Web Content Management Market Opens New Opportunities for Enterprises

Other |

2026-06-01 08:33:23

PW Consulting’s forthcoming Industrial Ammonium Sulfate Market report provides a pragmatic, decision-focused guide for executives operating across chemicals, water treatment, specialty manufacturing and industrial supply chains. The global market—measured at USD 612.45 Million (base year 2025)—is projected to continue expanding through the next planning cycle, reaching an elevated market footprint under a medium-growth trajectory supported by a 4.62% compound annual growth rate (forecast period 2026–2032). This briefing outlines the strategic value the full report delivers for 2026 planning without disclosing the granular segment tables and regional detail that remain exclusive to subscribers.

Industrial Ammonium Sulfate Market

Margin & pricing sensitivity: Feedstock volatility (ammonia, sulfuric acid) and trade policy shifts have introduced persistent price dispersion across markets. Understanding structural drivers—rather than spot movements—will be decisive for procurement and commercial teams preparing 2026 budgets.

Industrial Ammonium Sulfate Market

Supply-chain resilience: Ongoing consolidation in major producing markets and byproduct sourcing dynamics (notably caprolactam-related streams) necessitate proactive supplier diversification and contingency planning to avoid operational disruption.

Industrial Ammonium Sulfate Market

Regulatory risk & compliance: Updated emissions and manufacturing standards in key jurisdictions increase compliance expenditures and can create localized capacity shifts; legal, EHS and operations leaders must align capital plans accordingly.

M&A and capacity allocation: Moderate market concentration—indicative CR3 and CR5 metrics show meaningful but not intractable market power among leading manufacturers—creates tactical opportunities for bolt-on acquisitions, joint ventures, and asset rationalization strategies.

Feedstock and production pathways. Ammonium sulfate production continues to bifurcate between direct synthesis (ammonia + sulfuric acid) and byproduct flows (notably from caprolactam and certain coke-oven operations). Global production base remains substantial, led by integrated chemical platforms that can flex outputs based on feedstock economics. For 2026, companies that can dynamically route intermediates and leverage captive sulfur/ammonia positions will sustain cost advantages.

Trade flows and tariff environment. Recent policy developments have left ammonium sulfate more insulated than some upstream inputs: import tariff exemptions in certain major markets have helped maintain trade fluidity, while tariffs on ammonia and sulfuric acid in some jurisdictions increase the implicit landed cost of derivative production. Procurement teams must treat tariff and rules-of-origin shifts as a recurring variable in supplier contracts and hedge structures.

Regulation & emissions. The April 2026 updates to hazardous air pollutant standards in the U.S. create new compliance thresholds for inorganic chemical and agricultural chemical producers. Facilities with older emission-control infrastructure face potential permitting delays or capital-intensive retrofit obligations; conversely, early adopters of best-practice emissions management can exploit differentiation in supply negotiations.

Consolidation and caprolactam-based supply. Environmental and dual-carbon policies in key producing countries are accelerating consolidation among smaller producers and shifting share toward byproduct-origin supplies from larger integrated chemical players. Market entrants and downstream buyers should reassess long-term counterparty concentration and the operational resilience of caprolactam-linked supply chains.

The industrial ammonium sulfate arena is anchored by established chemical multinationals and regional specialists. PW Consulting’s competitive assessment synthesizes company profiles, route-to-market approaches, and strategic posture to highlight where bargaining power, technology, and geographic reach intersect.

BASF SE (Ludwigshafen) — Operates through integrated chemical platforms with global logistics and a focus on industrial-grade products for water treatment and commodity industrial processes. BASF’s advantage lies in scale and networked distribution, enabling flexible allocation between domestic and export markets.

Evonik Industries AG (Essen) — Focuses on specialty and industrial grades, often leveraging byproduct streams. Emphasis on sustainable production and customer-specific formulations creates higher-margin opportunities in regulated end uses.

LANXESS (Cologne) — Positions ammonium sulfate within a broader intermediates portfolio, concentrating commercial efforts where integrated European-Asian supply chains and technical service add value.

AdvanSix Inc. (Parsippany) — A major North American producer with integrated ammonia and sulfuric acid capability; recent company disclosures show robust pricing and mix dynamics in late 2025, underscoring favorable regional supply-demand balances.

Sumitomo Chemical, OCI Global, Domo Chemicals, Nutrien, Jost Chemical, Hubbard-Hall — These firms collectively span integrated fertilizer platforms, specialty markets, and niche industrial channels. Their strategic moves—capacity adjustments, byproduct optimization, and targeted commercialization—determine local availability and service levels.

PW Consulting’s analysis highlights that while a handful of global players command significant installed capability, the market is not monopolized: measured concentration ratios suggest room for competitive disruption via technology, cost positioning, or service differentiation.

Beyond headline forecast figures, PW Consulting’s deliverables are designed for immediate inclusion in corporate planning cycles and procurement playbooks. Key components include:

Integrated forecast engine: A transparent model projecting global market value (USD Million) across 2026–2032 under base, upside and downside scenarios; sensitivity toggles for feedstock price, tariff changes, and demand shocks.

Supplier risk matrix: Tiered counterparty scoring for credit, feedstock exposure, environmental liability, and logistics risk—scored and prioritized for mitigation planning.

Pricing & contract playbook: Market-tested approaches for indexation, minimum volumes, force majeure, and hedging strategies adapted to regionally divergent feedstock regimes.

Regulatory impact assessment: Jurisdictional checklists and capital-impact estimates tied to recent emissions and manufacturing standard updates to quantify likely permit timelines and retrofit costs.

M&A and partnering roadmap: Target profiles derived from concentration analysis and byproduct supply trends, with transaction case studies and valuation primers to accelerate deal execution.

Operational playbooks: Recommendations for optimizing co-located ammonia/sulfuric acid platforms, caprolactam byproduct routing, and conversion yield improvements.

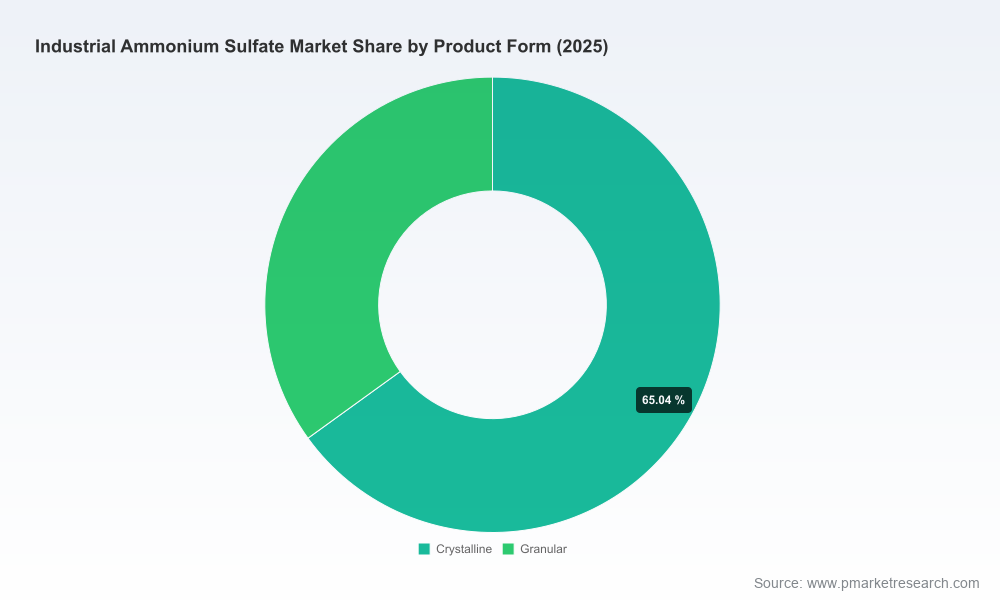

Commercial segmentation framework: Go-to-market options and margin-improvement levers for industrial-grade versus specialty-grade channels (note: the full report contains detailed segmentation data and regional breakdowns available to subscribers).

Lock in flexible supply: Negotiate tiered contracts with optionality tied to feedstock indices and tariff developments rather than fixed long-term spot contracts.

Prioritize counterparty due diligence: Focus on suppliers with captive ammonia/sulfuric acid integration or stable byproduct streams to reduce margin exposure to upstream tariffs.

Accelerate compliance-driven capex planning: Treat updated emissions standards as an operating cost driver—schedule retrofits early to avoid permit-related downtime or price hikes.

Explore adjacency plays: Target bolt-on acquisitions or tolling agreements with producers specializing in byproduct-origin supply to secure low-cost feedstock pathways.

Differentiate on service: For industrial customers, fast-response logistics, technical support and blended product solutions can command premium pricing in otherwise commoditized channels.

Scenario test your balance sheet: Run the PW Consulting forecast scenarios through capital allocation, working capital and covenant stress tests ahead of 2027 budgeting.

Corporate performance signals: Leading manufacturers have reported resilient price/mix dynamics in late 2025, highlighting favorable regional supply-demand balances in certain markets.

Trade policy nuance: Policymakers in some major import markets have exempted ammonium sulfate from recently introduced import tariffs, keeping cross-border supply channels more open than for some upstream inputs.

Trade flows: December 2025 import activity into major consumption regions confirmed sustained global trade flows and the strategic importance of low-cost exporting hubs.

Regulatory shifts: New hazardous air pollutant and manufacturing standards in 2026 create near-term compliance costs but also longer-term incentives for capacity rationalization and higher-barrier-to-entry positions for compliant players.

This preview communicates the most consequential signals PW Consulting has identified for 2026 decision cycles. The full Industrial Ammonium Sulfate Market report contains the proprietary data sets, regional and end-use segmentation, and downloadable forecasting model that enable precise scenario testing, supplier selection, and transaction due diligence. Consistent with the report’s role as an operational playbook, granular segment tables and geo-specific price curves are intentionally reserved for authenticated report subscribers to preserve commercial confidentiality and ensure actionable advantage.

For procurement leaders, strategy teams, and corporate development officers preparing 2026 initiatives, the recommended next steps are:

Request the full report and model to run your organization’s bespoke scenarios.

Engage PW Consulting for a tailored workshop to translate market scenarios into procurement contracts and capex roadmaps.

Undertake targeted supplier audits against the PW risk matrix as part of contract renewals scheduled for 2026.

PW Consulting delivers pragmatic strategy and industry analysis for energy, chemicals and industrial clients. Our Industrial Ammonium Sulfate Market report combines primary interviews, proprietary modeling, and regulatory scanning to create an operational blueprint for executives who must make high-stakes decisions in 2026 and beyond.

Access the full report and interactive forecast model at our official release page. Subscribers gain immediate access to detailed segmentation, regional breakdowns and downloadable scenario engines essential for transaction execution and operational planning.

For detailed analysis of this topic, please visit the official page:Industrial Ammonium Sulfate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com