Everything You Need to Know About Acupuncture Treatment in Dubai | Benefits, Process & Wellness

Health |

2026-07-11 12:08:38

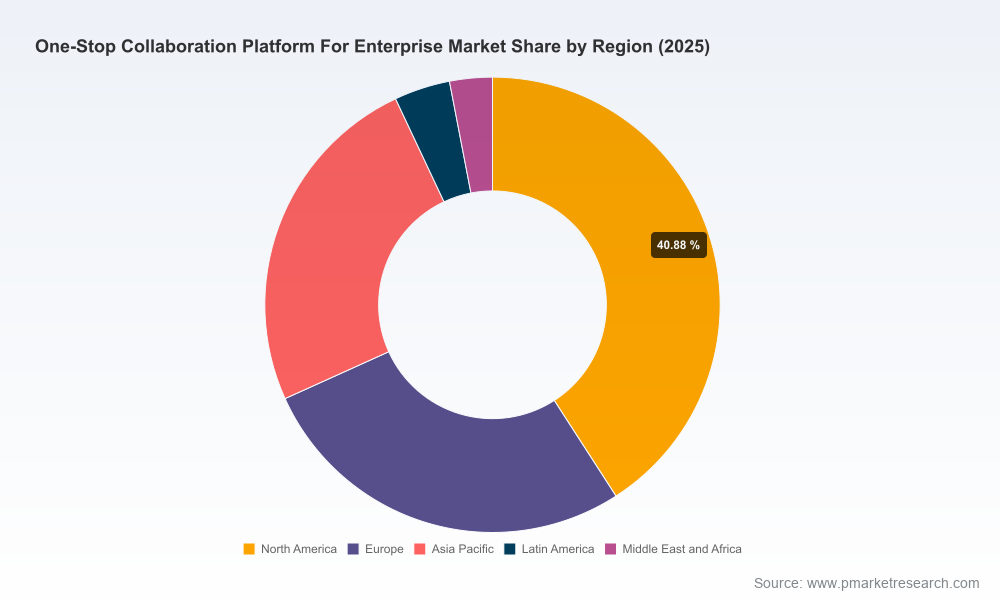

As enterprises finalize budgets and roadmaps for 2026, PW Consulting’s new market study on One Stop Collaboration Platforms delivers a decisive strategic resource. The market’s macro trajectory is unambiguous: the sector expands from a base year size of approximately USD 78.5 billion (2025) toward an estimated USD 179 billion by 2032, reflecting a compound annual growth rate (CAGR) of 12.48% over the 2026–2032 forecast window. That pace, coupled with a market concentration profile where the top three and top five providers account for a significant majority of value, creates both competitive pressure and clear opportunities for enterprise buyers, vendors, and channel partners.

One Stop Collaboration Platform For Enterprise Market

Decision horizon alignment — Buyers must translate growth and vendor consolidation signals into procurement, architecture, and vendor-management timelines to avoid lock-in and costly mid-cycle migrations.

One Stop Collaboration Platform For Enterprise Market

Investment prioritization — The available growth and technology trends highlight where spend on integration, security, and AI-enabled productivity will yield the highest risk-adjusted returns.

One Stop Collaboration Platform For Enterprise Market

Regulatory preparedness — New privacy regimes and state-level laws entering force in 2026 materially change contract requirements, operational controls, and vendor selection criteria.

The full PW Consulting report is designed as an operational toolkit for enterprise leaders and procurement teams. It balances market-level forecasting and vendor intelligence with hands-on resources that support procurement, architecture, and deployment. Key components include:

Strategic market primer — concise scenarios for enterprise buyers showing supplier consolidation effects, cloud hosting trends, and adoption velocity across hybrid work models.

Vendor scorecards — comparative frameworks that evaluate vendors across security, integrations, service models, AI capabilities, and extensibility. (Note: detailed vendor weightings and score matrices are included in the full report.)

Procurement and contracting playbook — clauses, SLA templates, and data transfer language aligned to emerging privacy laws and ADMT (automated decision-making technology) disclosure requirements.

Implementation roadmaps — phased migration blueprints, coexistence patterns for hybrid and cloud-first deployments, and cost-control levers for cloud-hosting expenses.

TCO and ROI models — customizable templates that integrate licensing, integration effort, operational support, and productivity delta assumptions to calculate payback periods under multiple adoption scenarios.

Security and compliance checklists — prescriptive controls for data residency, encryption-in-transit and at-rest, vendor audit readiness, and vendor contract governance.

Executive decision matrices — simple, board-ready artifacts that map business outcomes to procurement options and risk profiles.

AI as a differentiator — AI features are moving beyond “nice-to-have” automation to drive procurement decisions. Vendors that embed meeting intelligence, summarization, and workflow automation into core collaboration workflows can materially reduce time-to-value.

Cloud economics and hosting risk — public cloud spend has reached the high hundreds of billions range globally, placing pressure on platform architects to optimize architecture for predictable unit costs, especially for real-time media, storage, and search workloads.

Regulatory tightening — new privacy requirements (including expanded CCPA provisions effective January 1, 2026, and evolving state laws) mean that vendors must present defensible data processing maps and contractual guarantees; buyers need to bake verification and auditability into selection criteria.

Consolidation vs. best-of-breed — the market exhibits measurable concentration among leading vendors. This creates a trade-off between vendor-managed ecosystems (ease of integration, single-bill) and best-of-breed stacks (specialized capabilities, potential interop complexity).

The competitive field is characterized by a mixture of platform incumbents, productivity-suite bundlers, and specialized work-management players. Our analysis focuses on strategic posture rather than raw market shares — full competitive matrices are available in the report.

Microsoft — Leverages deep integration across productivity, identity, and endpoint management. Continued rollout of advanced Copilot capabilities through Teams accelerates automation and meeting-insight value propositions. Microsoft’s scale favors enterprises seeking consolidated licensing and integrated security controls.

Google (Workspace) — Differentiates with cloud-native collaboration on documents and real-time co-editing, paired with a simple admin experience. Google’s strength is rapid, low-friction collaboration; its roadmap emphasizes contextual AI and tighter enterprise administrative controls.

Slack / Salesforce — Positioned at the intersection of collaboration and CRM/workflow orchestration. Slack’s integration with Salesforce is evolving toward customer-facing workflow scenarios, making it compelling for revenue- and service-centric teams.

Cisco (Webex) — Competes on security, hybrid meeting experiences, and enterprise networking synergies. Webex’s AI investments and room-system integrations appeal to organizations prioritizing secure, high-quality hybrid collaboration.

Zoom — Maintains strength in synchronous communications and is expanding into broader collaboration and phone systems. Its strategy targets simplicity and interoperability for meeting-first workflows.

Atlassian, Asana, Wrike, ClickUp — These players focus on work management and structured collaboration, offering strong integrations into agile and project-centric environments. Recent product updates (e.g., Wrike’s template and AI agents) indicate rapid feature delivery aimed at increasing stickiness with project teams.

Zoho, Bitrix24, RingCentral — Provide integrated suites that appeal to mid-market and distributed organizations seeking consolidated communications and back-office functionality.

Recent product and go-to-market moves (AI feature expansions, room-system integrations, and feature releases through late 2025 into early 2026) illustrate a fast-shifting feature frontier. Enterprises should treat vendor roadmaps as a selection criterion rather than relying solely on current capability sets.

Define outcomes, not features — craft RFPs around measurable outcomes (meeting time saved, incident response time improvements, accelerated deal cycles) and require vendors to propose measurable KPIs tied to those outcomes.

Force-feed integration scenarios — demand vendor demonstrations that integrate with your identity, directory, ticketing, and CRM systems using your data and sample workflows, not vendor-supplied sandboxes.

Pilot for migration complexity — design pilots that validate coexistence patterns, latency under load, and admin workflows. Include rollback and cutover criteria in pilot success definitions.

Validate compliance posture — require contractual commitments for data processing, breach notification, and audit rights tailored to the new privacy landscape.

Privacy regimes entering force in 2026 increase the cost of non-compliance. Buyers should run updated DPIAs (data protection impact assessments) for collaboration platforms, include ADMT opt-out handling where applicable, and insist on vendor transparency around model training data and AI decisioning. Additionally, cloud-hosting costs and network egress can materially affect long-term TCO — PW Consulting’s TCO templates quantify these variables under alternative hosting scenarios.

Consolidation-first enterprises: If your priority is unified management, single-pane security, and minimized vendor management, prioritize platform suites with strong identity, endpoint, and productivity integration. Negotiate enterprise-wide SLAs and favorable audit clauses to offset concentration risk.

Best-of-breed adopters: If specialized capabilities or industry-specific workflows are critical, invest in integration platforms and automation layers to reduce operational friction. Insist on open APIs and formalized integration SLAs.

Cost-sensitive organizations: Use the report’s TCO scenarios to stress-test hosting and media-storage assumptions, and split workloads between cloud-managed services and optimized on-premise/hybrid components where latency or data residency requires it.

To maintain concise executive utility and to protect the granular intelligence that fuels procurement advantages, this briefing omits detailed regional and vertical revenue splits, vendor-by-vendor revenue figures, and cell-level segmentation tables. The complete PW Consulting report includes:

Comprehensive regional and vertical breakdowns and growth vectors

Vendor scorecards with weighted criteria and technical test results

Customizable procurement templates and build-vs-buy financial models

Detailed scenario modeling files for in-house use

90 days: Update procurement templates to include privacy-specific clauses and outcome-based KPIs; shortlist 2–3 vendors for technical pilots.

180 days: Run integration and compliance pilots, finalize licensing scenarios, and commence phased migration planning for non-critical workloads.

365 days: Execute enterprise-wide rollouts aligned to validated ROI thresholds and continuous monitoring of AI feature maturity and regulatory shifts.

PW Consulting’s One Stop Collaboration Platform study is intentionally structured to support these decisions with both market-level foresight and practical implementation tools. For the complete dataset, granular vendor matrices, and downloadable TCO/ROI models, access the full report on PW Consulting’s research page.

For detailed analysis of this topic, please visit the official page:One Stop Collaboration Platform For Enterprise Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com