Long-Term Skin Benefits of Committing to Electrolysis Hair Removal

Health |

2026-05-07 13:00:50

PW Consulting’s new Offshore Wind Turbine Market report (base year 2025) synthesizes market-scale forecasting, supplier benchmarking, and actionable execution playbooks to support high‑stakes decisions in 2026. Against a backdrop of accelerating turbine scale, supply‑chain stress and shifting U.S. regulatory posture, the offshore wind turbine market is entering a phase where timing, partner selection and manufacturing footprint choices will materially determine project returns and competitive position. This release is a “trailer” for the full analysis: we demonstrate the depth and methodology you need to trust our findings while intentionally reserving the proprietary segment tables and granular regional breakouts for report subscribers.

Offshore Wind Turbine Market

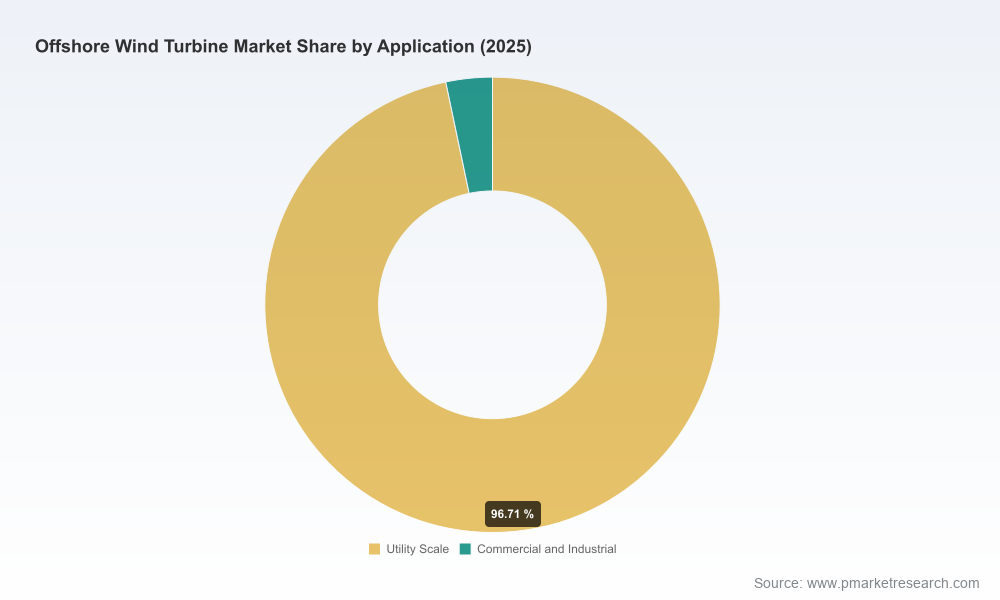

Macro dynamics are stark. The global offshore wind turbine market has moved from an early‑adopter growth base to a rapid expansion phase: our model shows the market expanding from roughly USD 15.2 billion in 2020 to about USD 38.6 billion in 2025, with a near‑term inflection as larger turbines and floating foundations scale. Under our forecast (2026–2032), the market is projected to grow at a compound annual growth rate (CAGR) of 13.5%, reaching roughly USD 93.5 billion by 2032. That cadence creates a concentrated runway of procurement, manufacturing and financing opportunities for firms that position themselves correctly in 2026.

Offshore Wind Turbine Market

With market volume expanding rapidly, procurement windows and conditional optioning of capacity materially affect pricing and delivery. Buyers that lock staged options with OEMs and reserve follow‑on slots in 2026 can reduce delivery uncertainty and capex escalation. The report provides decision trees that quantify the trade‑off between earlier contracting and option premium versus the exposure to rising component prices.

Offshore Wind Turbine Market

Decisions between fixed and floating foundations, and between direct‑drive and semi‑direct drive platforms, have cascading impacts on port infrastructure, transportation and O&M profiles. We show where floating solutions create multi‑decade upside for developers pursuing deeper‑water leases, and where fixed solutions still dominate near‑term cost‑effective deployments — while noting which technology vectors are most sensitive to steel and specialty alloy pricing.

Given projected steel demand and logistics complexity, OEMs and developers that secure local fabrication capacity and port staging nodes reduce schedule risk and tariff exposure. The report’s siting toolkit helps quantify breakevens for in‑country fabrication versus import strategies under multiple tariff and lease‑delay scenarios.

Regulatory developments — including major reviews and temporary lease pauses — can stop pipeline cashflows overnight. We provide stakeholder maps and playbooks for market participants to engage regulators, shape environmental and national‑security narratives, and accelerate permitting in jurisdictions where in‑country manufacturing or energy security arguments are persuasive.

Project financing in 2026 must combine adaptive tranche structures (to bridge prototype certification risk of larger turbines) with covenant packages that reflect supply‑chain concentration. Our investor pack shows how to structure returns under scenarios where certification or lease delays shift commissioning windows by 12–36 months.

The marketplace is competitive but not atomized. Concentration metrics indicate a moderate degree of OEM aggregation (top‑three share under 50% and top‑five above 60%), leaving room for both established OEM scale and aggressive challengers to alter share dynamics through technology or commercial innovation.

Recent corporate moves illustrate two concurrent market dynamics: (1) an arms race on turbine size and drivetrain architectures, and (2) geographic expansion and certification efforts that will reshape procurement options in 2026. Examples include GE Vernova gaining certification clearance for larger prototypes mid‑2025, Ming Yang expanding its European footprint in late 2025, and Goldwind ramping component production for ultra‑large turbines by year‑end. These developments reinforce the need for 2026 strategies that evaluate both incumbent reliability and emerging technology economics.

Two hard constraints dominate the near term: raw materials and regulatory uncertainty. Steel — which can constitute up to 90% of a turbine’s mass — is a structurally dominant input. US offshore pipeline planning over the next two decades implies multi‑billion‑dollar domestic steel demand, and this backdrop elevates the strategic value of secure supply contracts and local fabrication agreements. Our supply‑chain modules quantify exposure by project and supplier pathway and provide mitigations such as multi‑tier sourcing, forward hedges and strategic stockpiles.

Regulatory churn is the other critical variable. In 2025–2026 several jurisdictions have opened thorough reviews of offshore wind policy frameworks and, in some cases, paused leases for national‑security and permitting reasons. These actions create binary outcomes for project pipelines: expedited versus delayed. The report lays out regulatory‑stage scenario matrices and suggested advocacy approaches for private‑sector actors to reduce the probability and impact of stop‑work events.

For executives making 2026 decisions, the Offshore Wind Turbine Market report from PW Consulting delivers a synthesis of macro forecasting, supplier benchmarking, execution playbooks and regulatory scenario models that convert market noise into executable strategy. The market’s rapid expansion and the concurrent material risks around raw materials and regulation mean that a small set of early, well‑structured actions (manufacturing footprint, procurement cadence, and regulatory engagement) will disproportionately determine outcomes over the next five years.

To access the full data tables, regional and application breakouts, and the proprietary supplier scoring model that underpins the analyses summarized here, visit PW Consulting’s report landing page and download the executive package. The full report contains the granular inputs and sensitivity models you will need to finalize budgets, partner selections and board recommendations in 2026.

For detailed analysis of this topic, please visit the official page:Offshore Wind Turbine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com