熊谷 インドカレー

Networking |

2026-07-13 09:13:01

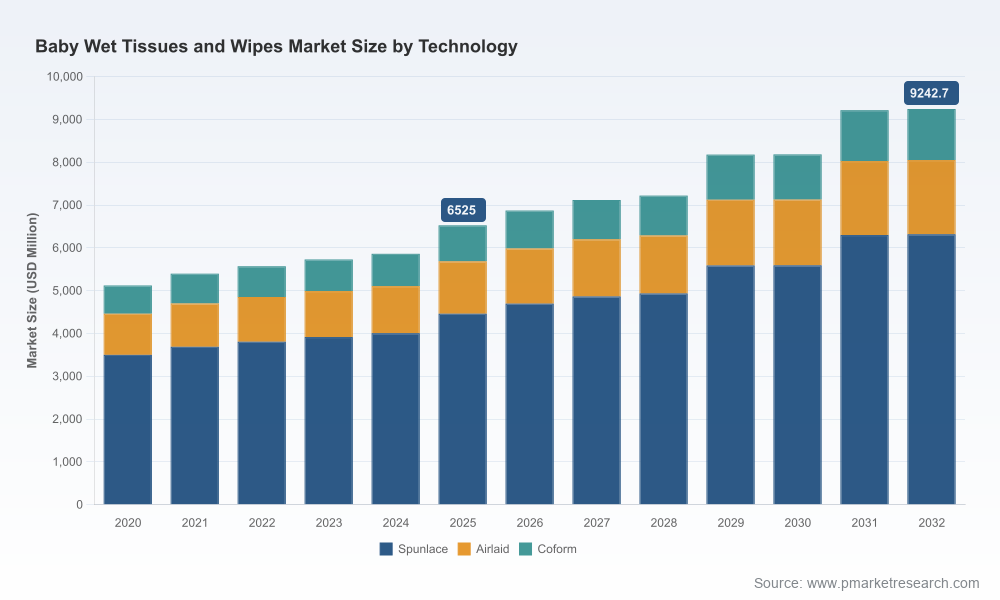

PW Consulting’s latest market study on Baby Wet Tissues and Wipes presents an evidence-backed playbook for executive decision-making in 2026. The global market reached approximately USD 6.5 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.1% through the 2026–2032 forecast window, with long-term trajectories suggesting a market approaching the high single‑digit billions by 2032. This brief highlights the report’s strategic value, summarizes the operationally oriented content, and translates industry dynamics into prioritized actions for manufacturers, retailers, investors and suppliers — while reserving the granular segment-level tables and price decks for the full report.

Baby Wet Tissues And Wipes Market

Healthy baseline growth masks active structural change. A mid-single-digit CAGR accompanies shifts in raw materials, regulation, and consumer preference — creating both margin pressure and premiumization opportunities.

Baby Wet Tissues And Wipes Market

Moderate concentration favors scale and niche specialization: the top three players account for just under 40% of market revenue, while the top five approach just over half the market. This market structure rewards both consolidation plays and focused regional or product differentiation strategies.

Baby Wet Tissues And Wipes Market

Input-cost and trade shocks are altering sourcing economics. Non‑woven polypropylene costs rose materially in 2025, and trade measures affecting imports have changed the calculus for offshore sourcing and regional manufacturing.

Regulation and quality incidents are immediate risk vectors. Recent recalls and preservative limits in key jurisdictions have heightened compliance and testing expectations across formulation and packaging lines.

PW Consulting structured the study to be a working tool for 2026 decision cycles. The following are the practical modules you can apply directly to strategy, procurement, manufacturing and commercial planning:

Top‑down and bottom‑up market-sizing (2020–2032) with scenario variants — base, downside and accelerated-adoption pathways — enabling stress‑tested budgeting and investment planning.

Price and margin model for finished wipes and major non‑woven inputs, including sensitivity to polymer feedstock, pulp and active ingredient costs.

Manufacturing cost benchmark with floor‑space, labor, CAPEX and yield assumptions to compare greenfield vs. conversion and contract manufacturing economics.

Channel and buyer behavior playbook: go‑to‑market levers for mass, pharmacy, convenience and e‑commerce, with prioritized tactics for private label acceleration and omni‑channel bundling.

Regulatory and QA matrix that aligns product formulations against the latest jurisdictional constraints and recall drivers, including required test protocols and supplier audit checklists.

Supplier and raw‑material risk map with near‑term mitigation options (dual‑sourcing, hedging, regional inventory hubs) and medium‑term strategies (localization, backward integration).

Sustainability assessment framework: lifecycle hot‑spotting, packaging reduction levers, and certification pathways for ecolabels and biodegradable claims.

M&A and partnership dossier: playbook for tuck‑ins, contract manufacturer partnerships, and JV structures aligned with distribution reach or technical capability gaps.

90/180/365 day action templates for commercial pilots, supplier negotiations, and regulatory compliance ramps — ready for immediate deployment by category teams.

The market mixes global consumer giants, regional champions and specialized contract manufacturers. Key strategic profiles summarized in the report include:

Procter & Gamble (Cincinnati, OH, USA) — Global brand leader with Pampers; strength in formulation expertise and large-scale distribution. Recent certification wins reinforce premium, lower‑plastic positioning.

Kimberly‑Clark (Irving, TX, USA) — Strong global supply footprint and a clear sustainability push through plant‑based biodegradable variants targeted at eco‑conscious parents.

Reckitt Benckiser (Slough, UK) — Niche leader in minimalist, water‑based wipes; expanding US/EU presence with clinical positioning for sensitive skin.

Johnson & Johnson (New Brunswick, NJ, USA) — Consumer health depth with hypoallergenic offerings and established route‑to‑market across developed and emerging markets.

Unicharm (Tokyo, Japan) — Regional product design expertise for Asian moisture and texture preferences; exporting footprint expanding into ANZ and West markets.

SCA Hygiene / Essity (Stockholm, Sweden) — Focus on certified sustainable materials and hygiene channel relationships in Europe and beyond.

Beiersdorf (Hamburg, Germany) — Skincare-led formulations, leveraging brand trust for premium positioning in retail and pharmacy channels.

Ontex (Aalst, Belgium) and Rockline Industries (Sheboygan, WI, USA) — Significant private‑label and contract manufacturing capability, critical partners for retailers and international brands seeking capacity or lower-cost production.

Nice Group (Foshan, China) — OEM/export specialist with scale in Asia and strong cost competitiveness for global private label demand.

2025‑10 — Reckitt launched an enhanced WaterWipes variant targeting eczema‑prone skin in US and EU markets.

2025‑09 — Kimberly‑Clark unveiled biodegradable Huggies Special Delivery at a major trade event, signaling faster commercialization of plant‑based formulations.

2025‑06 — P&G’s Pampers Pure received an EU ecolabel certification for reduced plastic content, supporting retail sustainability assortments.

2025‑04 — Unicharm expanded distribution of its flagship baby wipes into Australia through new retail partnerships.

2025‑02 — Essity introduced a near‑water formula in key Northern European markets, aligning with the minimalist trend.

Preservative limits: EU regulation restricts certain preservatives to low concentrations to prevent irritation — requiring reformulation workstreams and enhanced batch testing.

Quality incidents: A 2024 recall of over a million units in the US underscores the reputational and financial risk of microbial contamination; high‑frequency QA controls are now non‑negotiable.

Input cost inflation: Non‑woven polypropylene costs increased materially in 2025, pressuring margins for legacy formulations and emphasizing the value of efficient material use or alternative substrates.

Trade barriers: New tariffs on select non‑woven imports have raised landed costs for Asian‑sourced materials, accelerating conversations on regional capacity and near‑shoring.

Consumer shift: Demand for biodegradable and low‑impact wipes accelerated in 2025 — an adoption trend that premium and mainstream brands must map into innovation pipelines.

Procurement and manufacturing: Rebalance sourcing risk via multi‑sourcing and regional buffer stocks. For companies dependent on Asian non‑wovens, model the tariff and freight delta versus local conversion investments.

Product portfolio and R&D: Prioritize reformulations that meet tightening preservative and safety thresholds while enabling biodegradable claims. Fast‑follow pilots for 99% water formulations and low‑residue chemistries reduce regulatory friction.

Commercial strategy: Accelerate e‑commerce readiness and subscription models for repeat purchase frequency; deploy premium eco‑lines in pharmacy and specialty channels where verification and premium pricing are feasible.

M&A and capacity: Use market concentration dynamics to identify bolt‑on acquisitions that add technical know‑how (e.g., water‑based formulation) or fill regional manufacturing gaps — pick targets aligned to short payback horizons.

Quality and compliance: Implement end‑to‑end QA traceability and third‑party microbial controls as a differentiator and insurance against recall-related losses.

Sustainability comms: Align packaging and formulation claims with verifiable standards; ecolabels materially improve shelf visibility and retailer uptake in mature markets.

0–90 days: Run a procurement stress test to quantify exposure to polymer price and tariff scenarios; launch an internal cross‑functional regulatory compliance audit.

90–180 days: Pilot two product variants (one biodegradable, one near‑water) in select channels; commence supplier qualification for a regional non‑woven partner.

180–365 days: Finalize make vs. buy decision for regional capacity; execute one strategic partnership or tuck‑in acquisition to accelerate product or geographic reach.

For CPG leaders, investors and supply‑chain chiefs, the PW Consulting report translates macro growth and disruptive inputs into executable actions. It combines rigorous demand forecasting with manufacturability economics, regulatory compliance matrices and ready‑to‑use commercial playbooks — all designed to shorten the path from insight to measurable impact. The study’s scenario models allow you to stress‑test pricing, capital allocation and go‑to‑market decisions under plausible 2026 market shocks.

Note: This press brief intentionally highlights strategic findings and practical applications while withholding the granular segment tables, detailed price decks, and full region/application splits that underpin our models. Those core datasets and downloadable Excel tools are available in the full report and interactive dashboard on PW Consulting’s report page.

For inquiries, corporate briefings, or to request a corporate license to the full Baby Wet Tissues and Wipes Market report (including proprietary forecasts, channel KPIs, and supplier scorecards), please contact PW Consulting’s industry desk or visit our website for purchasing and enterprise subscription options.

For detailed analysis of this topic, please visit the official page:Baby Wet Tissues And Wipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com