Global Data Annotation Platform Market Growing at 5.6% CAGR Through 2034

Other |

2026-07-02 13:21:10

As global manufacturers and brand owners tighten requirements around recyclability, supply resilience, and cost-to-serve, the label release paper market is shifting from a largely commodity-driven space into a strategic input for packaging and adhesive innovation. PW Consulting’s forthcoming Label Release Paper Market report (base year 2025) synthesizes historical performance, near-term forecasts and practical go-to-market playbooks designed to inform capital allocation, procurement strategies, and M&A decisions in 2026 and beyond.

Label Release Paper Market

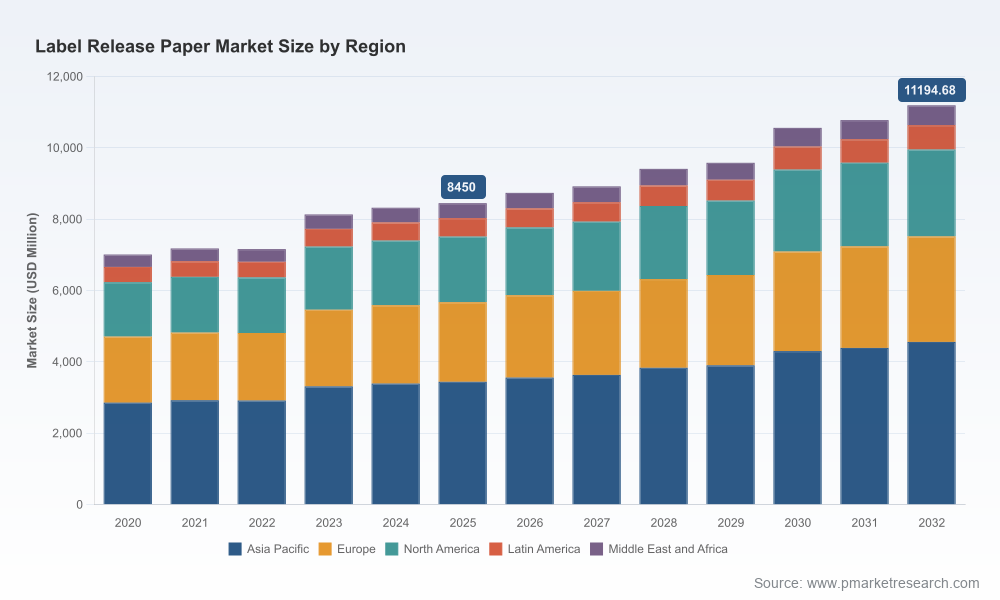

The market expanded unevenly in the 2020–2025 window but returned to a steady growth path in 2023–2025. Our base-year assessment pegs total market size at approximately USD 8.45 billion in 2025, with the market forecast to grow at a compound annual growth rate (CAGR) of roughly 4.1% through our forecast period. That trajectory implies a mid-decade market value north of USD 8.7 billion in 2026 and reaches into the low double-digit billion range by the end of the forecast horizon.

Label Release Paper Market

For procurement heads and capital planners, these macro dynamics matter: steady, single-digit growth combined with pockets of material-driven disruption demands a differentiated approach to supplier relationships, inventory policies and product innovation investments over 2026–2028.

Label Release Paper Market

The label release paper space remains diversified by base paper type and end use. Our full analysis parses demand across product types (glassine, coated kraft variants and poly-coated kraft among others), core application verticals (from logistics & e-commerce to pharmaceuticals and food & beverage), and regional dynamics. While we are deliberately withholding the granular split data in this preview to preserve our report’s actionable value, readers should note two strategic realities surfaced across segments:

Release liners are fundamentally a paper- or film-based product finished with silicone. Common base papers include glassine and various kraft grades; many manufacturers combine PE lamination or barrier films to mitigate silicone soak and meet performance specs. Grammages and substrate constructions vary by application, but the underlying theme for 2026 is materials arbiters: pulp and polymer availability, energy costs, and coating capacity will materially affect unit economics.

Strategic actions for 2026:

Regulatory trends and recyclability benchmarks are now front-and-center. Extended Producer Responsibility (EPR) schemes in multiple U.S. states and evolving European standards are increasing the cost of non-recyclable packaging components and raising lifecycle visibility.

Concurrently, product innovation is responding: recent commercial launches illustrate the industry’s push toward recyclable double-sided silicone-coated liners that meet CEPI-type recyclability assessments. These developments are not merely marketing; they affect sortability, material recovery economics and downstream recycling rates — metrics that will be factored into producer obligations under EPR frameworks in 2026.

The industry structure blends global diversified paper and materials majors, specialist liner manufacturers, and regional producers. Market concentration suggests the largest three players together hold a significant share, and the top five control an even larger portion — a dynamic that creates both opportunity and constraint for competitors and buyers alike.

Key competitor archetypes and strategic implications:

Recent product and technology moves illustrate these dynamics: suppliers have introduced recyclable double-sided silicone-coated liners and lower-grammage glassine products tailored for sustainable label programs. These advances reflect a broader industry pivot: technical differentiation will increasingly be delivered through sustainable performance, not price alone.

Our full Label Release Paper Market report is structured to be used, not just read. Highlights include:

We designed this research with two audiences in mind: commercial leaders who need to make procurement and product decisions in 2026, and corporate strategists evaluating structural moves such as integration or capability acquisition. The combination of up-to-date market sizing, concentration analysis, supplier and product maps, and operational playbooks provides a decision-ready toolkit rather than an academic exercise.

This preview highlights the report’s strategic value while preserving the granular data and segmentation analysis that make the full study actionable for procurement, product and M&A teams. To review the complete findings, including full segmentation tables, regional demand scenarios and supplier scorecards, please visit the PW Consulting report page or contact our industry leads for a tailored briefing.

PW Consulting will also be hosting a client-only roundtable in Q2 2026 to translate the report’s insights into customized roadmaps. Limited seats are available for brand owners, converters and strategic suppliers.

For organizations that must decide in 2026, the choice is straightforward: treat release liner sourcing and product design as a tactical checkbox, or elevate it into a strategic lever that reduces regulatory exposure, improves recyclability performance and secures supplier resilience. Our report is built to help you do the latter.

For detailed analysis of this topic, please visit the official page:Label Release Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com