Why Choosing the Right Legal Help Matters After an Accident

Other |

2026-02-01 04:07:47

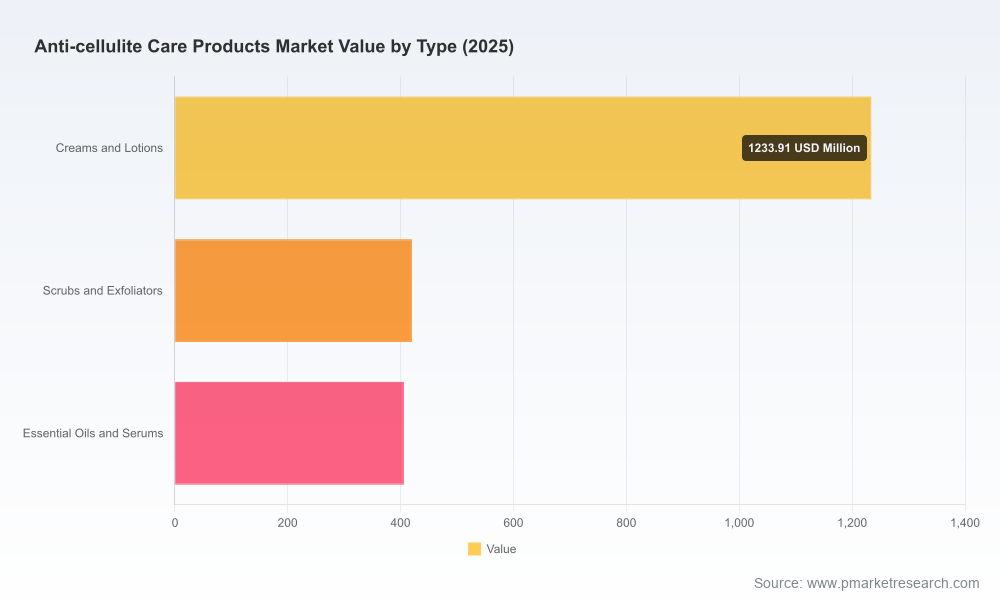

The anti‑cellulite care products market has entered a steady, structurally driven growth phase. After recovering and expanding in the early 2020s, global revenues reached a meaningful milestone in our base year (2025) and are forecast to continue expanding through the 2026–2032 horizon at a compound annual growth rate (CAGR) of 5.01%. By the end of the forecast window, the market is expected to approach roughly USD 2.9 billion. For strategy teams and corporate boards planning actions in 2026, the implications are clear: measured, evidence‑based product investment and differentiated channel strategies will capture disproportionate share while poorly substantiated claims and weak regulatory planning expose firms to reputational and commercial risk.

Anti Cellulite Care Products Market

Our historical analysis shows a steady expansion from the early 2020s through 2025, followed by continued growth across 2026–2032 under baseline assumptions. The 5.01% CAGR embedded in the forecast reflects a combination of sustained consumer interest in body‑contouring cosmetics, growing adoption of premium and natural formulations, and channel dynamics that increasingly favor omnichannel execution. For strategy teams, this trajectory demands three concurrent moves in 2026:

Anti Cellulite Care Products Market

This research is intentionally operational. It is structured to support immediate 90– to 720‑day planning cycles as well as medium‑term portfolio roadmaps. Highlights include:

Anti Cellulite Care Products Market

Note: This preview is intentionally high‑level. The full report contains the underlying tables, regional and application splits, and downloadable financial models required for transaction diligence and launch planning.

The market is populated by a mix of global consumer goods players, prestige skincare houses, and fast‑growing niche brands. Each archetype presents different strategic opportunities and constraints for entrants or incumbents considering expansion in 2026.

Selected company snapshots in the full report provide tactical takeaways. For example, effective use of caffeine and plant extracts across brand tiers demonstrates cross‑segment product architectures; Q10‑based positioning and botanical oils illustrate opposite ends of the efficacy vs. naturalness trade‑off. Recent independent players' commercial traction underscores how a well‑executed product + influencer activation can rapidly deliver sell‑through, but sustaining momentum requires proven repeatability and supply resilience.

Regulators and industry guidance are actively shaping product development and marketing. Safety notices and guidance on specific actives have underscored the need for careful claim framing and adverse event protocols. Both US and EU frameworks limit unsubstantiated structure/function claims and expect cosmetic firms to avoid statements that imply drug‑level effects without corresponding clinical evidence. For 2026 planning, the practical implications are:

Consumer preference is shifting toward formulations that combine demonstrable performance with clean, plant‑forward ingredient decks. High‑interest actives include caffeine, retinol derivatives, and selected botanical extracts; delivery formats span lotions, creams, oils and concentrated serums. The intersection of efficacy claims and sustainability credentials is a battleground: brands that can document ingredient provenance, minimize preservative‑related concerns, and back claims with third‑party testing will secure retailer trust and premium consumer willingness‑to‑pay.

This preview outlines the macro trajectory and the commercial levers that will matter most in 2026. The complete PW Consulting Anti‑Cellulite Care Products Market report provides the granular datasets, regional and application splits, competitive scorecards, and Excel models needed to convert insight into action. If your 2026 plan includes product launches, M&A, channel expansion, or R&D prioritization in this category, the full report will materially reduce time to decision and transaction risk.

For access to the complete market tables, proprietary forecasting model, and the full set of execution templates (including the clinical protocol, retailer activation scripts and acquisition candidate screen), contact PW Consulting to arrange an executive briefing and download the report landing page. The preview above is designed to clarify the strategic choices; the full intelligence set is required to operationalize them.

For detailed analysis of this topic, please visit the official page:Anti Cellulite Care Products Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com