Data Center Operations & Maintenance Services: Strategic Imperatives for 2026 — PW Consulting Market Preview

As enterprises recalibrate digital infrastructure strategies for the post-pandemic, AI-accelerated era, data center operations and maintenance (O&M) has moved from a back-office cost center to a mission-critical strategic function. PW Consulting’s forthcoming Data Center Operations And Maintenance Service Market report — based on a comprehensive analysis through the base year 2025 and projecting to 2032 — synthesizes the operational, financial, and regulatory levers that will determine which operators win in the next cycle of scale, efficiency and resiliency investments.

Data Center Operations And Maintenance Service Market

Market snapshot: scale, pace, and structural signals

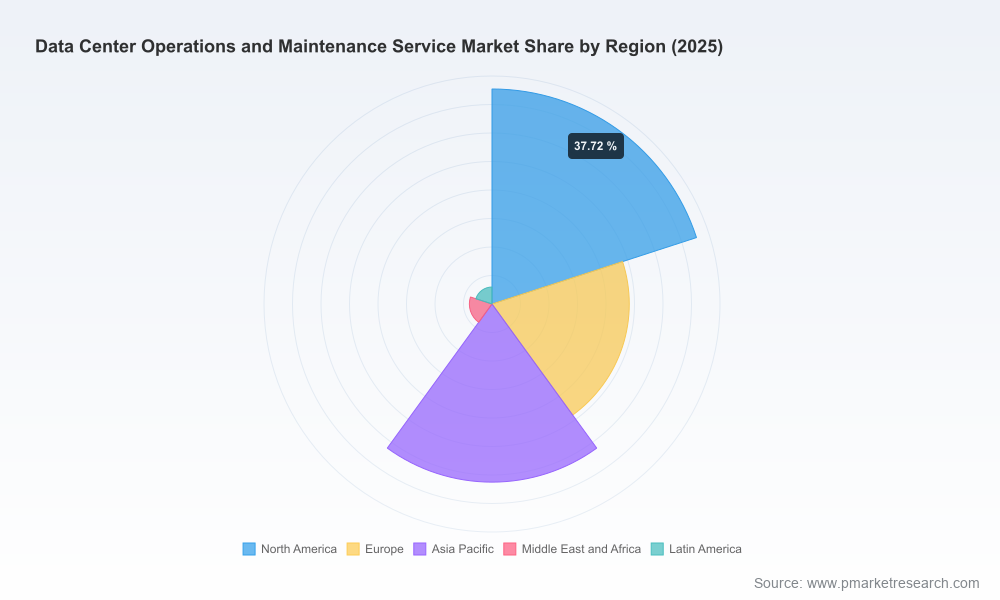

The market is sizable and expanding rapidly: from the established 2025 baseline, PW Consulting’s macro model forecasts continued expansion through 2032 at a compound annual growth rate of 11.69% for the forecast period. The trajectory reflects broad secular drivers — hyperscale buildout, colocation densification, edge rollouts, and enterprises migrating to hybrid architectures — and results in a materially larger global O&M services opportunity by 2032 than today. Equally important, market concentration metrics show a moderately consolidated supplier landscape: the top three providers account for roughly the high‑thirties percentage of market share and the top five encompass just over half of the market, indicating both incumbent strength and meaningful room for differentiated specialists and regional players.

Data Center Operations And Maintenance Service Market

Why this matters for enterprise decision-makers in 2026

- Strategic timing: 2026 is a pivot year. Capital commitments made this year to O&M models, whether outsourced managed services, third-party maintenance, or in‑house modernization, will determine total cost of ownership and agility across a 10–20 year infrastructure lifecycle.

- Operational resilience vs. cost trade-offs: Rising labor pressures, automation potential, and energy efficiency mandates are compressing traditional trade spaces. Labor shortages remain acute — nearly two‑thirds of operators reported difficulty retaining or recruiting qualified O&M staff in 2025 — forcing many buyers to choose between higher wage bills and greater automation/managed service adoption.

- Regulatory and compliance inflection points: New editions of energy and design standards and heightened expectations for data privacy and security certification are shifting the compliance burden into O&M playbooks. For organizations that must meet ISO/IEC 27001, SOC 2, or regional privacy regimes, O&M partners are increasingly evaluated for demonstrable compliance capabilities, not just response times.

- Cost visibility and lifecycle planning: Independent analyses highlight the scale of labor and operating costs during buildout and operation. Firms that integrate robust lifecycle O&M forecasting into procurement can avoid the frequent “greenfield optimism” bias that underestimates long‑run operating expenditures and staffing needs.

What the report delivers: practical, decision-ready content (not a data dump)

PW Consulting’s report is designed as a strategic playbook for procurement, operations, and infrastructure leadership — not simply an academic market write-up. Contents include:

Data Center Operations And Maintenance Service Market

- Actionable decision frameworks that map business objectives (e.g., latency, regulatory footprint, sustainability targets) to plausible O&M delivery models.

- Operational readouts and KPI templates for service-level agreements (SLAs), preventive maintenance cadences, spare-parts strategies, and failure-mode prioritization.

- Financial models and TCO templates allowing scenario analysis across insourcing, third‑party maintenance, managed services, and as‑a‑service alternatives, calibrated to PW Consulting’s macro market trajectory.

- Procurement playbooks and vendor scorecards for RFP design, vendor evaluation, and transition risk management — complete with contract clauses to protect uptime and control unanticipated cost escalation.

- Field-tested implementation checklists: commissioning and handover, seasonal readiness, predictive analytics adoption pathways, and KPI governance rhythms for senior management.

- Case studies and playbooks illustrating how leading operators translate standards (e.g., the latest energy standards and security certification requirements) into repeatable operational practices.

To honor the “trailer” principle: this preview showcases the report’s depth and practical value while reserving the full proprietary segment tables and granular vendor benchmarking for the report itself, which is available on PW Consulting’s website.

Competitive landscape: how incumbents and challengers are positioning for 2026

The supplier ecosystem is composed of global systems integrators, specialized third‑party maintenance firms, hyperscale operators with captive O&M capabilities, and professional services providers. Several strategic patterns are worth emphasizing:

- Platform + services bundling: Technology OEMs are leveraging platform ecosystems to embed O&M value. For example, firms offering integrated DCIM, predictive analytics, and lifecycle management are pushing beyond pure hardware maintenance toward outcome‑based contracts.

- Colocation operators scaling managed services: Large global colocation and interconnection providers continue to extend managed O&M offerings to capture an expanded share of customer spend and to protect margins as power and space commoditize.

- Third‑party specialists: Independent maintenance providers and facilities management firms offer multi‑vendor hardware support and scope flexibility; they are attractive to organizations seeking cost arbitrage without vendor lock‑in.

- Strategic partnerships and capacity deals: Expect more capacity agreements and long‑term partnerships between hyperscale demand and global operators to lock in scale and operational synergies.

Key players in the market exemplify these strategic archetypes. Global engineering and power/cooling specialists emphasize lifecycle and predictive services via integrated platforms; systems integrators and network vendors combine automation and security into O&M offerings; colocation giants continue to scale managed services while hyperscalers and global data center operators secure capacity and operational consistency through strategic agreements. Recent market activity — large multi‑year private cloud modernization contracts, acquisitions of facility management specialists, and multi‑MW capacity agreements — underscores that both organic capability building and inorganic consolidation are active levers going into 2026.

Operational headwinds and cost levers

- Labor and skills: The sector continues to be labor-constrained. Independent estimates highlight the massive labor dimension of data center buildout and operation; this reality elevates vendor capability in remote operations, automation, and structured skills pipelines as decisive selection criteria.

- Energy and efficiency: New energy standards and expectations for PUE and carbon management make cooling and power O&M a primary battleground for value capture.

- Compliance and security: Certification readiness and evidence-based operational controls have become procurement must-haves, not optional differentiators.

Five strategic recommendations for enterprise leaders in 2026

- Adopt an attribute-based vendor selection process: prioritize operational outcomes (time-to-repair, predictive maintenance maturity, certification posture) over appliance-level pricing alone.

- Embed lifecycle O&M modeling in capital planning: require vendors to provide scenario-based TCOs over 10–15 years and stress-test for labor and energy cost volatility.

- Transition from reactive to predictive operations incrementally: pilot DCIM and AIOps integrations on critical corridors, then scale using a phased, KPI-governed rollout.

- Hedge workforce risk: build hybrid delivery models combining on-site critical talent with regional managed service partners and remote operations centers to mitigate local labor shortages.

- Make compliance a differentiator: require evidence of ISO, SOC and energy‑standard alignment as part of baseline commercial terms and governance cadences.

How PW Consulting’s report accelerates decision-making

For leaders who must decide in 2026, the value of the report lies in combining market foresight with execution-ready tools. PW Consulting translates the macro growth path and supplier dynamics into procurement checklists, TCO templates, and operational playbooks so that decisions are supported by quantified scenarios rather than intuitive bets. The report’s vendor benchmarking and contract negotiation guidance are particularly useful for teams seeking to convert strategic intent into enforceable operational outcomes.

Final note: why a preview, not the full dataset

This article intentionally previews the themes, tools, and strategic implications of the full market study without reproducing the report’s proprietary segment tables and granular vendor benchmarking. That material — which contains the specific segmentation analytics and model assumptions required to operationalize the recommendations — is available in the full PW Consulting report. Organizations preparing capital and operational plans in 2026 will find the complete dataset and templates indispensable for translating strategy into measurable, low‑risk deployments.

To access the full report and the decision-support tools it contains, visit PW Consulting’s Data Center Operations And Maintenance Service Market page for the full download and subscription options.

For detailed analysis of this topic, please visit the official page:Data Center Operations And Maintenance Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com