Hydrogen-Cooled Synchronous Condenser Market: Strategic Imperatives for 2026 Decision-Makers

As global power systems accelerate toward high shares of variable renewable generation, system-strength solutions move from contingency planning to core procurement. PW Consulting’s latest market study on Hydrogen Cooling Synchronous Condensers — with a base year of 2025 and a forecast horizon through 2032 — translates granular technical insight and commercial intelligence into a practical playbook for executives, project sponsors, transmission operators, and OEMs facing procurement and investment decisions in 2026. The report combines historical trend analysis (2020–2025), forward-looking market modelling, and vendor-level competitive intelligence to enable confident strategic choices while preserving the proprietary segmentation detail that informs contract tactics and pricing negotiations.

Hydrogen Cooling Synchronous Condenser Market

Market outlook: scale, trajectory, and what it means for 2026

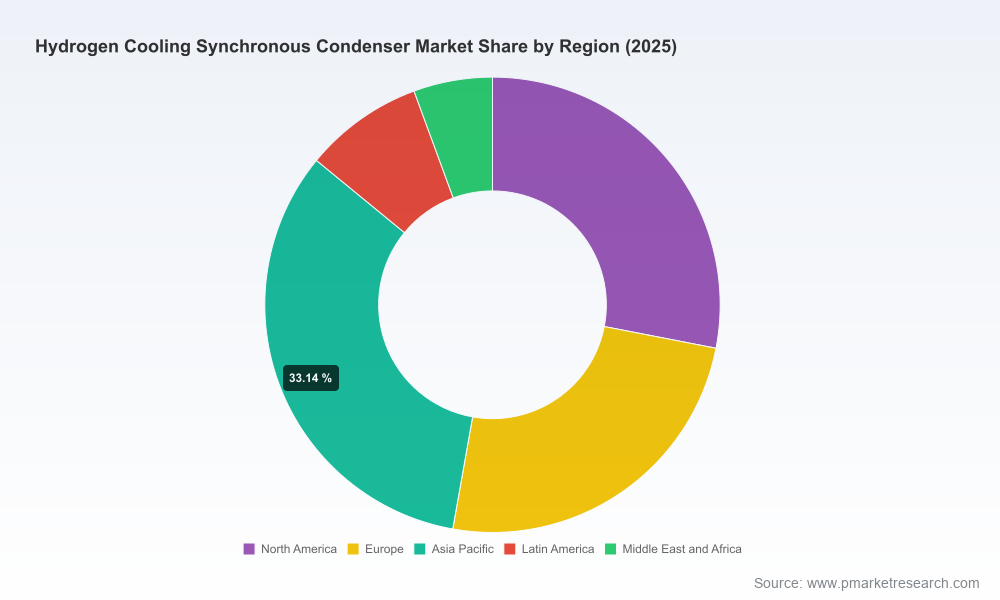

Our modelling shows the hydrogen-cooled synchronous condenser market in clear expansion: having grown from USD 290.15 Million in 2020 to USD 385.4 Million in 2025, the market is forecast to continue expanding at a compound annual growth rate (CAGR) of 5.86% through 2032, reaching roughly USD 574 Million by the end of the forecast window. These headline numbers capture both replacement demand driven by thermal plant retirements and new-build volumes linked to large renewable integration programs and transmission-strengthening projects.

Hydrogen Cooling Synchronous Condenser Market

- Why the growth matters in 2026: procurement cycles initiated now will intersect with peak delivery windows for Renewable Energy Zones, grid reinforcement programs, and generator decommissioning schedules in 2027–2029. Timing decisions made in 2026 therefore materially affect capacity availability, cost inflation exposure, and project sequencing.

- Market structure: concentration metrics indicate that a relatively small group of established OEMs captures the majority of large-scale hydrogen-cooled synchronous condenser business, creating both supply-side predictability and competitive pressure on lead times, standardization, and aftermarket services.

Technology trade-offs that will determine winners and losers

Hydrogen cooling is attractive for utility-scale rotating machinery because of its superior thermal conductivity and low density, enabling higher power ratings and operational efficiency than air-cooled alternatives. In practice, however, the hydrogen option introduces discrete engineering, safety, and lifecycle considerations that materially influence total cost of ownership (TCO) and project risk:

Hydrogen Cooling Synchronous Condenser Market

- Operational reliability vs complexity: hydrogen-cooled machines support higher continuous ratings and improved heat dissipation, but require robust sealing systems, purity control, and leak-detection infrastructure. Buyers must quantify the O&M lift and safety governance required to sustain expected performance over a multi-decade service life.

- Regulatory and procurement framing: grid operators in high-renewable systems increasingly specify synchronous condensers to restore inertia, short-circuit strength, and dynamic reactive support as synchronous thermal plants retire. Conversely, some tenders explicitly avoid hydrogen-cooled solutions to limit hydrogen handling complexity — an important procurement nuance to surface early in tender design.

- Cooling selection matrix: the decision framework should be driven by site-specific criteria — rated MVAR/MVA, ambient conditions, maintenance access, safety environment, and local regulatory stance on hydrogen handling — rather than a default technology preference.

Competitive landscape: established incumbents, new winners, and strategic implications

The market is populated by global OEMs with deep heritage in large rotating machinery and turnkey delivery capability. PW Consulting’s vendor assessment profiles the technical positioning, delivery footprint, and aftermarket strength of the principal suppliers, and maps how their strategic moves are reshaping supply-side dynamics. Key observations for 2026:

- Heritage and capability matter: firms with decades of experience in hydrogen-cooled generators translate that expertise to synchronous condenser designs at scale, offering advantages in design maturity, factory testing, and heavy-equipment logistics.

- Turnkey vs modular play: some suppliers emphasize turnkey EPC delivery with integrated balance-of-plant, while others compete on modular, factory-assembled units designed for faster on-site commissioning. Buyers should align contractual incentives — performance guarantees, mechanical completion milestones, and spare-part packages — with the supplier’s delivery model.

- Aftermarket and digitalization are strategic differentiators: vendors that pair hydrogen-cooled hardware with advanced condition monitoring and remote diagnostic services materially reduce lifecycle risk. For capital planners, the availability of vendor-backed performance analytics should factor into procurement scorecards.

Recent contract awards and EPC arrangements underscore these dynamics and provide tactical signals for 2026 sourcing:

- Major contract awards in 2025–2026 reflect active deployment of synchronous condensers alongside large renewable programs and grid-strength initiatives. Several notable OEMs secured multi-unit projects and national-grid assignments that demonstrate the ongoing prioritization of synchronous solutions.

- Consortium arrangements and EPC wins confirm that buyers and financiers prefer integrated delivery approaches for technically complex installations, particularly where site-specific civil works, gas handling infrastructure, and system integration are bundled.

Practical 2026 playbook — immediate actions for executives

For decision-makers preparing capital programs, procurement lanes, or vendor partnerships in 2026, PW Consulting recommends a compact, actionable set of steps to convert market intelligence into defensible outcomes:

- Adopt a cooling-agnostic requirements baseline: structure tenders to evaluate performance outcomes (inertia provision, short-circuit capacity, dynamic reactive response) rather than prescriptive cooling technologies. This preserves competitive tension while ensuring performance standards.

- Mandate lifecycle cost and risk disclosure: require bidders to submit harmonized TCO models that quantify maintenance regimes for hydrogen handling (seals, purity controls, leak detection), insurance implications, and workforce training needs.

- Embed safety and regulatory gating: ensure procurement timelines allow for permitting and hydrogen-handling safety case approvals; where jurisdictions are reticent on hydrogen, include non-hydrogen fallbacks as pre-approved alternatives in bid documents.

- Prioritize aftermarket and digital service SLAs: specify remote monitoring, predictive maintenance algorithms, and spare-part provisioning levels in contracts to minimize unplanned downtime and long-term costs.

- Secure long-lead components early: in markets with concentrated supplier capacity, locking critical-path items and long-lead mechanical assemblies through early supplier agreements can materially shorten delivery timelines and reduce price volatility exposure.

- Structure financing around performance milestones: use milestone-linked disbursements tied to factory acceptance testing, site mechanical completion, and guaranteed reactive/inertia performance to align incentives and de-risk project cash flows.

What the full PW Consulting report delivers (high level)

The study is built for decision support. It contains:

- Market sizing and trend modelling (historical 2020–2025 and forecast 2026–2032) presented in USD Million with scenario sensitivity to commodity, labour, and policy shocks.

- Vendor profiles and a competitive scorecard mapping technology approach, delivery models, aftermarket capability, and geographical footprint.

- Technical appendices comparing cooling technologies, engineering trade-off matrices, and a hydrogen-safety readiness checklist tailored to grid-connection projects.

- Commercial tools: procurement templates, RFP language options (hydrogen-allowed vs hydrogen-restricted), a standardized TCO comparator, and contract clauses for performance guarantees and spare-part coverage.

- Case studies and lessons learned from recent deployments, illustrating delivery risk, grid integration practices, and commissioning best practices.

Note: the report intentionally preserves sensitivities in market segmentation and individual contract economics to protect the competitive integrity of the underlying primary research. Prospective buyers who require disaggregated regional, application, and type-level data — and the vendor-level win/loss analytics that inform negotiation playbooks — should consult the full report or contact PW Consulting for a tailored briefing.

Strategic takeaway for 2026

2026 represents a window of strategic agency for stakeholders across the value chain. Buyers who design tenders around performance outcomes, anticipate hydrogen-handling realities, and prioritize long-term service relationships will capture competitive advantage and limit downstream operational risk. OEMs that commit to digital-enabled aftermarket offerings, transparent lifecycle economics, and collaborative execution models will consolidate position in a market where a few incumbents already command significant share.

PW Consulting’s Hydrogen Cooling Synchronous Condenser Market report equips leaders with the data-driven insight and executable templates to convert market momentum into reliable system strength — without exposing the granular segmentation intelligence that underpins proprietary procurement strategies. For access to the full dataset, vendor scorecards, and customized advisory, visit PW Consulting’s report page or contact our industry practice for a strategic briefing.

For detailed analysis of this topic, please visit the official page:Hydrogen Cooling Synchronous Condenser Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com