How The Keyword Demand Surges

Other |

2026-06-19 09:34:37

As companies prepare budgets and product roadmaps for 2026, PW Consulting’s latest Benchtop Power Supplies Market report delivers the focused, actionable intelligence senior executives need to convert market signals into strategic advantage. The global benchtop power supplies market, which we measure with 2025 as the base year, is on a steady trajectory — with a compounded annual growth rate of 6.42% across our 2026–2032 forecast horizon. From a practical viewpoint, this trajectory translates into expanding addressable demand and evolving customer expectations for programmability, efficiency and integrated data telemetry. This briefing summarizes the report’s strategic value, highlights the dynamics that will shape vendor and buyer choices next year, and outlines the specific decisions the full report is designed to support.

Benchtop Power Supplies Market

Our market model, built on historical data (2020–2025) and forward-looking scenarios (2026–2032), shows a resilient market expanding at mid-single-digit CAGR. For corporate leaders this implies: (1) predictable revenue expansion that justifies targeted R&D and go-to-market investments, (2) sufficient runway for late-cycle consolidation and select inorganic plays, and (3) growing importance of margin protection as competition intensifies around features and services.

Benchtop Power Supplies Market

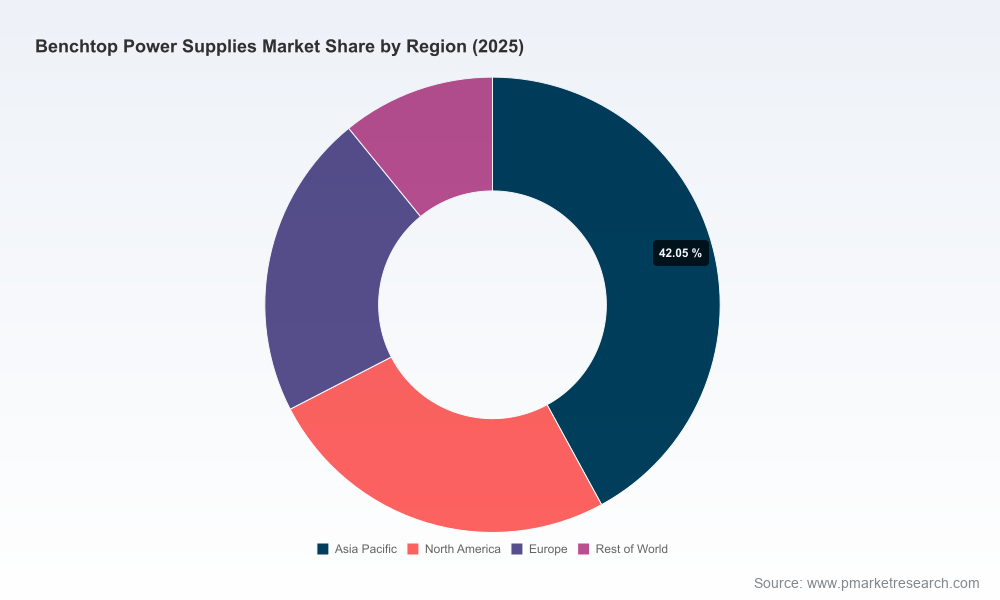

The market concentration profile is noteworthy: top-three vendors collectively hold a meaningful but not dominant share of market value, and top-five providers control around half of the market. In practice, this means scale matters — but there remain clear openings for differentiated competitors that can combine technology, service and channel reach.

Benchtop Power Supplies Market

Efficiency and safety standards are tightening. The IEC 62368-1 safety standard’s energy-efficiency emphasis and recent regulatory updates (e.g., tighter RoHS lead limits in Europe) are forcing design rework and certification timelines into 2026 product roadmaps. Firms that front-load compliance into their NPI process avoid late-stage redesign costs and accelerate time-to-market.

Component and input-cost volatility is re-shaping BOM choices. Raw material and component movements — from copper price upticks to a notable decline in SiC MOSFET costs — are creating simultaneous cost headwinds and performance opportunities. Lower SiC pricing, for example, enables smaller, more efficient switch-mode designs that can be marketed at improved power density or margin. Conversely, higher copper costs are increasing the cost of magnetics and transformer-dependent linear designs.

Labor and calibration capacity are strategic bottlenecks. Faster wage inflation in manufacturing and skilled-assembly segments increases the value of modular designs, test automation and outsourced calibration networks. Companies that invest in scalable service architectures will reduce unit cost escalation and improve after-sales margins.

Product feature competition has moved beyond raw power. Buyers now evaluate programmable telemetry, multi-channel synchronization, remote management interfaces, and data-logging as baseline expectations for R&D and production test labs. Vendors that package hardware with software-enabled workflows capture higher ASPs and recurring revenue opportunities.

The market encompasses a mix of established test & measurement incumbents, specialized power system manufacturers, and agile regional suppliers. Key vendor archetypes and examples include:

Test & measurement incumbents focused on lab ecosystems: Companies known for instrument breadth and lab automation capabilities are differentiating on software integration, instrument interoperability and data-centric features. Recent product introductions and quad-output models from such firms underscore a push to capture higher-value bench workflows.

Precision linear specialists: Vendors with a heritage in high-precision linear regulation continue to serve automated test and characterization applications where low-noise performance is essential. Web-enabled remote-control upgrades are appearing as part of their product evolution.

High-power modular suppliers: Firms offering modular and scalable benchtop power architectures are targeting industrial and high-power test benches, emphasizing continuity-of-operation and simplified system integration.

Value-oriented regional players: Aggressive feature-to-price propositions, rapid product refresh cycles and channel depth in education and small-lab segments are hallmarks of several regionally headquartered vendors.

Notable recent developments that signal near-term competitive behavior:

This report is built as a decision-support toolkit rather than an academic exercise. Key operational deliverables included are:

Days 0–30: Rapid risk triage. Use the supplier risk heatmap and the regulatory tracker to identify immediate supply-chain and compliance risks. Re-prioritize near-term procurement windows and initiate long-lead buy decisions where needed.

Days 30–90: Tactical product and channel moves. Apply the product-roadmap templates to freeze 2026 NPI scopes: decide which product lines require SiC-enabled switch-mode upgrades, which need web/remote-control retrofits, and which should be migrated toward modular, serviceable architectures. Simultaneously, engage top-channel partners with revised margin and service plans to accelerate refresh cycles.

Feature-led premiumization: Package hardware with telemetry, automated calibration options and software workflows to justify ASP premiums and enable subscription-style service models.

Component arbitrage and design pivot: Capitalize on declining SiC prices to redeploy R&D budget toward higher-efficiency switch-mode lines while insulating linear legacy lines through value-added services.

Supply-chain resilience over lowest-cost sourcing: Build regional calibration and assembly capacity or contractual buffer-stock arrangements to mitigate wage and materials inflation.

Selective inorganic moves: Target acquisitions that fill software, telemetry or high-power modular gaps rather than chasing volumetric scale alone.

PW Consulting’s analysis combines primary interviews with OEM product teams, survey data from end-user labs and ATE managers, teardown cost workstreams, and supply-side intelligence. The report uses 2025 as the base year, tracks historical performance from 2020–2025, and models three plausible demand scenarios across 2026–2032. Our quantitative outputs are underpinned by bottom-up BOM models, channel shipment tallies and validated pricing ladders; qualitative judgments are informed by vendor roadmaps and recent product announcements.

This article highlights the strategic contours that will define buying, sourcing and product decisions in 2026. To preserve the tactical value for subscribers and decision-makers, detailed regional and application segmentation tables, granular pricing ladders, revenue-by-product matrices and downloadable financial models are reserved for the full report. Those elements are essential if you intend to perform competitive benchmarking, target account sizing, or investment due diligence.

In an environment where efficiency standards, component economics and software-enabled test workflows converge, disciplined scenario planning and rapid tactical moves will separate winners from laggards in 2026. PW Consulting’s report equips executives with the frameworks, risk maps and financial tools required to make those calls with confidence.

For detailed analysis of this topic, please visit the official page:Benchtop Power Supplies Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com