Solid State Transformers Market Insights and Growth Trends

Other |

2026-06-29 12:26:09

As municipal utilities, industrial operators, and defense installations prepare budgets and procurement plans for 2026, PW Consulting’s latest Wastewater Level Sensors Market report delivers the market intelligence required to convert uncertainty into competitive advantage. Anchored on a 2025 base year and a 2026–2032 forecast window, the study quantifies a market that surpassed USD 1,000 Million in 2025 and is projected to continue expanding at a compound annual growth rate (CAGR) of 7.45% through 2032, when total revenue is forecast to approach USD 1,700 Million (USD, revenue in Million). This briefing summarizes the report’s strategic value to executives while preserving the detailed segment-level datasets available in the full release.

Wastewater Level Sensors Market

Regulatory pressure is intensifying. Proposed and emerging regulations (including recent EPA proposals and sectoral guidance) are increasing monitoring frequency and data granularity requirements for wastewater and stormwater discharges. These requirements are driving demand for robust, reliable level-sensing platforms that integrate with compliance and reporting workflows.

Wastewater Level Sensors Market

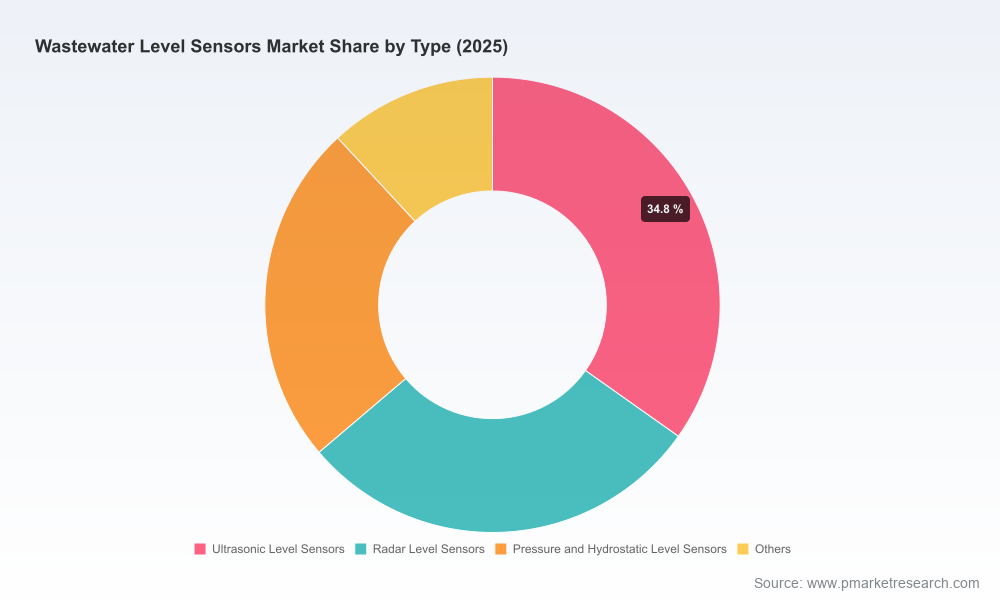

Operational expectations are shifting toward digitalization and real-time control. Smart-city investments and digital water programs prioritize non-contact sensing (ultrasonic, radar) and integrated telemetry to minimize maintenance and maximize uptime in challenging wastewater environments.

Wastewater Level Sensors Market

Supply-side constraints are material. Semiconductor shortages and volatility in piezoelectric and rare earth inputs are elevating cost and lead-time risk for several sensor technologies, requiring procurement teams to factor supply resilience into 2026 sourcing strategies.

Market structure favors both established OEMs and specialist innovators. Consolidation trends and the presence of high-capability incumbents create an environment where partnership, product differentiation, and service-led value capture are critical.

Robust market sizing and forecasting methodology — transparent assumptions, scenario variants, and sensitivity testing tailored to 2026 planning cycles.

Vendor benchmarking framework — capability heatmaps, product-technology alignments, go-to-market models, and a strategy roadmap for supplier selection and negotiation.

Technology landscape and adoption playbooks — strengths/weaknesses of ultrasonic, radar, and hydrostatic approaches, integration requirements for SCADA/IMS, and recommended pilot designs for rapid validation.

Procurement and contract templates — lead-time risk clauses, performance SLAs, spare-parts planning, and inventory hedging strategies designed to mitigate raw-material volatility.

Regulatory-impact assessment — jurisdictional risk matrices, compliance pathways, and recommended sensing specification updates to align with near-term monitoring mandates.

TCO models and ROI calculators — lifecycle cost comparisons that include installation, maintenance, downtime risk, and analytics/telemetry value capture.

Implementation checklists and field-validation protocols — practical steps to accelerate deployment while preserving data integrity and operational continuity.

The market exhibits a mix of global instrument OEMs, specialist sensor manufacturers, and systems integrators. Market concentration metrics indicate that the top three vendors collectively account for a meaningful but not dominant share (CR3 ~32.4%), while the top five increase concentration further (CR5 ~46.8%). The implication for procurement and strategy teams is clear: suppliers command differentiated technical and service value, but substantial opportunity remains for targeted entrants and local integrators.

Xylem Inc. (Washington, DC, USA) — Offers integrated measurement and control solutions across water and wastewater infrastructure. Strengths: systems integration, service networks, and a broad product portfolio that supports treatment-plant and lift-station deployments. (https://www.xylem.com)

Endress+Hauser Group (Reinach, Switzerland) — Established in process instrumentation with specific products for clarifiers, pumping stations, and sludge monitoring. Strengths: industrial-grade transmitters and lifecycle services. (https://www.endress.com)

VEGA Grieshaber KG (Schiltach, Germany) — Noted for high-frequency radar sensors and submersible transmitters tailored to sewage and stormwater contexts. Strengths: high-performance radar platforms and ruggedized submerged sensors. (https://www.vega.com)

KROHNE Messtechnik GmbH (Duisburg, Germany) — Supplies radar transmitters for contactless measurement in pumps, basins, and open channels. Strengths: industrial sensor engineering and established process-automation partnerships. (https://www.krohne.com)

Flowline Inc. (Los Alamitos, CA, USA) — Focused on municipal wastewater applications, especially for raw sewage vaults and lift stations. Strengths: application-specific sensor designs and retrofit-friendly solutions. (https://www.flowline.com)

Pulsar Measurement (Malvern, UK) — Ultrasonic transducers and radar sensors for tank monitoring and pump control. Strengths: modular product offerings and service-focused deployments. (https://pulsarmeasurement.com)

SJE-Rhombus (Detroit Lakes, MN, USA) — Provides continuous level sensors and float switches used in residential to municipal settings. Strengths: proven mechanical reliability and cost-effective control devices. (https://www.sjerhombus.com)

ABB Ltd. (Zurich, Switzerland) — Delivers ultrasonic and laser-based transmitters for lift stations, clarifiers, and digesters, with strengths in automation integration. (https://new.abb.com)

Siemens AG (Munich, Germany) — Offers hydrostatic and ultrasonic options with strong SCADA/controls integration capabilities for large treatment plants. (https://www.siemens.com)

APG Sensors (Logan, UT, USA) — Focused on water-and-wastewater sensor solutions aimed at efficiency and sustainability initiatives. (https://apgsensors.com)

Together, these vendors illustrate the market’s dual dynamics: established industrial suppliers prioritize reliability and systems integration, while specialized manufacturers deliver niche performance and rapid innovation. For buyers, the optimal strategy often combines products from both cohorts to balance performance, cost, and service coverage.

Trade shows remain a key innovation and partnership channel: major exhibitions (e.g., WWETT, WEFTEC) continue to showcase incremental sensor innovations and integrated monitoring platforms, signaling active product development and buyer engagement.

Regulatory developments — including proposed EPA monitoring expansions and defense-sector operational directives — are directly influencing sensor specifications and procurement cycles. Agencies are emphasizing traceability and more frequent reporting, which raises the bar for sensor reliability and data integration.

Raw-material and component constraints (semiconductors, piezoelectric materials, rare earths) are amplifying procurement risk. Lead times and unit costs are more volatile than in previous planning cycles, which matters materially for multi-site roll-outs planned in 2026.

Embed supply-resilience criteria in RFPs: require transparent BOM traceability, dual-sourcing strategies, and supplier commitments on lead times and substitution protocols.

Pilot-first deployments for non-contact sensors: run focused pilots that validate performance under site-specific fouling, aeration, and foam conditions before committing to wide-scale roll-outs.

Adopt lifecycle TCO over unit-price metrics: include maintenance intervals, downtime costs, telemetry and analytics integration, and spare-parts availability in procurement decision models.

Prioritize modular, upgradeable platforms: select sensor technologies that can evolve with telemetry, edge analytics, and remote calibration to protect future value and enable progressive automation.

Coordinate regulatory-aligned specifications: ensure sensor selection supports anticipated monitoring frequency and reporting formats to minimize retrofit costs when new regulations take effect.

Explore strategic partnerships: consider co-development, volume guarantees, or strategic inventory programs with OEMs to secure favorable terms amid raw-material volatility.

Use scenario planning: leverage the report’s scenario outputs to stress-test CapEx and OpEx plans against optimistic and constrained supplier environments and regulatory tightening.

PW Consulting’s Wastewater Level Sensors Market report is designed as an executable playbook for 2026. Executives and procurement leads will find the report immediately useful for budgeting, supplier selection, piloting, and regulatory compliance road-mapping. The full study includes downloadable TCO tools, vendor scorecards, procurement templates, and segmented datasets that support granular decision-making — information we intentionally withhold from this preview to drive direct engagement with the full deliverable.

To access the complete dataset, scenario dashboards, and tailored advisory services for implementing the recommendations summarized here, visit our report page or contact PW Consulting’s industry advisory team. For organizations preparing CapEx and operational plans for 2026, acting on these insights now will materially reduce execution risk and position teams to capture the operational and compliance benefits of smarter level sensing.

— PW Consulting, Senior Strategic Advisory & Industry Analysis Team

For detailed analysis of this topic, please visit the official page:Wastewater Level Sensors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com