https://www.facebook.com/AlphaRockSupplementforED

Art |

2026-05-20 09:42:01

As organizations recalibrate product portfolios, supply chains and capital plans for 2026, the carbon thermoplastic market presents a distinct strategic inflection point. PW Consulting’s latest market study—anchored on a 2025 base year and a 2026–2032 forecast horizon—finds that the global market has accelerated from a mid-single billion-dollar base in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 8.5%, reaching roughly USD 3.45 billion (million USD units) by 2032. This press briefing summarizes the study’s most decision-relevant findings and the implications every executive should consider before allocating resources in 2026.

Carbon Thermoplastic Market

Demand inflection from electrification and lightweighting: The structural shift toward electric vehicles (EVs), next-generation aerospace platforms, and high-performance industrial applications continues to expand the addressable market for carbon fiber reinforced thermoplastics (CFRTP). However, demand is now intersecting with new supply-side constraints and regulatory pressures that will materially affect margins and time-to-market in 2026.

Carbon Thermoplastic Market

Supply-chain and cost volatility: Raw material dynamics—most notably an 8% uptick in PAN precursor prices in late 2025—coupled with lingering freight surcharges and geopolitical trade measures, have made input costs less predictable. These headwinds amplify the value of procurement agility and localized production strategies.

Carbon Thermoplastic Market

Technology and recyclability are differentiators: Advances in thermoplastic resin systems and processing methods are enabling higher-rate production and circularity claims (e.g., recyclability certifications showcased at industry forums). Firms that can demonstrate validated recyclability and lower lifecycle emissions will secure premium positions with OEMs and regulators.

PW Consulting’s market model traces steady historical growth through 2025 and forecasts an 8.5% CAGR over 2026–2032. Under this trajectory, the market moves from an estimated USD 1,950 million in 2025 to roughly USD 2,234 million in 2026, then continues to the mid-single billion range by the end of the forecast period. This expansion is broad-based across mobility, aerospace and high-end industrial applications—but not uniform. Our scenario work shows that technology adoption curves, regulatory shifts and regional supply responses will produce materially different outcomes for companies depending on timing and strategic posture.

Market sizing and rigorous forecasting methodology: Transparent base assumptions, scenario envelopes (base, upside, downside) and sensitivity analyses tied to raw material and freight cost swings.

Go-to-market playbooks: Actionable commercial and technical pathways for OEMs, tier suppliers and material producers, including fast-follower tactics and first-mover strategies.

Supplier benchmarking and capability matrices: Comparative analysis of technology readiness, throughput economics, and application-specific performance across leading producers.

Risk and regulatory tracker: Real-time mapping of tariff regimes, chemical regulation impacts and trade frictions—paired with mitigation templates for procurement and policy teams.

M&A and partnership targets: Shortlists of strategic targets and fit/gap analyses for consolidation, capacity plays and IP acquisitions—scored against synergies and integration risk.

The market exhibits moderate concentration, with the three largest companies accounting for a meaningful portion of capacity and the top five nearly half of the market. That concentration creates both bottlenecks and opportunities: incumbent leaders can leverage scale to secure OEM qualification wins, while challengers can exploit niche applications and regional dynamics to carve defensible positions.

Toray Industries (Tokyo): A leading technology and volume player, Toray’s continued product introductions geared to mass automotive production underline its strategy to capture EV-related demand. Their early mover advantage in automotive-grade prepregs remains a core competitive asset.

Syensqo (formerly Solvay’s CFRT business) (Alpharetta, GA): Recent capacity expansions targeting EV platforms reflect a transport-focused growth play—an offensive move to convert EV chassis and structural budgets into thermoplastic solutions.

Teijin Limited (Tokyo) and Mitsubishi Chemical Group (Tokyo): Both combine materials science depth with application engineering, pushing higher-performance matrices (PA, PEEK) for demanding industrial and aerospace users. Certification and qualification wins underscore their route-to-market discipline.

Arkema (Colombes) and Hexcel (Stamford): These players are differentiating on resin innovation and production throughput, respectively—Arkema through recyclable resin systems and Hexcel through thermoplastic prepreg solutions designed for high-rate aerospace assembly.

SGL Carbon, Gurit, PlastiComp and Lingol: Each firm occupies targeted positions—automotive exterior tapes, wind and marine prepregs, long-fiber compounds, and pellet/preform supply for high-volume molding. Their partnerships with OEMs and tier suppliers demonstrate the ecosystem nature of CFRTP adoption.

Product launches and certifications are accelerating time-to-production: Notable examples include a high-rate automotive prepreg launch from a major carbon fiber producer in late 2025 and certification milestones from Tier material suppliers in 2025—both signals that technical barriers are being lowered.

Capacity additions focused on EV demand show how materials players are aligning with OEM roadmaps. These expansions have the potential to rebalance regional supply chains in the near term.

Brand-to-OEM partnerships—exemplified by tape/vehicle platform collaborations—are evolving from pilots to platform-level commitments, shortening cycle times for qualification when design intent and material supply are co-developed.

Raw material swings: PAN precursor cost pressures in late 2025 increased cost pass-through risk for carbon fiber producers. Buyers should incorporate raw-material hedging or long-term offtake mechanisms into sourcing strategies for 2026.

Regulatory tightening: Updated chemical regulations in jurisdictions such as the EU have constrained certain flame retardants, affecting some high-temperature thermoplastic formulations. Compliance-driven reformulation projects will require lead time and engineering resources.

Trade and transport frictions: Tariff adjustments and continued freight surcharges on key shipping lanes are reshaping landed costs—pushing some OEMs to nearshore or dual-source critical compounds.

Processing constraints: High-temperature matrices (e.g., certain PEEK systems) remain limited in high-volume settings because of processing temperature demands and equipment cost. In many cases these systems will stay concentrated in aerospace or research applications unless processing innovations reduce thermal barriers.

Embed material cost scenarios into product roadmaps: Adopt a two-track valuation model that ties design decisions to raw-material and freight scenarios; trigger points should dictate when to switch suppliers or scale production.

Prioritize qualification vs. volume: For OEMs, lock in qualification early with a select set of suppliers to secure capacity; for suppliers, align qualification pipelines with targeted OEM platform launches to avoid orphaned investments.

Invest in processing R&D and circularity: Funding pilot lines that reduce processing temperatures or enable recyclability will pay dividends as regulators and customers demand lifecycle performance.

Consider regional capacity plays: Nearshoring or partnerships with local compounders can mitigate tariff and freight volatility; use small-scale replication facilities to prove economics before committing to large greenfield investments.

Use M&A and strategic alliances selectively: Acquire targeted capabilities (e.g., pelletization, preform tooling, resin IP) to accelerate time-to-volume; pursue partnerships with OEM integrators to convert application designs into repeatable production programs.

For executives allocating capital and choosing partners in 2026, the critical questions are these: Do you control the technical route to qualification for your highest-value platforms? Have you stress-tested your bill of materials against plausible raw-material and freight shocks? Can your processing pathways scale without creating unacceptable thermal or throughput bottlenecks? Our report provides the diagnostic tools—scenario models, supplier scorecards and tactical playbooks—to answer these questions with confidence.

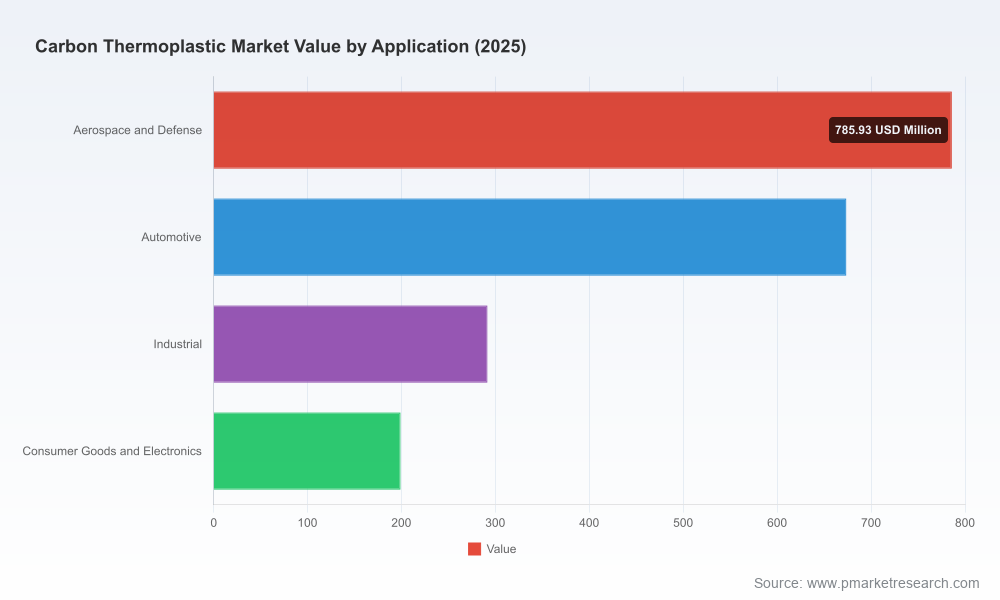

PW Consulting’s Carbon Thermoplastic Market report offers both the strategic framing and the operational instruments needed to convert market growth into sustainable competitive advantage. To preserve the commercial value of our proprietary segmentation and company-level scorecards, detailed regional and application-level splits have been reserved for the full report. For teams preparing 2026 budgets and strategic roadmaps, that granular intelligence is essential.

Clients and subscribers can access the complete report—containing segmentation detail, supplier benchmarking, M&A target lists and downloadable models—via PW Consulting’s publication portal. Contact our industry team to schedule a briefing and a customized deep-dive workshop that aligns the report’s insights to your strategic priorities for 2026.

For detailed analysis of this topic, please visit the official page:Carbon Thermoplastic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com