Fog Computing Market — A Strategic Brief for 2026 Decision-Makers

Executive summary

The fog computing market has moved from experimental proofs-of-concept to mission-critical deployments across industrial, infrastructure and enterprise environments. Our PW Consulting Fog Computing Market Report (base year 2025) quantifies an inflection: the global market expanded rapidly in the first half of this decade and is forecast to continue at a double‑digit compound annual growth rate, representing a transformational investment area for CIOs, CTOs and infrastructure leaders in 2026. This briefing highlights the strategic implications of the report for board-level decision-making while intentionally withholding the granular segmentation data contained in the full study to drive qualified follow-ups.

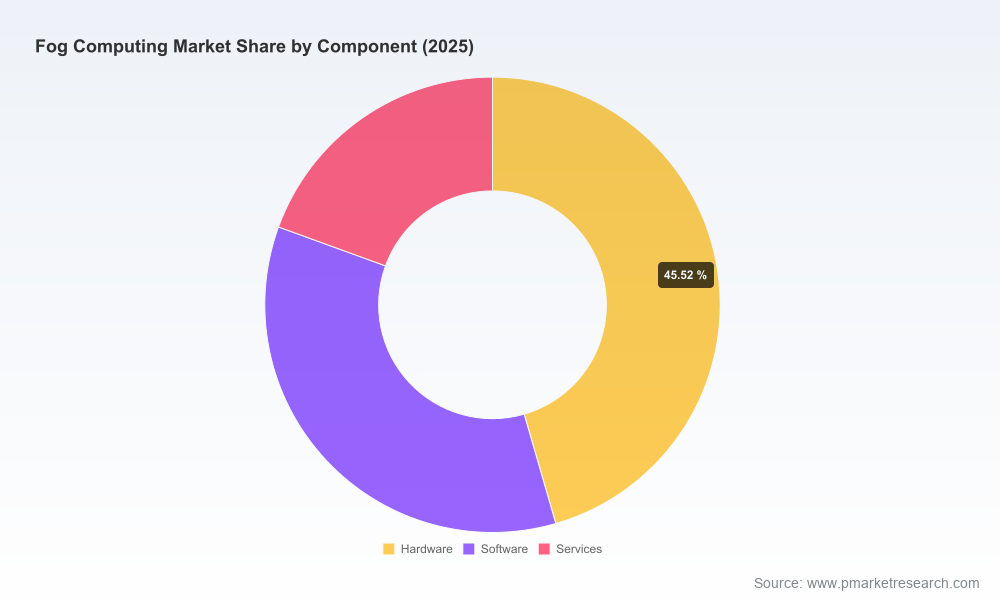

Fog Computing Market

Market trajectory: why 2026 is a strategic hinge year

Fog computing’s growth has been exponential. According to our analysis, the market moved from a low‑single‑digit billion-dollar base in 2020 to an order‑of‑magnitude larger footprint by 2025. The forecast period (2026–2032) assumes continued acceleration driven by latency-sensitive AI/ML workloads at the edge, industrial digitalization, and tighter regulatory and standards alignment. The market is projected to grow at a roughly 36% CAGR over the forecast window, with near-term step changes visible between 2025 and 2026 as early adopters transition to scaled deployments.

Fog Computing Market

For 2026 planning cycles this means three practical realities for enterprises: (1) vendor and architecture choices made now will materially affect TCO and upgrade paths over the next 5–7 years; (2) procurement timelines must accommodate integration, orchestration and cybersecurity hardening rather than treating fog as a simple hardware buy; (3) ecosystems and standards maturation will increasingly shape interoperability and lock‑in risks.

Fog Computing Market

What the PW Consulting report delivers (practical, implementable content)

- Strategic framework for capital allocation: prioritization matrix that aligns latency, data sovereignty, compute intensity and operational risk to investment cadence (pilot → scale → embed).

- Vendor evaluation playbook: repeatable scorecards and RFP templates that map functional requirements to vendor capabilities and long‑term total cost of ownership scenarios.

- Use‑case ROI models: configurable templates for 7 archetypal fog deployments (from predictive maintenance to smart mobility) that show payback intervals under conservative and aggressive adoption scenarios.

- Implementation roadmaps: sequenced milestones for integration of fog nodes, orchestration layers, AI inferencing at the edge, and lifecycle management covering 12–36 month horizons.

- Security and compliance toolkit: checklists for deploying quantum‑resilient encryption approaches, identity and attestation patterns for distributed nodes, and regulatory mapping for industrial/critical‑infrastructure operators.

- Organizational change plan: skill maps, operating model options (centralized, federated), and partner governance templates to bridge OT/IT boundaries.

Competitive landscape — who matters and why

The fog market is maturing but remains functionally diverse and commercially fragmented. The environment favors organizations that combine systems expertise, field‑hardened hardware, platform software, and partner networks. Notable profiles from our coverage:

- Cisco Systems — recognized as a conceptual pioneer in fog architectures; its IOx approach remains a go‑to model for secure, containerized applications at the network edge and is particularly attractive for industrial networking integrators.

- Dell Technologies — plays to strengths in ruggedized servers and gateways optimized for distributed fog topologies; compelling where enterprises require consolidated lifecycle services and supply chain continuity.

- Microsoft — brings hybrid cloud-to-fog continuity via Azure Stack Edge and related services; attractive for organizations standardizing on Azure for cloud services and looking to normalize management planes across environments.

- ARM Holdings — foundational supplier of energy‑efficient processor architectures that enable low‑power, high‑density fog nodes and accelerate workload-specific silicon strategies.

- FogHorn Systems — strong in real‑time analytics and industrial‑grade fog software for predictive and anomaly‑detection use cases; differentiates on streaming analytics and low-latency inference.

- GE Digital — leverages industrial domain expertise and Predix lineage to deliver fog-enabled OT suites for heavy industry asset management.

- Fujitsu — integrates fog with 5G and smart manufacturing stacks, proving effective in greenfield Industry 4.0 initiatives in APAC and beyond.

- Schneider Electric — combines energy and automation domain depth with an edge/fog-enabled platform approach for energy management and distributed control.

- ADLINK Technology — supplies ruggedized hardware and modules purpose-built for harsh industrial environments where durability and long lifecycle support matter.

- Nebbiolo Technologies, Crosser, IOTech — smaller, specialist vendors focused on IIoT platforms, real‑time data flows, and open‑source driven edge stacks — attractive as technology partners and integrators for niche deployments.

Strategic takeaway: buy, build or partner decisions should be made against three dimensions—hardware lifecycle and ruggedization, software orchestration and analytics capability, and ecosystem reach (systems integrators, telcos, industrial OEMs). The market’s present fragmentation (top vendor share well under majority control) creates opportunities for both megavendors and focused specialists; however, interoperability and long‑term support contracts will be decisive for enterprise risk committees.

Standards, regulation and a new security baseline

Standards and regulatory forces are converging on fog architectures. The conceptual model articulated in NIST guidance provides an accepted taxonomy for things→fog→cloud flows, while IEEE efforts and the legacy OpenFog reference architecture are shaping manageability, nomenclature, and interoperability. These initiatives reduce integration risk but also raise expectations for compliance and certification.

Security is entering a new phase: decentralized compute at scale increases the attack surface and elevates the need for post‑quantum resistant cryptography, secure boot and hardware attestation. Recent patent activity around quantum‑resistant encryption for fog nodes underscores that national security considerations are now part of procurement risk assessments for critical infrastructure providers.

Operational imperatives for 2026

- Design for negotiated interoperability: require vendors to demonstrate orchestration compatibility with open standards and provide sandboxed interoperability tests during procurement.

- Prioritize cybersecurity lifecycles: include firmware signing, secure update processes, and post‑quantum encryption roadmaps as mandatory contractual SLAs.

- Adopt hybrid operational models: implement federated governance that bridges central IT policy with local OT autonomy to accelerate rollouts while containing compliance risk.

- Run targeted pilots that are instrumented for learning: use short, outcome‑based pilots that validate latency, data locality, and economic assumptions before scaling.

- Negotiate vendor economics for scale: shift from capex‑only contracts to blended capex/opex models that align vendor incentives with long‑term performance and serviceability.

- Invest in skills and tooling: prioritize edge orchestration, observability and site reliability practices for distributed compute nodes rather than generic cloud operations skill sets.

How PW Consulting’s recommendations should shape 2026 board agendas

Executives should treat fog computing as strategic infrastructure, not an adjunct to cloud programs. Our report recommends the following board‑level actions for 2026:

- Mandate a three‑year fog adoption roadmap with explicit decision points tied to measurable KPIs (latency, uptime, operational cost per site, and business outcome improvements).

- Create a cross‑functional oversight forum (IT, OT, security, procurement, legal) empowered to authorize integration pilots and vendor selection, with monthly reporting cadence.

- Define a standards/compliance budget to fund interoperability testing and third‑party certifications that de‑risk supplier selection.

- Allocate a portion of transformation funding to partner‑led PoCs that include systems integrators and telecom providers to accelerate on‑the‑ground deployments.

Why the full report is essential for procurement and architecture teams

This public brief intentionally focuses on strategic implications and the high‑level competitive context. The full PW Consulting Fog Computing Market Report contains the actionable analytics that procurement, architecture and SRE teams need to convert strategy into repeatable programs: scenario‑based financial models, validated vendor scorecards, deployment playbooks and a detailed risk register tied to standards and regulatory dynamics. These deliverables are designed to reduce time‑to‑value and to make capital allocation defensible to audit and compliance functions.

Next steps

- For enterprise leaders: convene a 90‑day steering committee to assess pilots and vendor shortlist using the report’s procurement playbook.

- For technology officers: request the vendor scorecard and integration checklist to execute side‑by‑side comparisons and interoperability tests during RFP evaluation.

- For risk and security heads: use the report’s security toolkit to map quantum‑resilience requirements into existing cybersecurity roadmaps.

PW Consulting’s full Fog Computing Market Report provides the complete dataset, vendor benchmarking, and implementation artifacts required to operationalize the strategic guidance summarized here. Access to the report and the accompanying implementation workshop schedule is available through our report page; this brief is intended as a provocation and orientation for decision-makers preparing capital and operating plans in 2026.

For detailed analysis of this topic, please visit the official page:Fog Computing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com