Custom Mushroom Mylar Bags Guide for Simple Packaging

Food |

2026-07-07 08:43:26

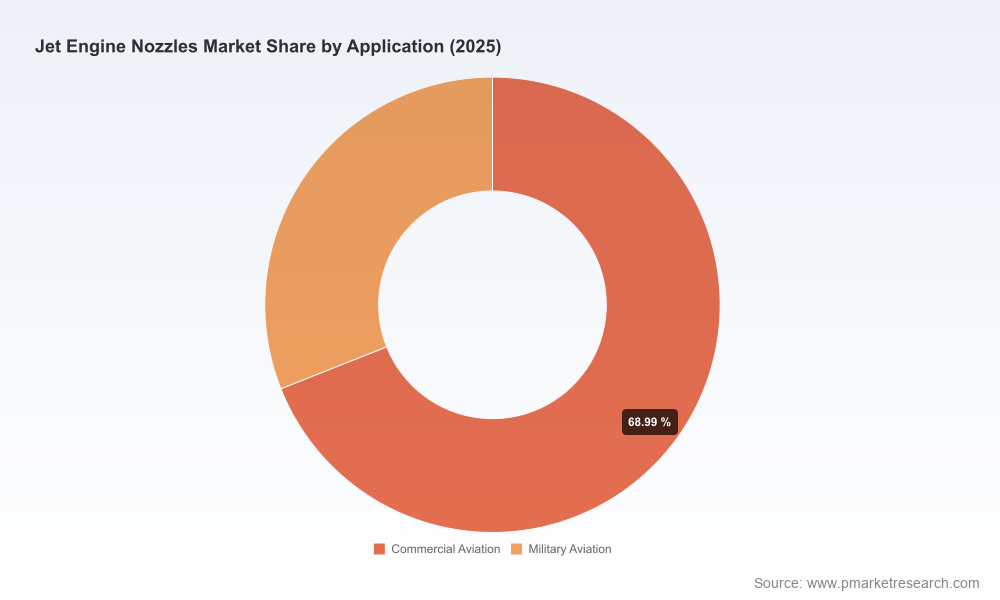

PW Consulting today publishes an executive industry brief that frames the strategic choices aerospace suppliers, OEMs, MRO providers, and Tier‑1 investors must make as the jet engine nozzles market transitions into a new cycle of technology-driven growth. Built from a comprehensive 2020–2025 historical audit and a 2026–2032 forecast, the report surfaces the macro trajectory, structural dynamics, and five actionable decision pathways that will determine who captures value as the market expands at a compound annual growth rate (CAGR) of 5.85%.

Jet Engine Nozzles Market

With jet engine nozzle demand rebounding and re‑shaping under pressures from fuel efficiency mandates, noise regulations, and new propulsion architectures, 2026 will be a year where early strategic moves compound into durable competitive advantages. PW Consulting’s base‑year snapshot (2025) anchors a robust forecast that sees the market grow through 2032, providing commercial clarity for capital allocation, R&D prioritization, and supply‑chain redesign. Our analysis is expressly designed to inform board‑level target setting, procurement negotiations, and M&A screening for the coming 18–36 months.

Jet Engine Nozzles Market

The nozzle market has demonstrated steady growth through the 2020–2025 period and reaches a material inflection point in our 2026 baseline. Under PW Consulting’s central case, the market grows at a 5.85% CAGR across the 2026–2032 forecast window, reflecting durable demand from commercial retrofit cycles, military modernization programs, and next‑generation engine architectures.

Jet Engine Nozzles Market

Market concentration is significant: the top three suppliers control a majority share, while the top five firms capture an even larger portion of total industry revenue. This concentration creates both barriers and opportunities — scale enables investments in additive manufacturing and high‑temperature materials, while specialist suppliers can monetize niche capabilities in repair and aftermarket services.

Raw material and regulatory dynamics are decisive. Nickel‑based superalloys remain foundational to high‑temperature nozzle components, accounting for a dominant share of superalloy demand. Titanium alloys continue to be indispensable where high specific strength and corrosion resistance are required, especially in military applications.

PW Consulting’s full report is structured as an operational playbook rather than a purely academic forecast. Core deliverables include:

Scenario‑based revenue modelling (2026–2032) with sensitivity to fuel price, fleet utilization, and regulatory tightening.

Technology roadmaps mapping nozzle architectures (fixed, convergent‑divergent, variable geometry, thrust vectoring) to engine types and mission profiles, with an emphasis on additive manufacturing, cooling technologies, and noise‑attenuation geometries.

Supply‑chain heat maps identifying single‑source risks in critical materials (nickel superalloys, titanium) and suggested hedging strategies including qualified supplier ramps, long‑lead contracts, and joint‑R&D co‑funding.

Commercial playbooks for Tier‑1s and aftermarket providers covering aftermarket capture strategies, service pricing, turnaround time optimization, and digital inspection adoption.

Company scorecards and capability matrices for key players, with M&A and partnership target lists ranked by technical fit and integration risk.

Regulatory and sustainability impact analysis that connects emissions and noise standards to nozzle design requirements and compliance timelines.

Primary interview excerpts with procurement directors, engine OEM engineers, and MRO decision‑makers, plus a toolkit of Excel models and decision trees for in‑house planning teams.

Our competitive analysis focuses on a set of incumbents and specialists that collectively shape technology development, supply assurance, and aftermarket economics. Key strategic observations include:

GE Aerospace (Cincinnati, Ohio) — Strong momentum in additive manufacturing and cross‑program supply for high‑volume commercial platforms. Its workstreams linked to open‑fan and RISE initiatives position GE as a lead innovator in low‑fuel‑burn nozzle concepts; expect continued investment in AM process qualification to scale production cost‑effectively.

Safran Aircraft Engines / CFM International (Paris/Global JV) — Deep expertise in high‑temperature exhaust components and integration across commercial engine programs. Safran’s joint operations enable platform‑level synergies (engine‑nozzle system optimization) that raise switching costs for airframers and airlines.

Pratt & Whitney (East Hartford, Connecticut) — Focused on turbine and fuel nozzle systems for both military and geared‑turbofan commercial engines. The company’s engine‑integration approach and aftermarket network give it leverage in specification control and lifecycle service economics.

Rolls‑Royce (London) — Material science leadership for large‑diameter exhaust and UltraFan programs, with a premium on advanced alloys and novel cooling schemes. Rolls‑Royce’s long‑haul program exposure makes it a bellwether for widebody nozzle demand trends.

Wall Colmonoy / Aerobraze & Moeller Aerospace — Critical niche players in repair, coating, and precision machining. Their capabilities are essential to MRO resilience and enable cost‑effective life extension of legacy nozzle inventories.

The Lee Company & ITP Aero — The Lee Company’s compact fluid systems and ITP Aero’s thrust‑vectoring nozzles spotlight the diverse technological pathways that suppliers can exploit: component miniaturization and mission‑specific nozzle geometries.

Program showcases and demonstrations continue to accelerate technology adoption. High‑visibility displays of thrust‑vectoring and flat 2D nozzle concepts at defense airshows reinforce the urgency for suppliers to secure design IP and qualification routes.

Academic‑industry partnerships are pushing noise‑reduction concepts toward maturity. Recent R&D on trapezoidal and chevron‑like geometries for supersonic/noise reduction indicates a potential new tranche of nozzle designs tailored for emerging commercial supersonic and low‑boom programs.

OEM program updates highlight that open‑architecture engine efforts include dedicated nozzle innovation streams, creating opportunities for second‑tier suppliers to participate as co‑developers rather than pure manufacturers.

Based on our synthesis, PW Consulting recommends five near‑term strategic moves for industry players preparing 2026 budgets and KPIs:

Prioritize materials strategy: Secure long‑lead agreements or equity partnerships with nickel superalloy and titanium producers, and qualify alternative alloy families where viable. Material continuity is a latent constraint that will shape delivery in high‑temperature nozzle segments.

Invest selectively in additive manufacturing scale‑up: Fund targeted process qualification for nozzle components that unlock reduced part counts and faster repair turnarounds. Focus on thermal‑cycle validation and post‑build heat‑treatment pathways.

Design for serviceability: Integrate modularity and standardized interfaces to capture aftermarket revenue and reduce shop visit time. Digital twins and non‑destructive inspection tool chains should be funded in parallel with hardware redesign.

Form defensive alliances: For mid‑tier suppliers, entering strategic teaming agreements with at least one Tier‑1 OEM and one MRO provider hedges demand volatility and provides a route to scale.

Embed regulatory foresight: Map nozzle design choices against evolving emissions and noise regulations so that product roadmaps proactively meet future compliance thresholds, rather than react to them.

PW Consulting’s full market study contains granular datasets, regional and application splits, segmentation scenarios, and detailed company financial proxies that operational teams use to build investment cases. In keeping with our “trailer” approach, this public brief highlights the analytical framework and strategic conclusions while withholding the detailed sub‑segment tables, supplier share tables, and downloadable modelling assets that are available on the report landing page. These appendices include a downloadable Excel model, supplier scorecards, and a prioritized M&A watchlist designed for immediate use by corporate development and procurement teams.

Leaders preparing 2026 strategy cycles should view this brief as a tactical waypoint: it identifies the inflection points and provides an operational checklist, but the full competitive and quantitative detail lives in the report’s appendices. PW Consulting is scheduling private briefings for boards and corporate strategy teams to walk through the scenario models and bespoke supplier impact analysis. Contact the PW Consulting research desk to request a briefing and access the full report.

For organizations making capital, procurement, or strategic partnership choices in 2026, the decisions you make this year will structurally determine your ability to capture the gains our forecast anticipates. PW Consulting’s Jet Engine Nozzles Market report is designed to make those choices clearer, executable, and defensible.

For detailed analysis of this topic, please visit the official page:Jet Engine Nozzles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com