engineering roles.

Procurement and RFPs: adopt the vendor assessment framework and security checklist to reduce procurement cycle time and align SLAs to business outcomes.

Business case modeling: use the forecasted growth profile and scenario-driven sensitivities to stress-test revenue and cost assumptions for multilingual, regulated, or mobility-centric programs.

This briefing outlines the strategic contours you need for 2026 decisions. The full PW Consulting market report contains the segment-level forecasts, regional and application breakdowns, vendor scorecards, and downloadable datasets that operational teams and investors will require to execute. To access the complete dataset, detailed methodology, and vendor benchmark matrices, please consult the full report on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Hybrid Voice Recognition System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com