Cell and Tissue Culture Bags Market: Strategic Imperatives for 2026 — A PW Consulting Preview

As bioprocessing and advanced cell therapies enter a decisive commercialization phase, cell and tissue culture bags have moved from niche consumables to strategic enablers of downstream manufacturing scale, cost control, and regulatory compliance. PW Consulting’s forthcoming market study (base year 2025; historical coverage 2020–2025; forecast 2026–2032) quantifies this transition and translates it into actionable guidance for executives making 2026 investment and operational decisions. This preview highlights the report’s core strategic takeaways while preserving the detailed segmentation and forensic data for the full release.

Cell And Tissue Culture Bags Market

A fast-growing, investable market

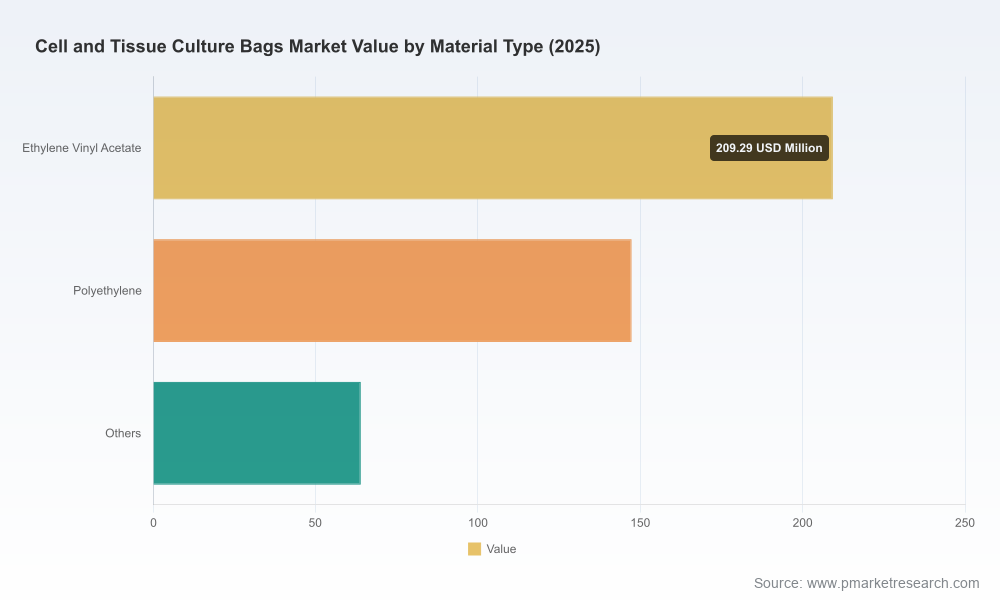

The market for cell and tissue culture bags is expanding at a near-double-digit compound annual growth rate of 9.85% through our forecast window. From a 2025 baseline, the market roughly doubles by the end of the 2026–2032 forecast period, reflecting accelerating demand across biologics production, cell therapy manufacturing, and diagnostic workflows. This growth is not uniform — it is driven by technology shifts (single-use adoption, higher-purity film formulations), regulatory expectations for traceability and biocompatibility, and evolving supply-chain strategies among biomanufacturers.

Cell And Tissue Culture Bags Market

Why this matters to corporate decision-makers in 2026

- Operational leverage and cost-to-clinic. For cell therapy producers, bag selection and supplier strategy materially affect process yields, sterility assurance, and scale-up timelines. Small choices in bag film and connector systems propagate into facility footprint and COGS when scaled to commercial batches.

- Regulatory and quality alignment. Single-use consumables must meet cGMP requirements and biocompatibility standards (e.g., ISO 10993, USP guidance). Suppliers’ certifications — including ISO 13485 and regional MDSAP recognition — are now gating factors in qualified vendor lists and regulatory submissions.

- Supply resilience and concentration risk. The market shows moderate concentration among leading suppliers, creating both advantages (reliable quality, scale) and exposure (single-source dependencies). Sophisticated manufacturers will blend long-term agreements, dual-sourcing, and local buffer inventories to de-risk clinical and commercial programs.

- Material science as a strategic lever. High-purity films such as FEP, high-grade polyethylene, and EVA each deliver distinct trade-offs in gas permeability, extractables, and mechanical performance. Material selection should align with process modality (adherent vs non-adherent cells, cryopreservation, wave vs stirred systems) and downstream processing plans.

What the full PW Consulting report delivers — practical, transaction-ready insight

This study is structured to move rapidly from market intelligence to executable decisions. The full report contains:

Cell And Tissue Culture Bags Market

- Comprehensive market sizing and seven-year forecasts (2026–2032), including scenario modelling that quantifies outcomes under moderate, accelerated, and conservative adoption curves.

- Commercially focused competitive landscaping with vendor profiles, capability maps, and an assessment of manufacturing footprints and certifications.

- Supplier risk matrix and sourcing playbooks that recommend procurement strategies for clinical-stage firms, CMOs, and large-scale biomanufacturers.

- Product and process compatibility triage — a practical decision-tree to match bag materials and configurations to cell types, culture modes, and regulatory endpoints.

- Deal and partnership intelligence — a summary of M&A, JV, and co-development patterns shaping the supplier ecosystem and a set of red flags for diligence.

- Financial implications and cost modelling templates to estimate COGS impacts from bag choice, scale effects, and supplier mixes (templates are provided in editable format for client use).

- Executive playbook: prioritized actions and a 90/180/360-day roadmap to capture commercial upside while controlling operational risk.

Competitive landscape — profiles and strategic positioning

The market is served by a mix of specialized suppliers and larger life-sciences OEMs. Each player brings differentiated strengths that influence procurement, integration, and validation strategies:

- OriGen Biomedical (Austin, Texas). Focused on high-purity FEP-based products such as PermaLife and Evolve, OriGen emphasizes gas permeability and cryopreservation-capable designs. Its recent organizational milestones and facility recognition underscore growing manufacturing scale and regulatory alignment.

- Charter Medical (Winston-Salem, North Carolina). Known for EXP-Pak and Bio-Pak families, Charter addresses non-adherent cell expansion and modular bag systems used in cell therapy workflows and bioprocessing lines.

- Thermo Fisher Scientific (Waltham, Massachusetts). Under the Gibco brand, Thermo Fisher couples consumables with automation and bioreactor integration, offering disposable pre-filled and connector-ready solutions that favor scaled, instrumented manufacturing.

- Corning Incorporated (Corning, New York). Corning’s polyolefin gas-permeable bags target wave and rocker culture formats and emphasize established quality systems compatible with cGMP applications.

- Saint-Gobain (Life Sciences operations). Supplies customized processing bags with optimized gas transmission for applications such as T-cell expansion, leveraging material science and customization capabilities.

- Sartorius (Göttingen, Germany). Offers single-use bioreactor and culture bag systems for wave-mixed and stirred platforms (Flexsafe RM and STR lines), positioning itself where bag technology intersects with single-use bioreactor adoption.

Recent public developments (notably multiple OriGen highlights in early 2026) reflect supplier-level investment in capacity and compliance — a trend we expect to continue as suppliers chase qualifying status with large biomanufacturers and CMOs.

Market structure and strategic implications

The market exhibits a moderate-to-high level of concentration among the top vendors, which creates predictable supply chains but also increases negotiation power for incumbents. For buyers and investors, this suggests a distinct set of playbooks:

- For clinical-stage sponsors: prioritize qualification of two suppliers per critical consumable family and include rigorous extractables and leachables testing in bridging strategies.

- For CMOs and large biomanufacturers: pursue longer-term supplier alliances and invest in in-house validation capabilities to accelerate line qualification when adopting new bag formats or materials.

- For suppliers and investors: assess vertical integration opportunities (e.g., film extrusion, sterile filling) and targeted M&A to capture downstream growth from cell therapy commercialization.

Risk factors and sensitivities

Decision-makers should weigh the following industry-specific risks in 2026 planning:

- Regulatory shifts. Evolving FDA/EMA expectations for extractables and process qualification can lengthen vendor qualification timelines; early engagement with suppliers and regulators reduces this risk.

- Raw-material volatility. High-purity film feedstocks command premium pricing and supply flexibility; forward contracts and dual-sourcing for critical polymers are prudent.

- Compatibility mismatches. Misaligned choices between bag material and downstream processing equipment (connectors, sensors, disposables integration) add validation cost and time.

- Concentration-driven supply shocks. Reliance on a few large suppliers increases exposure to capacity constraints during demand surges; buffer inventory strategies and regional sourcing help mitigate.

Actionable recommendations for 2026

- Execute a supplier qualification sprint. Prioritize validating at least two qualified suppliers for each class of critical bag within 6–9 months. Include extractables/leachables, gas transmission, and mechanical integrity tests mapped to your product’s release criteria.

- Align material choice to scale-up strategy. Define a materials decision matrix that ties film type to cell type, culture environment, and downstream processing steps to avoid late-stage revalidation costs.

- Negotiate supply agreements with flexibility. Incorporate volume tiers, capacity reservation clauses, and rapid response SLAs to manage demand variability during pivotal clinical-to-commercial transitions.

- Invest in in-house verification labs. A modest capital allocation to bench-scale testing capabilities for extractables and compatibility can reduce external testing cycles and accelerate supplier onboarding.

- Monitor regulatory and standards developments. Maintain a cross-functional regulatory-compliance tracker for ISO 13485, MDSAP, and single-use bioprocessing guidance; anticipate changes and build them into product release timelines.

Why PW Consulting’s report is decision-critical for 2026

Our study goes beyond market arithmetic to provide the playbooks and analytic tools that convert commercial intelligence into boardroom decisions. It couples a data-driven forecast (2026–2032) and concentration metrics with supplier diligence, materials engineering guidance, and procurement checklists — all calibrated for the commercialization inflection many cell-therapy and biologics programs face in 2026.

For executives evaluating capital allocation, supplier strategies, or M&A, the report’s scenario models and transaction-oriented insights are designed to shorten time-to-decision and to lower execution risk by surfacing the most impactful operational levers.

Next steps

This preview is intended to prepare leaders for the strategic choices confronting them in 2026. The full PW Consulting Cell and Tissue Culture Bags Market report includes the detailed segmentation, vendor scoring, downloadable financial models, and an executable 360-day roadmap that together support procurement, R&D, and corporate development teams. To access the complete analysis and proprietary datasets, please visit the PW Consulting research library or contact our industry practice team for a briefing and demo.

PW Consulting remains available to support immediate due diligence, supplier negotiations, and bespoke scenario planning tailored to your organization’s product pipeline and manufacturing footprint.

For detailed analysis of this topic, please visit the official page:Cell And Tissue Culture Bags Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com