Home Respiratory Monitor Market — Strategic Briefing for 2026 Decision-Makers

PW Consulting’s new market research briefing on the Home Respiratory Monitor market frames a practical, decision-ready view for executives planning investments, product launches, partnerships, or M&A in 2026. Built on a 2025 base and a 2026–2032 forecast horizon, the report quantifies a sustained growth trajectory (CAGR 8.15%) and documents how the market evolves from approximately USD 2.85 billion in 2025 to an expected USD 4.93 billion by 2032. Market concentration is modest (CR3 ~28.5%; CR5 ~38.2%), signaling a market with meaningful incumbent strength but ample room for challengers and consolidation.

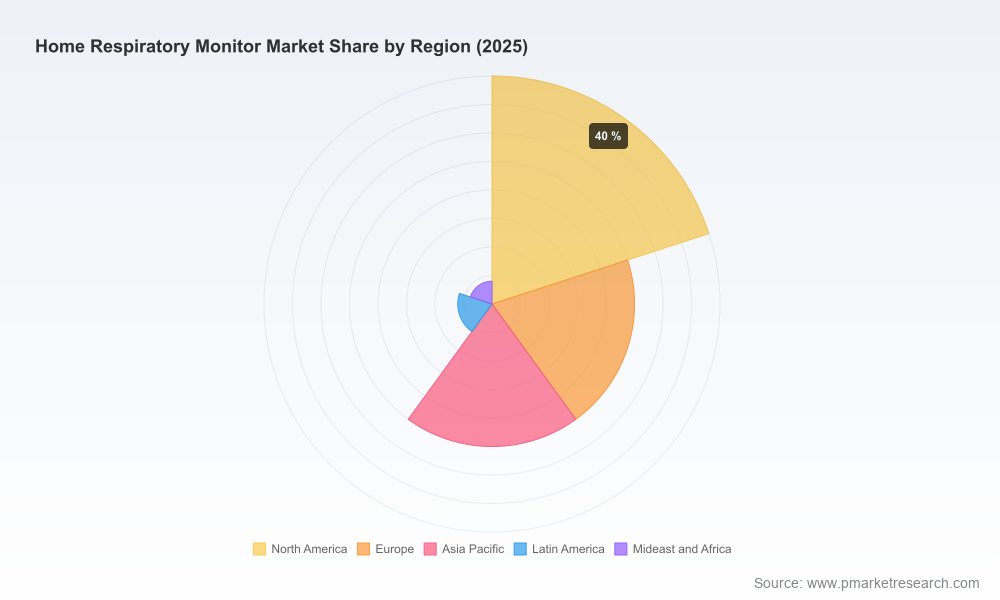

Home Respiratory Monitor Market

Why this briefing matters in 2026

- Actionability: The briefing is structured to convert market intelligence into the tactical plays executives need for the coming planning cycle — product roadmap priorities, reimbursement positioning, partner selection, and M&A triage.

- Policy inflection points: Recent regulatory and reimbursement developments (including the CMS proposed updates in August 2025 and prevailing RPM/RTM billing conventions such as CPT code 98976) materially change commercial economics for remote respiratory monitoring solutions beginning in 2026.

- Evidence-first decisions: Payers and large homecare providers now require clear clinical and economic evidence to scale coverage; the briefing identifies the minimum evidence sets and real-world data strategies that unlock reimbursement and enterprise deployments.

Market dynamics: what is driving growth and how the landscape is shifting

- Demand-side drivers: demographic tailwinds, rising prevalence of chronic respiratory diseases and sleep-disordered breathing, and broader consumer adoption of health monitoring—all supported by telehealth normalization—are sustaining demand.

- Technology convergence: improvements in wearable sensors, home capnography, continuous pulse oximetry, and integrated software platforms are moving respiratory monitoring from episodic testing to longitudinal care models.

- Reimbursement and policy: proposed CMS updates for RPM/RTM beginning in 2026, plus widely used CPT billing pathways, create clearer revenue mechanics for recurring physiologic monitoring—if devices and services meet medical device and documentation requirements under current regulatory guidance.

- Channel evolution: commercial models are shifting toward integrated care bundles (device + connectivity + clinical services). Direct-to-consumer (DTC) remains important for adoption and awareness, but sustainable enterprise growth increasingly depends on payer and provider integration.

- Competitive structure: the market is neither a pure winner-take-all nor fully fragmented. Leading vendors hold important advantages in clinic integration, scale, and reimbursement relationships, while specialists and new entrants compete on sensor differentiation, usability, and data platforms.

Competitive landscape: what incumbents and challengers are doing

- ResMed Inc. (San Diego, CA) — Strengths: integrated patient management platforms and home sleep testing capability. Strategic emphasis should be on extending software-driven care pathways that lock in provider workflows and recurring service revenues. Risk: margin pressure if lower-cost device entrants undercut hardware economics. Opportunity: leverage clinical networks to accelerate bundled service adoption.

- Koninklijke Philips N.V. (Philips Respironics) (Amsterdam) — Strengths: broad sleep and ventilation portfolio with deep clinical relationships. Strategic priority: demonstrate outcomes and total-cost-of-care improvements to maintain reimbursement positioning. Opportunity: product-for-service shifts supported by remote monitoring capabilities.

- Masimo Corporation (Irvine, CA) — Strengths: sensor and bedside monitoring technologies with strong pulse oximetry and capnography IP. Strategic play: capitalize on credentialed sensor accuracy to gain trust in chronic-care remote monitoring. Opportunity: partnerships with homecare providers and payer pilots that reward measurement fidelity.

- Medtronic plc (Dublin) — Strengths: capnography solutions and deep clinical credibility. Strategic actions: package capnography for higher-acuity home settings and to support transition-of-care pathways from hospital to home.

- Fisher & Paykel Healthcare (Auckland) — Strengths: ventilation and humidification for home respiratory support. Strategic focus: service models and consumables recurrent revenue; invest in connectivity and outcome measurement to participate in value-based contracts.

- Nonin Medical (Plymouth, MN) — Strengths: portable oximetry with established reputation for reliability. Strategic path: push into integrated home monitoring platforms and B2B distribution with homecare operators.

- Sunrise (Belgium/USA) and Snap Diagnostics (USA) — Strengths: focused home sleep testing sensor solutions. Strategic niche: fast, low-friction diagnostic pathways and DTC-to-clinical handoffs. Opportunity: convert diagnostic users to long-term monitoring subscribers.

Taken together, these profiles show differentiated plays: platform incumbents are defending integrated workflows and recurring revenue; sensor specialists compete on precision and cost; and niche diagnostic vendors pursue conversion funnels into chronic care. The overall competitive posture favors partnerships (technology + clinical service providers) and bolt-on acquisitions that fill gaps in connectivity, clinical workflows, or evidence generation.

Home Respiratory Monitor Market

What the report contains — practical, executable deliverables

- Market sizing and forecasts (historical 2020–2025; base year 2025; forecast 2026–2032) with modeled scenarios tied to reimbursement and adoption inflection points.

- Market concentration and competitor scorecards (CR metrics, capability heatmaps, go-to-market archetypes).

- Regulatory and reimbursement playbook: device classification guidance, RPM/RTM billing pathways (including CPT considerations), and payer engagement templates.

- Commercial readiness checklists: clinician onboarding, device provisioning, patient adherence programs, and support staffing models.

- Clinical-evidence blueprints: trial designs, real-world evidence (RWE) protocols, and outcomes metrics that payers and networks require.

- Dealmaking toolkit: M&A selection filters, valuation sensitivities tied to recurring revenue multiples, and integration risk matrices.

- Proprietary Excel models and scenario dashboards that allow you to stress-test product, pricing, and coverage assumptions without exposing segment-level proprietary figures in this public briefing.

Strategic implications & recommended 2026 actions (prioritized)

- 1. Immediate reimbursement readiness — Update clinical documentation, device labeling, and billing workflows to align with the post-2025 RPM/RTM code landscape. For organizations that have not built billing infrastructure, consider rapid partnerships with RPM vendors or third-party billing specialists.

- 2. Evidence-first commercialization — Allocate budget in 2026 for one or two focused RWE pilots with payers or integrated delivery networks that measure utilization, hospitalization avoidance, and patient adherence. Use those pilots to create reusable dossiers for payers.

- 3. Product prioritization and modularization — Segregate product investments between core clinical-grade sensing (accuracy, reliability) and peripheral user-experience features (apps, notifications). Clinical-grade wins payer trust; UX wins volume in DTC.

- 4. Channel and partnership strategy — Pursue partnerships with home healthcare providers and telehealth platforms to accelerate deployments. For new entrants, prioritize a few high-value payer or provider partners rather than broad DTC spend.

- 5. Pricing tied to outcomes — Pilot outcome-based pricing for defined cohorts (e.g., COPD transition-of-care or sleep-disordered breathing) to de-risk payer adoption and differentiate from device-only offers.

- 6. M&A and bolt-ons — Use small acquisitions to fill gaps in software, connectivity, or service delivery capability. Target assets that accelerate time-to-revenue (customer contracts, proven patient engagement tech, or clinical decision support modules).

- 7. Data and interoperability — Invest in standards-based data pipelines (FHIR, secure APIs) to integrate with EHRs and third-party care management systems; this is increasingly a must-have for enterprise sales.

- 8. Risk mitigation — Monitor policy updates and ensure product compliance with medical device definitions for RPM/RTM billing. Build regulatory timelines into product-release roadmaps to avoid commercialization delays.

A final word on timing and next steps

The home respiratory monitoring market is entering a phase where commercial success will be decided less by single-product features and more by the strength of integrated propositions: recognized measurement fidelity, payer-aligned clinical evidence, and operationalized service delivery. The market’s projected rise (from roughly USD 2.85 billion in 2025 to nearly USD 4.93 billion by 2032 at an 8.15% CAGR) rewards timely, evidence-based plays in 2026. Given the market concentration profile, there remains substantial opportunity for differentiated specialists to scale rapidly through partnerships or targeted M&A.

Home Respiratory Monitor Market

This briefing is a synthesis of our complete market study — designed to be a trusted, executable roadmap for 2026 planning. The full report contains confidential segment-level models, company scorecards, and downloadable financial templates that operational teams and deal teams use during negotiations. To access the full datasets, proprietary segmentation, and the Excel model, please visit the PW Consulting report landing page or contact our industry practice team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Home Respiratory Monitor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com