What Is Xtreme HD IPTV and Is It Worth Your Time? A Real Look at the Service

Networking |

2026-06-27 06:55:09

PW Consulting today releases the Pfsa Ionomer Market study — a forward-looking strategic briefing designed to underpin executive decisions through 2026 and beyond. Drawing on an expanded dataset spanning 2020–2025 (base year 2025) and a detailed forecast to 2032, the report synthesizes market dynamics, supply-chain tensions, competitive positioning, and practical commercial playbooks for firms operating across fuel cells, electrolyzers, chlor-alkali, sensors, and related electrochemical systems.

Pfsa Ionomer Market

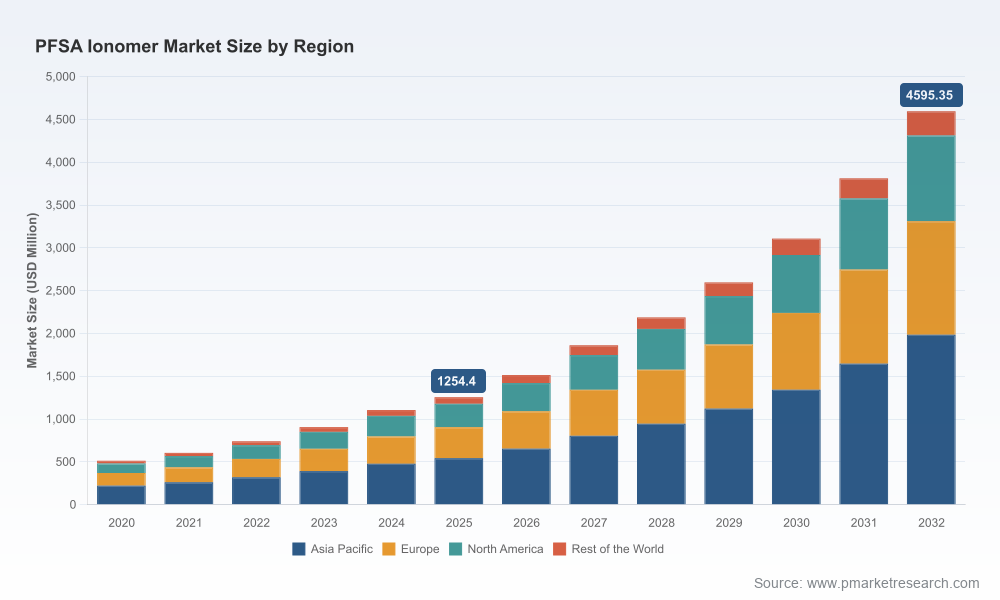

The PFSA ionomer market has transitioned from a niche specialty-chemical space into a scale market aligned with the energy transition. Total global revenue increased materially between 2020 and 2025, and our modeling projects continued acceleration through the forecast horizon.

Pfsa Ionomer Market

PW Consulting’s baseline: the PFSA ionomer market expands at a robust forecast CAGR of 20.38% during 2026–2032, driven by rapid electrification of mobility, accelerated electrolytic hydrogen capacity deployments, and ongoing industrial electrolysis demand.

Pfsa Ionomer Market

At the aggregate level, the market moves from a mid‑three‑figure Million USD base in 2020 to a low four‑figure Million USD by 2025 and is forecast to scale to multi‑billion USD levels by 2032 under our base case. (Full time‑series and scenario tables are provided in the report.)

Market structure is concentrated: the top three players account for a substantial majority of supply; the top five capture nearly nine in ten dollars of revenue — a dynamic that creates both capacity risk and opportunity for differentiated entrants.

Timing of capacity investments: with double‑digit CAGR dynamics continuing into the late 2020s, near‑term capacity expansions will be decisive. Companies that align capex with realistic offtake (and that secure upstream monomer feedstock) will capture disproportionate share as demand scales.

Supplier risk and consolidation: the market concentration profile means supplier selection is not only a cost negotiation — it is a strategic bet. Firms should structure dual‑sourced supply corridors, evaluate toll‑manufacturing partnerships, and explore strategic equity or JV relationships with established PFSA producers.

Regulatory & ESG calculus: PFAS regulatory pressure in North America and Europe, and high‑visibility corporate commitments (including exits by legacy PFAS players in prior years), are reshaping access and permitting risk. Sustainability and end‑of‑life strategies for ionomers are quickly moving from “nice to have” to commercial imperatives — especially for OEMs selling hydrogen solutions into regulated markets.

Raw material and feedstock exposure: Tetrafluoroethylene (TFE) remains the primary upstream monomer for PFSA synthesis. Recent sector analysis points to a growing and increasingly valuable TFE market; procurement strategies for 2026 should factor in price volatility, capacity constraints, and long lead times for fluoropolymer feedstocks.

Our competitive review profiles incumbent PFSA producers and advanced materials specialists. Leading firms have differentiated along three axes: materials science (membrane/ionomer chemistry and side‑chain architecture), product form and formulation (membrane sheets vs dispersions vs solid resins), and applied system integration (electrode inks, MEA supply chains, and end‑use testing). Key players highlighted in the report include established fluoropolymers producers and high‑tech specialty chemical houses with global footprints.

Chemours: a leading commercial name with a long‑standing Nafion™ portfolio. Recent public developments — including published research on sustainable end‑of‑life targets and significant government grant participation — position the company as a technology and policy‑engaged incumbent.

Syensqo: brings an articulated short‑side‑chain chemistry for high‑performance fuel‑cell and electrolyzer use cases; their product breadth spans membranes, dispersions, and solid forms aimed at performance‑sensitive OEMs.

AGC Chemicals and Asahi Kasei: two major Japanese players focused on integrated supply and application‑grade membranes for hydrogen and electrolysis markets, leveraging industrial scale and regional customer relationships.

Dongyue Group: a vertically integrated supplier with growing presence in Asia — important for buyers seeking regional cost and logistics advantages.

Importantly, the industry is not static: public‑funded demonstrations, academic‑industry publications, and targeted grant programs (including multi‑million USD awards supporting hydrogen value chains) are accelerating applied innovation and enabling new business models (recycling, membrane recovery, aftermarket services).

Demand drivers: PEM fuel cells and water electrolysis are the primary commercial pull for PFSA ionomers. Growth in heavy‑duty mobility, stationary power, and green hydrogen projects underpins demand growth and shortens lead times for technical validation.

Product form and value capture: dispersions and formulated solutions often command higher near‑term margin because they embed formulation and integration services (ink development, electrode coatings). Commodity‑style resin forms can scale volume but compete on price — a tradeoff that should inform route‑to‑market choices.

Supply‑chain fragility: concentrated upstream feedstock markets (TFE) and regulatory headwinds create episodic supply constraints. Scenario planning for 2026 must therefore include contingency sourcing, forward purchase agreements, and recycled‑content strategies where technically feasible.

Recycling and circularity: technical pathways for membrane recovery are maturing. Corporates that invest in lifecycle infrastructure early (pilot recycling, take‑back schemes, or catalyst recovery) will mitigate reputational and regulatory risk while unlocking secondary raw‑material streams.

PW Consulting’s Pfsa Ionomer Market report is designed as an operator’s toolkit as much as an analyst’s study. The deliverables span:

Time‑series market model (2020–2032) with base, upside and downside scenarios, enabling dynamic sensitivity testing for capex and revenue outcomes.

Supply‑chain heatmaps identifying critical nodes (feedstock, intermediate processing, specialty tonnage), plus risk scores and mitigation playbooks.

Competitive benchmarking: techno‑commercial profiles for incumbents, innovation watchlists, and acquisition target screening criteria tailored for strategic or financial buyers.

Commercial playbooks for OEMs and raw‑material buyers — from procurement contracting templates (price and supply clauses) to formulation partnership blueprints.

Regulatory and ESG impact assessment with decision matrices for siting, permitting, and product stewardship in regulated geographies.

Case studies and go‑to‑market scenarios for entrants — including licensing, tolling, JV, and captive manufacturing strategies — with projected ROI timelines under multiple demand trajectories.

Board and investment committees: use the report’s scenario outputs to validate timing of series spending and to stress‑test return profiles under feedstock and regulatory shocks.

Commercial teams: leverage the channel and formulation cues to prioritize customers and define premium offerings (e.g., high‑performance dispersions with integrated maintenance contracts).

R&D leaders: prioritize roadmap items with near‑term commercialization lift (durability, recycling, catalyst‑binding chemistries) while staging more speculative platform investments.

M&A and corporate development: the concentration profile indicates attractive bolt‑on opportunities for producers seeking scale or for integrators aiming to secure supply; PW Consulting’s target scorecards accelerate screening and valuation alignment.

We combine a granular, bottom‑up technology assessment with macro demand modeling and deal‑oriented commercial frameworks. The report deliberately bridges lab performance to factory economics and policy risk — translating material science into boardroom‑grade investment guidance. In keeping with a “trailer” approach, this release highlights strategic insights while reserving the detailed segment tables, regional and application splits, and granular supplier pricing models for the full report.

Executives, investors, and procurement leads planning 2026 strategy cycles should request the full Pfsa Ionomer Market report to access the detailed time‑series datasets, regional and application allocations, supplier scorecards, and our proprietary scenario models. The complete deliverable includes downloadable Excel models, supplier due‑diligence packs, and an implementation playbook tailored to executive timelines.

For licensing, enterprise distribution, or bespoke briefings (including wave‑planning for capital projects, joint‑venture diligence, or product‑form strategy), contact PW Consulting’s Pfsa practice through our official report page. The full report contains the detailed commercial and segment intelligence intentionally omitted from this briefing to preserve the integrity of client decision advantage.

For detailed analysis of this topic, please visit the official page:Pfsa Ionomer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com