Direct Debris Removal Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-26 08:27:36

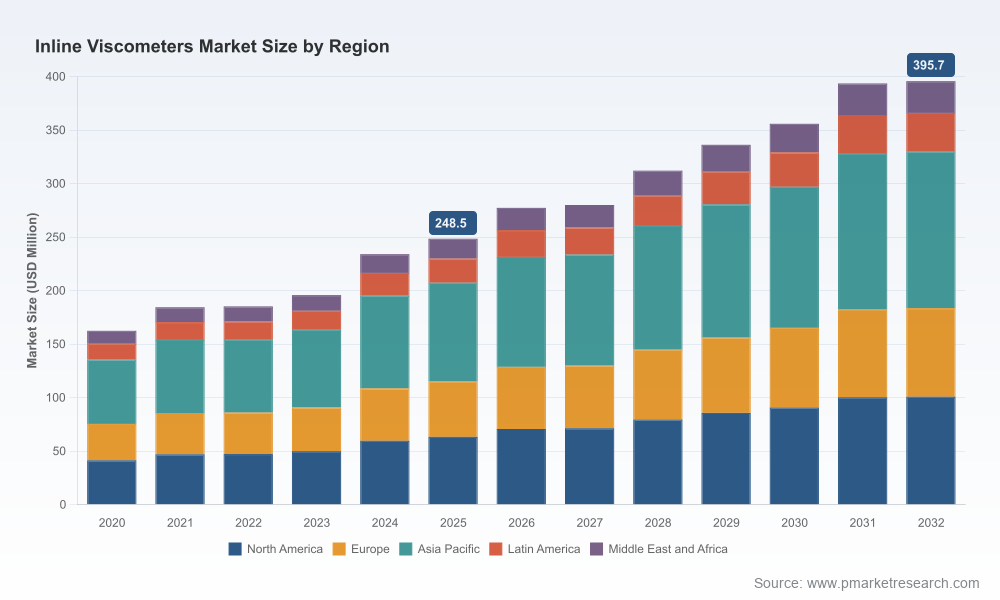

PW Consulting’s latest market study on Inline Viscometers (base year 2025; forecast 2026–2032) identifies a maturing but still dynamic marketplace that will materially influence process control and product-quality economics across oil & gas, chemicals, food & beverage, and pharmaceuticals. The market has expanded from roughly USD 162 million in 2020 to USD 248.5 million in 2025 and is projected to grow to roughly USD 396 million by 2032, representing a compound annual growth rate (CAGR) of about 6.85% over the forecast window. This brief synthesizes the report’s high‑impact, actionable conclusions for 2026 decision-makers while preserving the underlying segment-level data — available in full from PW Consulting.

Inline Viscometers Market

Operational digitalization is accelerating the shift from offline sampling to inline, real‑time measurements. The economic and regulatory incentives to reduce batch variability, lower scrap rates and accelerate product release are converging into procurement mandates for continuous viscometry.

Inline Viscometers Market

Advances in sensor technology — including resonant and other non‑invasive measurement principles — are reducing maintenance burdens and increasing uptime, widening the addressable market to applications formerly deemed too aggressive or sanitary for inline sensors.

Inline Viscometers Market

Regulatory standards and test-method harmonization (e.g., ISO 3219:2021 for rotational viscometry) continue to influence adoption patterns by specifying accepted measurement approaches for quality release and compliance workflows.

Supply‑chain normalization and capital‑expenditure cycles in heavy industries make 2026 the year to convert pilot projects into scalable programs: organizations that standardize on an inline measurement architecture this year will realize the largest marginal benefit over the next three years.

Modelled market-size and demand scenarios: a transparent, sensitivity-tested forecast that supports CAPEX prioritization and ROI thresholds for project approvals.

Supplier evaluation framework: vendor scorecards that compare technical fit, integration complexity, lifetime cost of ownership, service networks and roadmap alignment (for confidentiality reasons, the full scorecards and numeric ratings are available in the report).

Technology assessment and implementation archetypes: detailed profiles of vibrational, rotational, torsional and hybrid measurement approaches, including where each technology minimizes total cost of ownership or maximizes measurement fidelity.

Procurement and contracting playbook: practical tender language, performance SLA templates, acceptance test plans and tips for structuring multi‑year service agreements to hedge obsolescence risk.

Case studies and pilot-to-scale blueprints: step‑by‑step accounts from process lines that moved from manual sampling to continuous inline control and the measurable benefits realized in cycle time, waste reduction and margin improvement.

Risk register and mitigation menu: supply‑chain, regulatory, calibration and cyber‑security risks mapped to mitigation options and decision triggers.

M&A and partnership radar: themes and target archetypes for companies looking to extend their sensing footprint either through inorganic acquisitions or strategic OEM alliances.

Prioritize pilots that map directly to margin improvement. Rather than running broad exploratory trials, select pilot lines where inline viscosity will have clear, traceable financial impact — lower rework, higher yield or faster time‑to‑release. Use the report’s ROI templates to pre‑qualify projects.

Establish an integration architecture before vendor selection. Measurement hardware is now indistinguishable from data architecture: ensure your control system, historian and analytics layers can accept high‑frequency viscosity feeds, and determine whether edge pre‑processing or cloud analytics will be primary.

Adopt a technology-fit matrix, not a brand-first approach. Different sensor principles have distinct failure modes, sanitary constraints and calibration regimes. The report’s technology matrix helps match sensor type to fluid characteristics, process temperatures and cleaning regimes.

Negotiate service and calibration into the procurement price. For high‑value continuous processes, lifetime service, rapid-response calibration and local spares materially influence total cost. Structure contracts with outcome‑based SLAs where possible.

Monitor concentration and provider risk. The market shows meaningful concentration among a small set of established vendors (our analysis indicates leading-three firms account for a material share and the leading-five increase that degree of concentration). This creates advantages — depth of service and integration — and risks — single‑source dependencies and price cycles. Use multi‑sourcing or second‑tier supplier development as mitigants.

Plan for regulatory and standard evolution. ISO 3219 and related harmonized methods shape acceptance criteria for product release; keep a regulatory watchlist and design validation protocols to align with certification requirements.

AMETEK Brookfield (USA) — A long‑standing name in viscosity measurement, Brookfield’s inline sensor offerings are positioned for continuous process monitoring in food, chemical and pharmaceutical lines. Their strength is deep application experience and broad aftermarket support.

Anton Paar GmbH (Austria) — Known for precision laboratory instrumentation, Anton Paar has extended its portfolio into production‑grade inline sensors and process analytics; its emphasis is on accuracy and lab‑to‑line traceability.

Rheonics AG (Switzerland) — A leader in resonant sensor technologies, Rheonics targets oil & gas, coatings and food sectors with compact inline viscometers and density meters that trade high precision for minimal maintenance.

Emerson Electric Co. (USA) — Emerson’s strategy is systems integration: marrying inline viscosity measurement with flow and mass meters to provide consolidated process measurements and reduce instrument count and wiring complexity.

KROHNE Messtechnik GmbH (Germany) — KROHNE focuses on heavy process industries (chemical, petrochemical and food processing) with rugged inline viscometers designed for aggressive process conditions and long service intervals.

Each of these vendors brings differentiated strengths — service footprint, sensor technology, integration capability or industrial pedigree. Our full vendor section includes a comparative matrix, capability heatmaps, and buyer negotiation notes for each provider.

Calibration and drift. Inline sensors reduce sampling error but require structured calibration plans. Mitigation: implement automated zero/check routines and vendor-supported calibration intervals tied to process risk.

Integration complexity. High‑frequency data can overwhelm legacy historians and introduce latency. Mitigation: define data architecture up‑front, use edge pre‑processing for event detection and standardize on OPC‑UA or equivalent protocols.

Sanitation and materials compatibility. Food and pharma lines pose CIP/SIP constraints. Mitigation: select sanitary-rated sensor variants and validate with accelerated cleaning cycles during procurement.

Cyber security. Connected sensors expand the attack surface. Mitigation: enforce network segmentation, device hardening and firmware management policies.

Supplier concentration. Heavy reliance on a single vendor can create service bottlenecks and price negotiation imbalance. Mitigation: dual sourcing, local spare inventories and staged migration plans.

For executives preparing capital plans and technology roadmaps in 2026, the report provides an operationally focused, decision‑ready toolkit: validated market forecasts, procurement templates, integration checklists and vendor playbooks. We designed the deliverables so that procurement, engineering and operations teams can move from pilot to plant‑wide deployment with minimized risk and clear, measurable KPIs.

To maintain the value‑preserving “trailer” approach, this summary intentionally omits the full segmentation tables, regional and application breakdowns, and the detailed numerical vendor‑score outputs — all of which are included in the full PW Consulting report. Those datasets contain the granular inputs needed to populate capital approval decks and vendor selection RFPs.

If your 2026 capital plan includes investments in process analytics, inline control, or quality automation, engage PW Consulting for a tailored briefing. We will walk through the model assumptions, run scenario evaluations on your specific product lines, and provide a prioritized implementation roadmap that aligns with your margin and compliance objectives.

For detailed analysis of this topic, please visit the official page:Inline Viscometers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com