Navigating the HostBooks Ltd Case for Smarter Enterprise Accounting

Other |

2026-07-08 21:39:25

PW Consulting’s latest Fluorapatite Market report — base year 2025, historical coverage 2020–2025, forecast horizon 2026–2032 — provides a decision‑grade synthesis for commercial, policy and investment leaders preparing strategy in 2026. The market is quantified in USD Million and our macro model shows the market expanding from an assessed 845.5 (USD Million) in 2025 to an initial forecast point of 916.74 in 2026, growing at a compound annual growth rate (CAGR) of 4.12% across the 2026–2032 forecast period. These headline metrics frame the choices companies must make this year: where to allocate capital, which partnerships to prioritize, and how to hedge supply and regulatory risk.

Fluorapatite Market

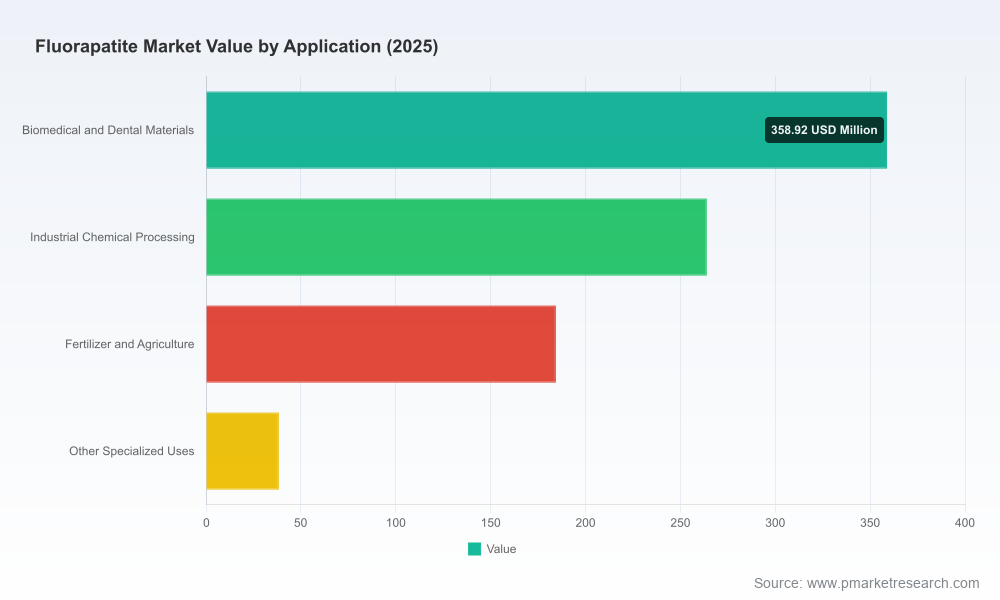

Transitioning demand profiles: End‑market demand for fluorapatite is evolving beyond traditional fertilizer channels into higher‑value specialty applications such as biomedical and dental materials and engineered industrial chemistries. This is creating asymmetric return profiles across producers and processors.

Fluorapatite Market

Supply reshaping: New mine approvals and domestic production initiatives are altering regional supply dynamics. In the U.S., for example, marketable phosphate rock production (primarily fluorapatite) remained material in 2025, prompting policy and investment responses that will affect sourcing and logistics in 2026 and beyond.

Fluorapatite Market

Technological inflection: Scale‑ups of bioactive fluorapatite production signal potential for premium‑priced specialty streams. These technology pathways will bifurcate the market between commodity rock processing and higher‑margin, controlled‑synthesis product lines.

Our top‑line model — calibrated to observed 2020–2025 outcomes and scenario stress tests — projects steady expansion through 2032, underpinned by moderate demand growth and incremental downstream substitution toward specialty uses. The market’s movement from 845.5 (USD Million) in 2025 to 916.74 (USD Million) in 2026 is the first visible manifestation of structural trends that will play out over the forecast window.

Concentration metrics in our analysis indicate a moderately consolidated upstream landscape (CR3 ≈ 42.15%; CR5 ≈ 58.9%). This concentration profile creates both systemic risks and strategic opportunities: while major producers retain scale advantages and logistics control, there is room for targeted entrants and non‑integrated specialists to capture margin by vertical specialization, product differentiation and control of value‑added processing.

Supply resilience and sourcing strategy: With environmental permitting and new mine development shaping availability, companies should pivot from single‑source procurement to a layered sourcing strategy that blends long‑term offtakes with short‑term merchant markets and localized inventory buffers.

Vertical specialization vs. integration: Firms must weigh investments in downstream capabilities (e.g., wet‑process phosphoric acid integration, bioactive synthesis capacity) against the economics of selling higher‑purity product streams into a growing specialty market. Our report contains comparative IRR and payback models for both paths.

Premiumization through technology: Successful scale‑up of bioactive fluorapatite production presents pathways for differentiated products in dental, orthopedic and advanced ceramics markets. Early movers who secure clinical or regulatory milestones can command price premiums and capture durable niche demand.

Regulatory and ESG repositioning: Environmental constraints — habitat impacts, water management and fluorine handling — will increasingly drive permitting timelines and capital allocation. Proactive ESG programs and community engagement can shorten approvals and de‑risk projects.

M&A and partnership playbook: Given the concentration and asset specificity, strategic M&A (acquiring processing technology, specialty producers, or regional mine positions) and structured joint ventures are likely to deliver the best risk‑adjusted access to growth.

The industry comprises a mix of large integrated phosphate miners and fertilizer majors, national champions in resource‑rich jurisdictions, and a scattering of specialty miners and mineral specimen suppliers. Leading firms maintain upstream mine positions and integrated processing assets, giving them scale, logistic advantage and access to commodity revenue streams. Notable participants include global phosphate miners and fertilizer groups that dominate ore supply and downstream conversion, alongside specialist suppliers and processors who serve niche industrial and research markets.

Integrated majors: The largest mining and fertilizer firms continue to leverage scale, long‑term offtake contracts and integrated phosphoric acid production. Their strategic play emphasizes securing feedstock, optimizing conversion efficiency and deploying cost leadership in bulk markets.

National and regional champions: In several producing countries, state‑backed or regionally focused groups concentrate on export and domestic security of supply. Their decisions on capital deployment and export policy materially influence global availability and price volatility.

Specialists and assemblers: A cohort of companies focuses on high‑quality mineral specimens, controlled synthesis and niche downstream products. These players are increasingly relevant where product specification and traceability matter — for example, biomedical applications or high‑purity industrial chemicals.

Our competitive analysis synthesizes public filings, plant footprints and announced investments to map strategic intent across these groups. We then overlay a capability matrix that highlights where each competitor is likely to move: capacity expansion, downstream capture, or technology adoption.

Commercialization of bioactive fluorapatite: Noteworthy scale‑up achievements in bioactive fluorapatite synthesis indicate practical routes to manufacture at commercial volumes — accelerating timelines for specialty product entry and affecting premium markets.

New mine approvals: Regulatory approvals for new phosphate projects have appeared in several jurisdictions, including a major U.S. approval in 2025. These approvals recalibrate medium‑term supply risk and influence near‑term procurement and investment choices.

Mining and processing of fluorapatite are subject to multi‑dimensional environmental and regulatory constraints: habitat disturbance, water usage and fluorine management are recurrent themes in permitting and community engagement. These dynamics increase project timelines and capital intensity. Our risk framework quantifies permitting lead‑time distributions and overlays scenario‑based sensitivity analyses for operating cost impacts under tightening environmental requirements.

For companies planning expansion, the policy environment suggests three actionable mitigations: formalize multi‑stakeholder engagement plans early, invest in lower‑impact processing technologies (water recycling, emissions controls) and design contractual flexibilities to absorb permitting-linked timing shifts.

Robust demand and supply models: Time‑series market sizing from 2020 through 2032, with scenario variants and sensitivity tests focused on commodity and specialty pathways.

Investment calculators: Project-level IRR, NPV and payback templates adjustable by ore grade, capital expenditure, processing route and offtake terms.

Supply‑chain risk matrix: Supplier concentration analysis, logistics bottleneck mapping and inventory optimization playbooks for 12‑ and 24‑month horizons.

Downstream product strategy: Commercialization roadmaps for premium bioactive and specialty fluorapatite products, including regulatory milestone gates and sample go‑to‑market frameworks.

Competitive heatmaps and capability matrices: Strategic positioning and plausible moves for major players and specialist providers, with market entry and defense scenarios.

M&A and partnership playbook: Target profiles, due diligence checklists and integration risk templates tailored to fluorapatite‑centric transactions.

ESG & permitting playbook: Practical mitigation steps, community engagement templates and capital allocation scenarios under differentiated regulatory regimes.

Procurement leaders: Implement layered sourcing with short‑term spot allocations, longer‑dated offtakes and localized inventory nodes to protect production continuity.

R&D and product teams: Prioritize pilot investments in bioactive and high‑purity synthesis routes now to secure first‑mover advantages in specialty applications.

Corporate development: Target bolt‑on acquisitions of specialty processors and offtake positions in jurisdictions with clearer permitting trajectories.

Policy and sustainability teams: Accelerate ESG programs focused on water stewardship and emissions control to reduce permitting risk and shorten time‑to‑market for new projects.

This release highlights the strategic framing and high‑level macro metrics you need to orient 2026 decisions: market size, trajectory and concentration context. The full PW Consulting Fluorapatite Market report contains the granular segment and regional models, supplier scorecards, and downloadable financial templates used to build our scenarios. To review the complete intelligence, including the proprietary split models and detailed company profiles, please visit our report page for subscription and sample extracts.

PW Consulting’s team stands ready to deliver bespoke briefings, customized scenario workshops, and transaction support informed by the report’s granular analytics. For operational implementation assistance or to commission a tailored deep‑dive aligned to your asset footprint or product roadmap, contact our advisory desk.

For detailed analysis of this topic, please visit the official page:Fluorapatite Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com