M2M Satellite Communication Solution Market Size, Share & Forecast 2034

Technology |

2026-05-28 10:25:28

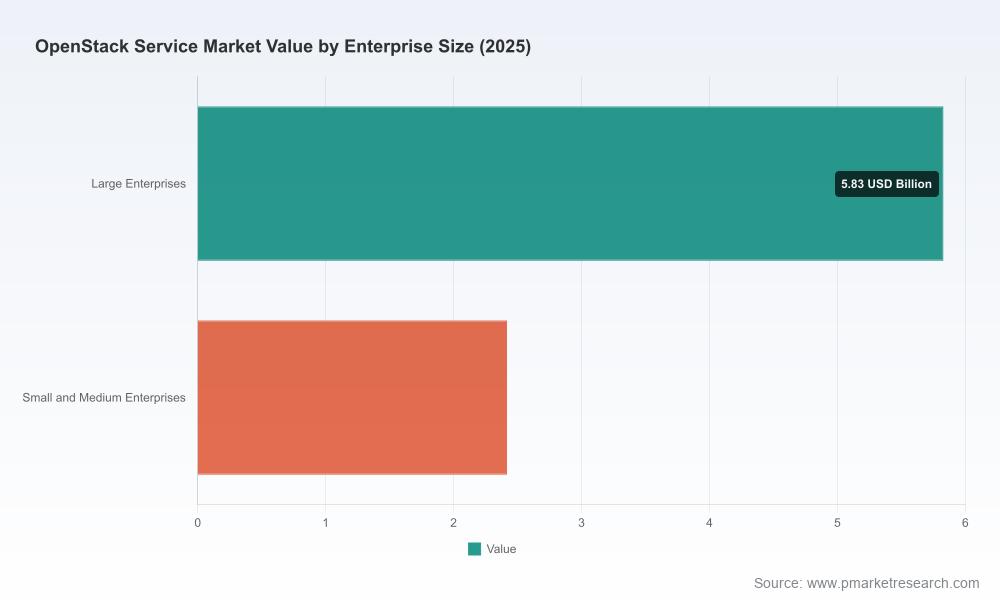

PW Consulting’s latest OpenStack Service Market report—based on a 2025 base year and a 2026–2032 forecast horizon—maps the commercial re-emergence of OpenStack as a pragmatic foundation for private, hybrid and edge cloud architectures. Our analysis shows the market expanding from a mid-single‑digit billion USD base in 2020 to an USD multi‑billion market in 2025, and projecting to nearly USD 17.0 Billion by 2032, driven by a compound annual growth rate (CAGR) of 10.78% across the forecast period. For enterprise leaders planning 2026 investments, the report translates these macro dynamics into decision-ready strategy, procurement, and operational guidance—without burying you in raw segment tables. (For full segment-level detail, vendor share matrices and downloadable data sets, please consult the full report.)

Openstack Service Market

Market momentum and timing: The OpenStack services market is sufficiently mature that 2026 is now a tactical year for converting pilots into production-grade deployments. The combination of continued upstream innovation and expanding managed-service offerings means enterprises can shorten time-to-value while retaining deterministic cost control and portability.

Openstack Service Market

Risk-managed modernization: Organizations facing rising public-cloud bills, energy and grid constraints, or sovereign data requirements need validated roadmaps to shift workloads to private/hybrid platforms. Our report provides the frameworks to quantify risk versus reward across multiple migration patterns.

Openstack Service Market

Vendor strategy: With a market exhibiting moderate concentration, vendor selection matters: choosing between enterprise Linux/open-source integrators, pure-play OpenStack specialists, systems vendors and cloud-native service providers affects operational model, SLAs and long-term TCO.

Renewed adoption at scale: OpenStack is experiencing a second wave of adoption, reinforced by upstream releases that prioritize automation, workload mobility and heterogeneous hardware support. Foundation telemetry and community surveys indicate sustained production footprints measured in tens of millions of compute cores—evidence of real-world scale beyond early adopters.

Services-first market shift: Growth is driven more by services—consulting, managed operations, migration and integration—than by pure software sales. Buyers increasingly prefer outcomes-based engagements, fixed-price migration packages and build-operate-transfer contracts that lower entry barriers.

Edge and research workloads: Scientific and HPC use cases, and latency-sensitive edge services, are catalyzing bespoke OpenStack deployments where performance and control trump public-cloud convenience.

Energy and regulatory tailwinds: Rising data-center electricity demand and evolving grid commitments by hyperscalers are forcing enterprises to include energy cost, resilience and compliance as first-order factors in cloud location and architecture decisions.

Transparent market sizing and methodology: Reproducible top-down and bottom-up approaches, assumptions mapping, and scenario runs for conservative, base and accelerated adoption paths over 2026–2032.

Buyer-focused playbooks: Step-by-step deployment and migration playbooks covering discovery, PoC design, VMware-to-OpenStack migration pathways, cutover sequencing, and rollback/continuity options.

TCO and ROI models: Customizable templates that factor capital, operational, energy and labor costs over five-to-ten-year horizons—allowing procurement and finance teams to stress-test managed services versus insourced operations.

Vendor scorecards and commercial negotiation checklists: Comparative templates capturing product maturity, integration toolchains, managed-services SLAs, credentialing, security and compliance posture, and commercial terms to prioritize in RFPs.

Security and operational readiness: Practical controls, hardening checklists, patch/maintenance playbooks and incident response runbooks mapped to hybrid-cloud realities.

Case studies and deployment archetypes: Real-world snapshots across industries—enterprise IT, telco, research computing and edge—that illustrate architecture tradeoffs and lessons learned.

Large enterprise integrators and platform vendors remain central influencers. Red Hat continues to position its enterprise OpenStack platform and hybrid cloud integrations as a default choice for organizations standardizing on Red Hat/OpenShift ecosystems, with strong enterprise support and migration tooling.

Pure-play OpenStack specialists are translating product expertise into managed operations and outcome-based engagements. Firms that can package production-grade managed services, migration accelerators and build-operate-transfer models are winning multi-year contracts.

Canonical and other Linux-centric vendors offer automated deployment frameworks and fixed-price service packages attractive to buyers seeking predictable onboarding and SLA-driven managed services.

Regional and niche providers—those focused on hosted private clouds, scientific research, or specific geographies—are differentiating on domain expertise and latency/sovereignty guarantees rather than competing on scale alone.

Systems and infrastructure vendors continue to bundle OpenStack compatibility into converged and hyperconverged offerings, simplifying procurement for organizations prioritizing vendor single‑point accountability.

Market concentration: The top three and top five suppliers command meaningful shares but do not form an insurmountable oligopoly. Buyers retain negotiating leverage through clear procurement frameworks and outcome-based contracting.

OpenStack 2026.1 release: The upstream community’s latest release focused on operational improvements, smarter automation and enhanced workload migration capabilities—reducing operational friction for heterogeneous infrastructures and improving interoperability between bare metal, virtualized and containerized workloads.

Measured scale in production: Foundation-level surveys documenting large compute footprints signal that vendors’ claims of enterprise readiness are backed by production deployments and operational experience—critical when evaluating references and failure modes.

Product and services moves: Continued introductions of fixed-price managed packages, expanded managed-service portfolios and strengthened security updates from major platform vendors have shortened the ramp time for many organizations moving to OpenStack.

Energy and grid dynamics: Rising data-center electricity use and recent industry commitments to fund grid upgrades—combined with regional transmission changes in response to AI/cloud load growth—make energy strategy and site selection a core component of cloud economics and resilience planning.

Regulatory nuance: While some jurisdictions lack binding federal data-center efficiency mandates, recent policy instruments and industry pledges are reshaping the incentives and obligations around new builds and large-scale migrations.

CIO / CTO: Treat 2026 as a decision year. Run parallel PoCs for managed-service and insourced operating models, and use our TCO templates to quantify energy, labor and migration risk. Prioritize workloads where control, data residency or latency provide material strategic value.

Infrastructure & Cloud Architects: Adopt a validated reference architecture from the report that includes automation-first operational models, defined upgrade/rollback procedures, and a roadmap for integrating Kubernetes workloads with OpenStack-managed infrastructure.

Procurement & Finance: Negotiate outcome-based SLAs and include built-in escrow, portability clauses and capacity change mechanisms. Use our vendor scorecards to align commercial terms with operational risk tolerances.

Security & Compliance: Bake security updates, patch cycles and third-party audit requirements into vendor contracts. The report’s security playbook provides concrete timelines and acceptance criteria for patch windows and hotfix rollouts.

Our report is designed to be the working document for 2026 planning cycles: it pairs clear market sizing and forecast scenarios with hands‑on playbooks, procurement artifacts, vendor scorecards and customizable TCO models. Whether you are evaluating a phased migration, procuring managed services, or designing an energy‑aware private cloud footprint, PW Consulting offers implementation workshops, vendor due diligence, and operational readiness assessments that translate the report’s strategic insights into executable plans.

To access the full dataset, region- and application-level economics, vendor market shares, and downloadable procurement templates—including the migration checklist and ROI calculator referenced above—download the complete OpenStack Service Market report from PW Consulting’s publications page. For tailored briefings or bespoke advisory support, contact our industry team to schedule a strategy session focused on your 2026 priorities.

For detailed analysis of this topic, please visit the official page:Openstack Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com