Airborne Mission Management System Market: Strategic Imperatives for 2026 — PW Consulting Preview

As defence and special-mission aviation programs transition to more distributed, sensor-rich architectures, airborne mission management systems (AMMS) are moving from bespoke stovepipes to modular, software-defined mission ecosystems. PW Consulting’s upcoming market research release offers executive teams a pragmatic playbook for 2026 decision-making: it synthesizes observed market dynamics, technology and regulatory inflections, supplier positioning, and investment levers that determine program success over the next funding cycle.

Airborne Mission Management System Market

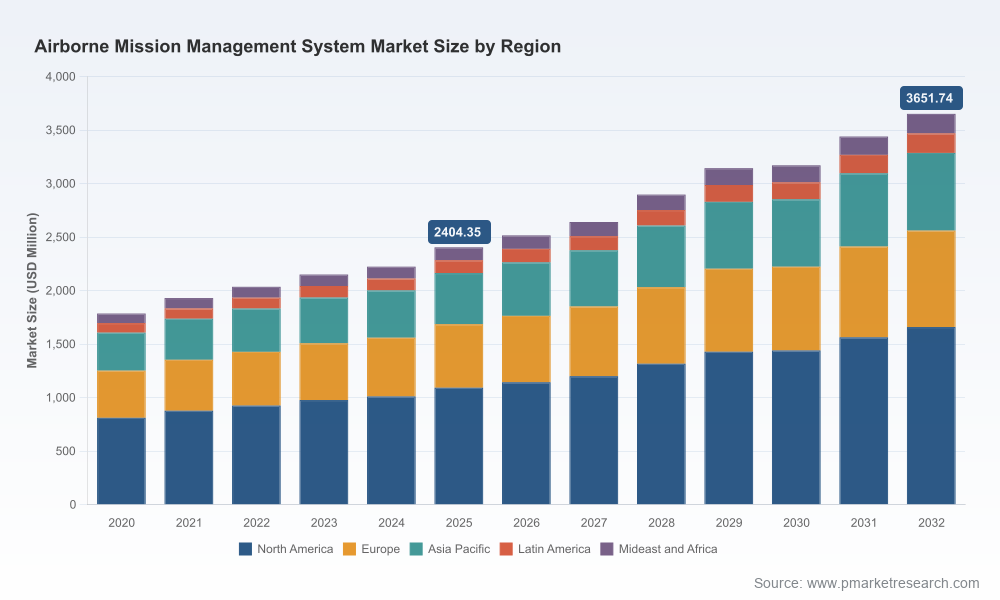

Market snapshot (base year 2025; forecast to 2032)

Our analysis uses 2025 as the base year and assesses historical evolution (2020–2025) before projecting through a 2026–2032 forecast horizon. The global Airborne Mission Management System market expanded from approximately USD 1,785 million in 2020 to roughly USD 2,404 million in 2025. Under the scenarios modelled in this report, we project continued growth to an estimated USD 3,652 million by 2032, representing a compound annual growth rate (CAGR) of about 6.15% across the forecast period.

Airborne Mission Management System Market

Why this matters for 2026 corporate strategy

- Budget cycles and program awards in 2026 will be driven by modernization priorities—platform-common mission processing, MOSA-compliant architectures, and certification-ready software baselines. Firms that can articulate a credible MOSA roadmap will shorten procurement timelines and reduce integration risk.

- Growth is steady but selective. A mid-single-digit CAGR means volume opportunities exist, but share gains will come from differentiated capabilities (sensor fusion, low-SWaP rugged computing, cyber-hardened mission processors) and validated certification pathways, not from broad price competition alone.

- Certification and traceability are a gating factor. Compliance with DO-254/DO-178C and alignment to ARP4754A processes materially affects time-to-field and lifecycle costs; organizations that embed certification planning during design will capture more downstream value.

- Market concentration favors established primes and specialists. The market exhibits moderate concentration (CR3 approximately 48.5%; CR5 approximately 62.3%), underscoring that a handful of incumbents command a meaningful share while a competitive mid-tail of niche specialists continues to innovate.

Report highlights — what PW Consulting delivers (actionable, not academic)

- Decision-ready market sizing and scenario models: granular forward scenarios (baseline, accelerated modernization, and constrained-budget cases) that translate market growth into program-level demand signals for 2026 procurement and 3–5 year roadmaps.

- Investment prioritization framework: a risk-adjusted matrix ranking technology bets (e.g., MOSA middleware, AI-enabled fusion, low-SWaP processors, secure comms) by time-to-value, certification burden, and addressable market.

- Integration & procurement playbook: contract design options (fixed-price vs. IDIQ, sustainment-led vs. capability-led acquisition), RFP evaluation checklists, and sample acceptance criteria that link technical deliverables to certification artefacts.

- Supplier diligence pack: vendor scorecards, red/green flags for strategic partnerships, and recommended diligence questions for JV/technology acquisition discussions.

- M&A and partnership scenarios: valuation sensitivities for target classes (system integrators, sensor-fusion middleware vendors, rugged computing specialists) and integration traps that commonly erode synergy value.

- Operationalization templates: product roadmaps, test & integration timelines, and a certification traceability checklist aligned to DO-178C/DO-254 expectations to reduce schedule risk during flight test and qualification.

- Executive briefings and tailored workshops: a suite of deliverables to align product, commercial, and BD teams for rapid response to 2026 RFIs/RFPs.

Competitive landscape — who to watch (strategic profiles)

- Curtiss-Wright Defense Solutions (Ashburn, VA, USA): Offers AMMS and mission processors for high-end UAVs and manned platforms with a strong pedigree in rugged, MOSA-friendly computing. Recent contract awards demonstrate traction in naval UAV programs and legacy-system derivatives—important evidence of prime-level integration credibility.

- General Dynamics Mission Systems — Canada (Ottawa, Canada): Positions as a full-spectrum integrator for fixed/rotary-wing and unmanned platforms with strengths in ISR, ASW and secure data-fusion solutions. Their participation in platform modernization contracts highlights ability to combine systems engineering with fielded support.

- Saab AB (Linköping, Sweden): Brings non-flight-critical C2 and mission management suites designed for AEW, MPA and rotary platforms, emphasizing mission flexibility and multi-role adaptability—relevant for customers prioritizing mission-agnostic solutions.

- BIRD Aerosystems / Ondas (Israel, acquired by Ondas): Their MSIS AMMS and ISR suites (now part of Ondas) underscore how strategic acquisitions accelerate capability infusion—particularly in multi-mode radar and EO integration for special-mission aircraft.

- Leonardo (Rome, Italy): Focused on aircraft and mission management systems for rotary platforms, delivering end-to-end data acquisition and mission orchestration—an incumbent with deep platform OEM relationships.

- Honeywell Aerospace (Charlotte, NC, USA): Supplies mission management workstations and crew-centric situational awareness solutions for tactical mapping and special operations—leveraging avionics and human-system integration strengths.

- Thales Group (Paris, France): Integrates mission management with sensors and C2 backbones for complex naval/defence airborne missions—notable for systems-level integration across domains.

Recent deal and program signals (validated by primary sources)

- Curtiss-Wright won a material IDIQ award in mid-2025 to supply airborne mission processors derived from legacy AMMS lines for a high-profile UAV program—evidence of demand for upgrade paths that re-use proven software baselines.

- In early 2026, a modernization contract involving General Dynamics Mission Systems — Canada highlighted national-level procurement activity around platform life-extension using modern mission management suites.

- Strategic consolidation accelerated in 2026 with Ondas’ acquisition of BIRD Aerosystems, signaling buyer appetite for integrated ISR + mission management portfolios that shorten customer acquisition of multi-sensor capabilities.

Regulatory and technical dynamics that will shape 2026 decisions

- Certification regimes remain pivotal: DO-254 (hardware) and DO-178C (software) continue to be the certification backbone for airborne mission systems where airworthiness is required. Programs that neglect certification early incur schedule and cost penalties.

- MOSA momentum: U.S. DoD MOSA policies are steadily raising the bar for modular designs—suppliers must show clean interfaces, well-documented APIs, and upgrade pathways to remain competitive on DoD recompetes.

- Systems engineering standards: ARP4754A alignment remains a requirement for safety-critical integrations and should be embedded within contract Statements of Work and acceptance criteria.

- Hardware constraints: High-performance rugged computing with low SWaP continues to be a bottleneck. Solutions that balance compute density, thermal management, and certifiability will unlock platform-agnostic scalability.

Practical recommendations for 2026 program plans

- For OEMs and primes: Prioritise MOSA-aligned reference architectures and supplier ecosystems that can demonstrate certification artefacts. Keep a two-track roadmap: near-term modernization deliverables and a mid-term transition to software-defined core processing.

- For component and middleware vendors: Invest in certifiable toolchains and test suites that reduce buyers’ integration and qualification effort. Offer ‘certification acceleration’ packages as a commercial differentiator.

- For integrators and service providers: Build rapid-fusion demonstrators that prove multi-sensor interoperability and cyber-resilience—successful demos materially shorten contract negotiation cycles.

- For investors and M&A teams: Target firms that provide mission-level software stacks, rugged low-SWaP compute nodes, or proven data-fusion modules. Value targets by their certification readiness and customer footholds rather than pure R&D pipelines.

- For procurement teams: Embed certification milestones and interface control document (ICD) delivery into contract milestones, and prefer flexible award structures that allow incremental capability insertions.

How PW Consulting supports executive decisions

Our full report equips leadership with the quantitative models, supplier due diligence, and executable playbooks necessary to convert market growth into durable program wins. PW Consulting offers tailored briefing packages, scenario workshops, and vendor negotiation support designed to shave months off procurement timelines and reduce integration exposure.

Airborne Mission Management System Market

Next steps

This preview outlines the strategic context and practical imperatives that 2026 program owners cannot ignore. For the full dataset, segmentation breakdowns, supplier scorecards, contractual templates, and the detailed scenario models that underpin our recommendations, access the complete PW Consulting Airborne Mission Management System Market report. The full report includes proprietary segment-level intelligence, procurement-ready templates, and an interactive forecast model—content intentionally withheld from this preview to preserve client value and support direct engagement.

Contact PW Consulting to schedule a briefing and receive the complete report customized to your program, region, or technology focus.

For detailed analysis of this topic, please visit the official page:Airborne Mission Management System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com