Your Guide to Understanding Liposuction in Riyadh from Consultation to Recovery

Health |

2026-06-01 12:26:45

As healthcare providers and med-tech executives prepare strategic plans for 2026, PW Consulting’s latest Arthroscopy Irrigation Pumps Market report delivers the forward-looking intelligence required to convert opportunity into sustainable growth. This briefing highlights the tactical value of the full report for board-level decisions, product roadmaps, commercial strategy, and M&A screening — while preserving the report’s proprietary subsegment detail to encourage direct engagement with the full study.

Arthroscopy Irrigation Pumps Market

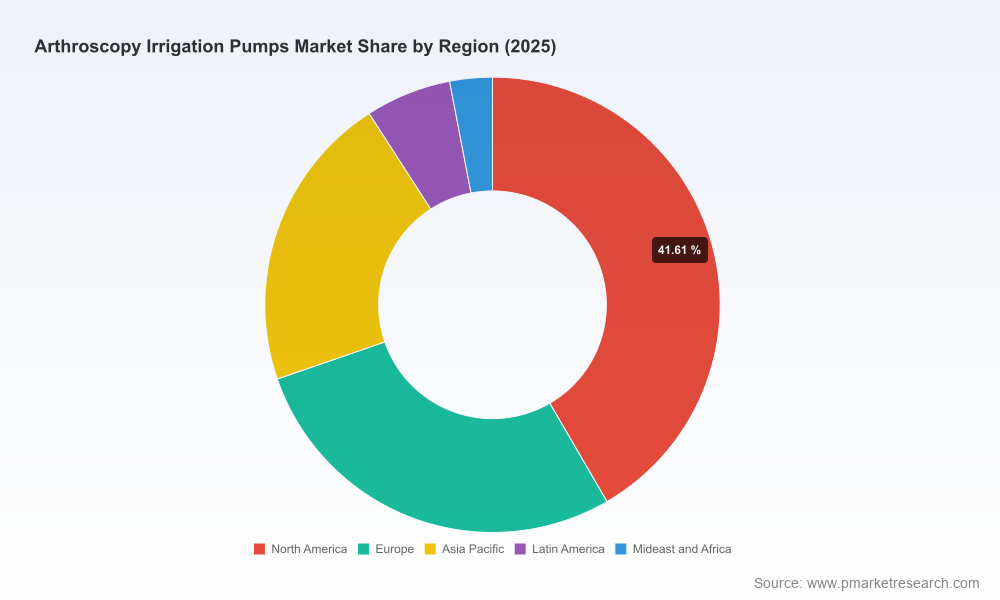

After a period of moderate volatility through the early 2020s, the global arthroscopy irrigation pumps market has re-established steady expansion. Our analysis uses 2025 as the base year and models a 6.2% compound annual growth rate across the 2026–2032 forecast period. That trajectory underpins a meaningful expansion of the market’s absolute size over the forecast window, reflecting a mix of clinical adoption, technology substitution (toward electronic fluid management), and favorable reimbursement and regulatory dynamics in key healthcare systems.

Arthroscopy Irrigation Pumps Market

Market concentration metrics underscore the competitive reality: the top three manufacturers account for approximately two-thirds of market value (CR3 ~65%), and the top five capture more than four-fifths (CR5 ~82%). For incumbents and new entrants alike, these figures signal that differentiated offerings and targeted route-to-market strategies are decisive.

Arthroscopy Irrigation Pumps Market

Actionable commercial playbooks: Go-to-market strategies tailored for hospitals, ambulatory surgery centers, and OEM partners — including procurement/tender tactics and effective value-communication for sterile processing and OR stakeholders.

Regulatory and reimbursement navigators: Stepwise guidance for 510(k)/MDR compliance, clinical evidence strategies, and how recent Medicare policy trends alter adoption economics for arthroscopy fluid management systems.

Technology and product benchmarking: Comparative assessment frameworks that rank pump platforms on criteria such as flow control fidelity, visualization integration, ease of use, sterilization workflows, and service economics — enabling product roadmap prioritization.

Commercial risk assessments: Supplier resilience analysis, price erosion scenarios, and scenario-based revenue projections that quantify downside and upside exposures for 2026 planning.

M&A and partnership playbooks: Due-diligence checklists, integration risk profiles, and synergy quantification templates oriented to both strategic acquirers and financial sponsors targeting the med-tech space.

Clinical adoption and training models: Best-practice programs to accelerate OR adoption and reduce time-to-first-case, including ROI calculators that link pump performance to case throughput and visualization quality.

Regulatory pressure and market access: Arthroscopy fluid management systems are regulated as arthroscope accessories under FDA 21 CFR 888.1111, and EU MDR requirements have raised compliance costs. Our report maps the regulatory pathways and evidence expectations that determine time-to-market and post-market surveillance burdens.

Reimbursement tailwinds: Recent favorable shifts in Medicare reimbursement for arthroscopic procedures have reduced adoption friction in certain procedural categories. The result: an environment where capital purchases of integrated visualization and fluid management systems can be justified on throughput and quality metrics.

Technology substitution: Electronic, closed-loop fluid management platforms are gaining clinical preference over manual and gravity-fed options due to improved joint distension control, visualization consistency, and OR efficiency. The full study quantifies adoption curves and timing for elective markets versus emerging geographies.

Consolidation and supplier strategy: High CR3/CR5 ratios indicate an oligopolistic core market. This has compressed margins in commoditized tiers while expanding the premium segment for integrated systems with visualization and analytics features.

The market is characterized by a mix of large global med-tech incumbents, specialist European OEMs, and regional manufacturers serving price-sensitive segments. Our report provides decision-useful competitor intelligence on product positioning, channel footprints, and recent strategic moves. Highlights include:

Arthrex, Inc. (Naples, FL) — Known for Continuous Wave™ and DualWave™ pump platforms that emphasize precise joint distention and integrated fluid management. Arthrex’s move into next-generation integrated fluid/visualization systems (noted in May 2025) signals a deliberate push upmarket into systems-level OR solutions; competitors should expect further bundling around visualization and instrumentation.

Stryker Corporation (Kalamazoo, MI) — Offers cross-functional pump platforms incorporating both inflow/outflow control and battery-operated flexibility. A notable contract win with a major U.S. health system (March 2025) reflects Stryker’s strength in enterprise-level contracting and its ability to leverage clinical integration capabilities to secure scale deployments.

Smith & Nephew plc (London, UK) — Offers inflow/outflow pump solutions designed for sport medicine workflows, with a focus on consistent debris removal and OR efficiency. Its positioning emphasizes serviceable consumables and sports-medicine channel relationships.

CONMED Corporation (Utica, NY) — Markets high-performance systems with customizable presets and reliability claims that appeal to high-volume orthopedics centers. CONMED’s strategy draws on configurable workflows and aftermarket service agreements to build stickiness.

Richard Wolf GmbH & KARL STORZ — European-focused vendors that leverage broad endoscopy portfolios to cross-sell pump systems as part of integrated endoscopic suites. Their strengths are systems integration and long-standing clinical relationships in EMEA.

Hemodia SAS (France) — A vertically integrated pump manufacturer with a demonstrated regional presence and a focus on cost-effective, in-house produced platforms that can support national sales strategies in Europe.

Advin Healthcare & JD Meditech (India) — Regional manufacturers focused on cost-competitive offerings for emerging markets and price-sensitive procurement channels. Their presence illustrates a bifurcated market: premium integrated systems versus lower-cost, high-volume alternatives.

Product strategy: If you are an incumbent, prioritize modular integration with visualization and telemetry features to protect margin and defend against commoditization. If you are a challenger, target niches defined by procurement constraints or unmet clinical workflows and build credible service propositions.

Commercial strategy: Enterprise contracting and bundled procurement represent the shortest path to scale in developed markets; focus commercial resources on health system procurement leadership and clinical champions to accelerate adoption.

Regulatory and clinical evidence planning: Start evidence generation early. For 2026 approval and reimbursement planning, manufacturers should align 510(k)/MDR timelines with clinical outcomes studies that demonstrate throughput and visualization benefits — the metrics that most influence hospital purchasing committees.

M&A and partnerships: Consider tuck-ins that add software analytics, imaging integration, or service capabilities. Our model-driven M&A templates quantify likely payback periods under conservative and aggressive adoption scenarios.

Emerging markets playbook: Combine lower-cost hardware with locally optimized service models. Regional OEMs demonstrate that price-performance balance and local regulatory agility can unlock volume outside the most consolidated geographies.

PW Consulting’s market model synthesizes historical shipment data (2020–2025), supplier revenue disclosures, primary interviews, and clinical adoption metrics. The forecast period (2026–2032) uses a blended approach combining top-down macro drivers and bottom-up adoption curves by hospital type and clinical application. Scenario-sensitivity testing — including a conservative low-adoption and an accelerated uptake case — is provided in the full report to stress-test strategic options.

For executive teams, the value of this analysis is immediate: it translates macro growth (anchored on a 6.2% CAGR across the 2026–2032 horizon) into operational choices — from R&D prioritization to sales territory design and M&A screening. The high concentration of market share among the leading vendors magnifies the return on precise positioning: small differences in feature set, clinical evidence, or contracting approach can produce outsized share shifts.

PW Consulting’s study is designed as a decision-ready toolkit: strategic recommendations, executable go-to-market plays, and proprietary scenario models that quantify the economics of alternative choices for 2026 and beyond.

To preserve the competitive value of our proprietary segmentation and subsegment revenue breakdowns, detailed regional splits, and granular application sizing (the elements that most directly inform investment and bidding decisions), those datasets are available exclusively in the full report and online portal.

If your board is preparing budget allocations, product roadmaps, or M&A pipelines for 2026, schedule a briefing with PW Consulting to obtain the full report, interactive model files, and a tailored executive workshop that maps findings to your strategic priorities.

Contact our Strategic Markets team to request the full study, confidential briefings, or bespoke scenario analyses that translate market growth and competitive dynamics into a 12–36 month action plan.

For detailed analysis of this topic, please visit the official page:Arthroscopy Irrigation Pumps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com