Polymer Modifiers Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-15 04:08:32

PW Consulting’s latest Polyelectrolyte Market report—built on a verified historical window (2020–2025) and a forward-looking forecast period (2026–2032)—translates granular industry signals into pragmatic strategy for executives planning in 2026. The global market is estimated at USD 3,450.0 Million in our 2025 base year and, under current demand and supply dynamics, is projected to expand to approximately USD 4,952.42 Million by 2032 at a compound annual growth rate (CAGR) of 5.31% over the 2026–2032 forecast horizon. This briefing highlights the report’s strategic value while preserving the proprietary segmentation detail reserved for subscribers.

Polyelectrolyte Market

Actionable foresight: The 2026 planning cycle is being driven by capital allocation decisions—capacity investments, procurement contracts, and M&A—that must account for medium-term market growth, raw-material exposure, and tightening regulation. Our market sizing and 7-year forecast deliver the demand envelope executives need to stress-test these decisions.

Polyelectrolyte Market

Risk calibration: Polyelectrolyte economics are tightly coupled to polymer feedstock and energy markets. The report quantifies this exposure and models scenarios to quantify margin sensitivity to feedstock volatility, helping procurement and finance teams set hedging and sourcing strategies.

Polyelectrolyte Market

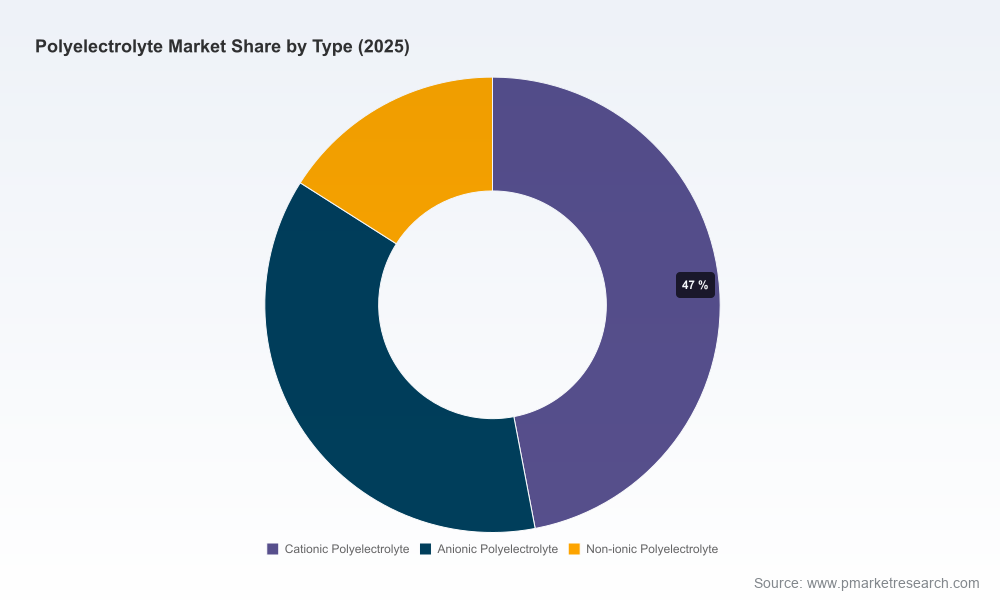

Competitive positioning: With market concentration measured at CR3 = 34.8% and CR5 = 47.5%, the sector is neither a pure monopoly nor atomized. That structure favors differentiated product plays, selective capacity consolidation, and regional partnerships—insights that are unpacked in the competitive chapter.

Regulatory & sustainability implications: Stricter wastewater discharge and chemical safety regulation are accelerating demand for higher-performance chemistries. The report maps regulatory pressure points by application and highlights where product reformulation and compliance investments will deliver ROI.

Across end uses—industrial water treatment, pulp & paper, mining, oil & gas and specialty life‑science segments—the need for reliable flocculation, coagulation and sludge-management chemistries remains the primary growth engine. However, 2025 produced mixed signals: demand softness in certain commodity cycles coincided with new capacity coming online, creating near-term price pressure in some regions and modest upward price movement in others where demand held firm.

For 2026, three dynamics will dominate boardroom agendas:

Feedstock and energy exposure: Production economics remain exposed to upstream monomer and energy inputs derived from petroleum streams. Procurement teams must embed crude-oil sensitivity into cost models and evaluate diversified feedstock contracts or backward integration options where feasible.

Regulation-driven premiumisation: Stricter effluent and chemical-safety requirements are shifting buyer preference toward higher-performance polyelectrolytes and certified suppliers. This creates opportunities for premium-priced formulations and lifecycle service bundles (dosing optimization, monitoring, waste-reduction programs).

Selective consolidation & capacity optimization: With the market exhibiting mid-level concentration and sizable regional manufacturing capacity, the optimal 2026 play differs by company scale—global leaders should prioritize service and scale-driven cost leadership, while mid-tier and regional players should emphasize product differentiation and local service excellence.

The competitive analysis in the report profiles the broad mix of global leaders, regional champions, and industrial suppliers shaping the market. Below are the principal archetypes and representative firms analyzed (profiles include strategic positioning, manufacturing footprint, product breadth, and commercial approaches):

Global volume leaders — SNF Floerger (Andrézieux, France; https://www.snf.com) stands out for high-volume polyacrylamide capacity and deep water-treatment focus. These players leverage scale for cost competitiveness and global distribution.

Integrated chemical majors — BASF SE (Ludwigshafen, Germany; https://www.basf.com) and Arkema (Colombes, France; https://www.arkema.com) offer comprehensive portfolios and strong R&D platforms that enable rapid product adaptation to regulatory or performance requirements.

Water-chemicals specialists — Kemira (Helsinki, Finland; https://www.kemira.com), Solenis (Wilmington, Delaware, USA; https://www.solenis.com), and Ecolab/Nalco (St. Paul, Minnesota, USA; https://www.ecolab.com) differentiate through technical services, on-site dosing expertise, and customer retention programs—critical in municipal and industrial wastewater markets.

Diversified chemical suppliers & regional producers — Dow (Midland, Michigan, USA; https://www.dow.com), Thermax (Pune, India; https://www.thermaxglobal.com), and a set of Asian manufacturers (e.g., Xinqi Polymer, regional Chinese producers) supply a mix of commodity and tailored chemistries for local markets. Their strategic advantage is agility and cost-competitive manufacturing.

Strategic takeaways for 2026:

Large players will continue to compete on integrated service offerings and technical differentiation; expect investment in monitoring/digital dosing services that convert chemistry into recurring revenue.

Regional producers can win through reliability, price leadership in local procurement cycles, and fast regulatory-response times—critical where on-the-ground compliance timelines are compressed.

Mid-market consolidation remains opportunistic: buyers with strong balance sheets can acquire capacity or niche product lines to broaden portfolios and capture synergies in logistics and R&D.

Market sizing and forecast (2026–2032) with scenario analysis for high/low demand and feedstock-price shocks.

Segmentation frameworks by product chemistries, applications and regions—presented with decision matrices (note: detailed subsegment tables and exact breakdowns are available only in the full report).

Supply‑chain mapping: upstream feedstock dependencies, contract structures, and manufacturing capacity overlays to identify pinch points and sourcing alternatives.

Raw-material pricing dynamics and sensitivity models that link acrylamide and energy cycles to producer margin profiles.

Regulatory and ESG impact assessment with compliance roadmaps by geography and application.

Competitive benchmarking: differentiated playbooks for global leaders, regional champions and specialty providers—covering commercial model, R&D focus, and likely moves in M&A and partnerships.

Go‑to‑market strategies and procurement checklists for 2026: pricing playbooks, tender design, and contract terms to lock in supply while preserving flexibility.

Case studies and executive-ready slide packs for board deliberations.

We recommend four priority actions for companies running 2026 planning cycles:

Re-run capital-allocation models under at least two feedstock-price scenarios. If your business is polymer-heavy, include a sensitivity band for upstream monomer and energy costs to avoid margin erosion.

Elevate regulatory-readiness from compliance to competitive advantage: invest selectively in high-performance chemistries and ancillary services (process optimization, monitoring). These investments typically yield shorter payback in regulated municipal and industrial procurement environments.

Rethink procurement: blend long-term off-take agreements with flexible spot coverage and consider regional dual‑sourcing to manage logistics risks and local regulatory changes.

Pursue outcome-based commercial models: customers increasingly value lower total-treatment cost and predictable effluent outcomes. Packaging chemistries with monitoring and service creates stickiness and improves gross margin resilience.

PW Consulting’s assessment synthesizes primary interviews with buyers, manufacturers and distributors, validated production-capacity datasets, and proprietary pricing models. Historical data covers 2020–2025; the 2026–2032 forecasts leverage trend extrapolation, scenario stress-tests, and sensitivity runs to produce a robust planning envelope. Wherever numerical granularity is commercially sensitive (subsegment shares, customer-level contracts), we preserve confidentiality while providing the directional and scenario intelligence executives need to act.

This release is intended as a strategic preview. The full report contains the exact segmentation tables, regional and application breakdowns, company scorecards and downloadable slide packs required for procurement tenders, board presentations, and M&A due diligence. For clients preparing 2026 budgets, supply contracts, or M&A pipelines, access to the full dataset and appendices will materially accelerate decision cycles and reduce execution risk.

Contact PW Consulting to request the full Polyelectrolyte Market report, bespoke briefings, or a custom scenario workshop for your executive team. Our analysts can translate the forecast envelope and competitive playbooks into a tailored plan aligned with your 2026 priorities.

For detailed analysis of this topic, please visit the official page:Polyelectrolyte Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com