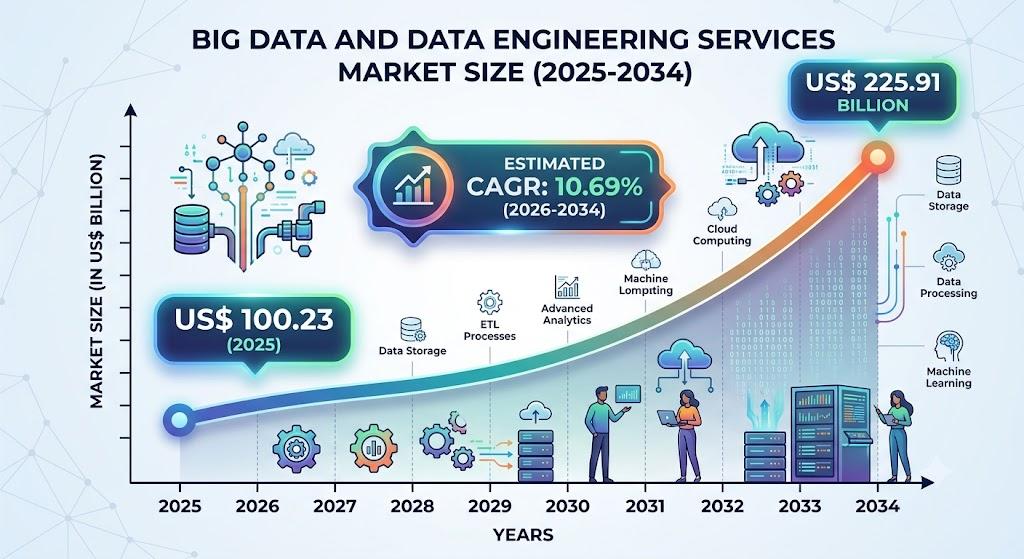

Big Data and Data Engineering Services Market Overview Share, Growth & Forecast 2034

Technology |

2026-07-09 13:00:02

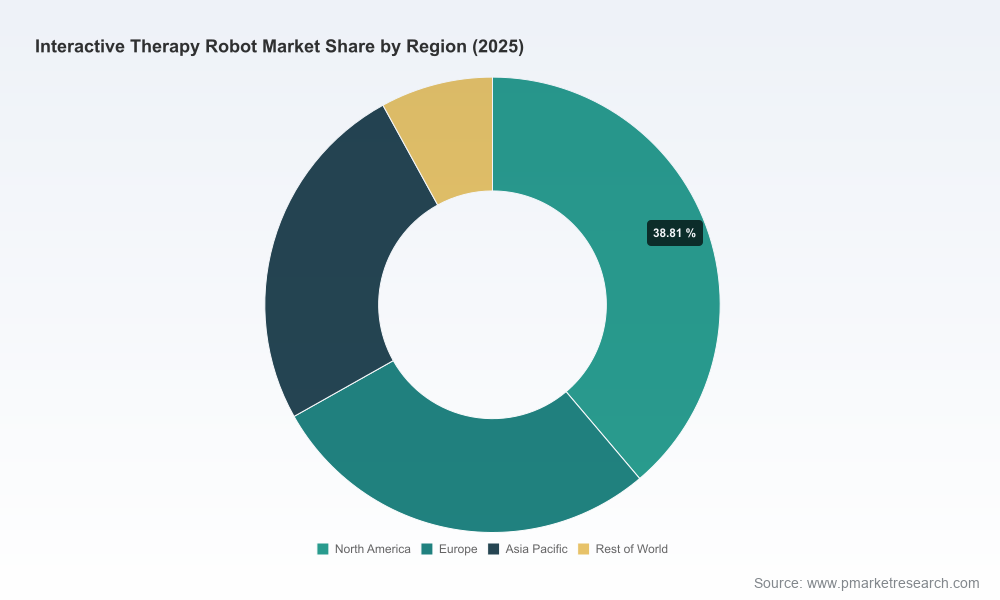

As lead industry analyst at PW Consulting, I present a concise strategic briefing drawn from our new Interactive Therapy Robot Market report (base year 2025, forecast 2026–2032). The market has moved from a sub‑billion niche in 2020 to roughly USD 1.6 billion in 2025, and is projected to accelerate under an 18.5% CAGR — surpassing USD 1.8 billion in 2026 and climbing toward a multi‑billion dollar opportunity by 2032. For executives making 2026 resource-allocation and go‑to‑market decisions, this is a pivotal inflection point: the technology is maturing, regulatory and reimbursement signals are converging, and early deployments are delivering measurable clinical and operational value. This briefing outlines the strategic implications and the practical capabilities our full report delivers, while reserving the detailed segment-level figures for the full study.

Interactive Therapy Robot Market

Regulatory clarity is materially improving. Examples such as the FDA’s classification of therapeutic animal‑like devices demonstrate a viable medical‑device pathway for emotionally assistive and biofeedback robots; concurrently, EU MDR and country‑level guidance are increasingly defining when such systems fall under medical device rules versus lower‑risk classifications. That distinction drives clinical evidence requirements and time to market.

Interactive Therapy Robot Market

Reimbursement momentum is real. The 2026 CMS update added Remote Therapeutic Monitoring (RTM) service codes (e.g., 98979, 98984, 98985) that can cover device‑enabled therapeutic interactions and device data transmission — a structural change that enables sustainable service revenue models for device makers, providers, and digital therapeutics partners.

Interactive Therapy Robot Market

Proof points from care settings are scaling. Recent hospital and nursing‑home deployments demonstrate measurable reductions in staff burden and gains in patient engagement across pediatrics, geriatrics, and cognitive care. These early adopters are providing the real‑world evidence needed to convert pilots into procurement programs in 2026–2027.

Robust market sizing and forward‑looking modeling: end‑to‑end revenue model calibrated to 2025 base data and forecasted through 2032 with scenario sensitivity to reimbursement, unit economics, and pricing dynamics.

Deployment playbooks and procurement checklists: templates for clinical pilots, KPI frameworks (clinical outcomes, utilization, staff time savings), contract terms, and expected TCO timeline for 6‑ to 36‑month horizons.

Regulatory & reimbursement roadmaps: step‑by‑step guidance for U.S. FDA and EU MDR pathways, suggested evidence generation strategies, and payer engagement playbooks tailored to the RTM and related code sets.

Vendor benchmarking and technology maturity matrix: comparative assessment covering clinical validation, software/AI stack, hardware reliability, integration readiness (EHR/APIs), and service delivery capabilities.

ROI and business‑case models: pre‑built calculators and sensitivity analyses that quantify outcomes‑driven revenue (reimbursement capture, value‑based contracts) and cost offsets (reduced readmissions, labor efficiencies).

Go‑to‑market playbook for three archetypes — incumbent medical device firms, digital health entrants, and specialized robotics teams — with channel strategies, partnership matrices (providers, payers, distributors), and M&A/partnership scenarios.

Market structure: concentration is moderate. Top three vendors account for roughly four‑tenths of current market revenue, and the top five collectively approach roughly six‑tenths. That concentration signals meaningful incumbent strength but leaves substantial runway for differentiated newcomers and vertical specialists.

Profiles and strategic positioning:

Strategic implications: competition is bifurcating along two vectors — (1) clinically validated, regulated therapeutic devices that integrate into provider reimbursement pathways; and (2) consumer/home‑focused companions that monetize via subscription and partner ecosystems. Winning companies will combine domain‑specific clinical evidence with platform economics (software, content, data). Interoperability and outcomes data will be the deciding asset for long‑term share gains.

Reimbursement adoption timelines: payer pilot adoption and local Medicare Advantage programs will dictate whether RTM codes translate into scalable revenue in 2026 or remain pilot‑level income until 2027–2028.

Evidence bar and labeling: companies that treat devices as general wellness products will face slower provider adoption; conversely, those who pursue clinical claims must be ready for the time and cost of regulatory compliance and trials.

Data governance and privacy: device manufacturers must demonstrate robust data security and de‑identification practices as devices capture sensitive behavioral and health data, particularly when integrating with EHRs.

Operational integration risk: successful deployments require alignment across clinical workflows, IT integration, staff training, and measurable KPI governance — pilots that ignore these dimensions underdeliver.

Prioritize reimbursement‑aware pilots: design pilots that map directly to available RTM/procedure codes and collect the minimum evidence needed to secure payer interest or interim reimbursement.

Invest in clinical validation early: even modest, well‑designed trials demonstrating clear outcomes (e.g., reduction in therapy hours, improved engagement metrics) will materially shorten procurement cycles with hospitals and payers.

Build or partner for data platforms: outcome measurement, remote monitoring, and secure EHR integration are not optional — they unlock recurring revenue and make long‑term contracts possible.

Choose go‑to‑market focus deliberately: service‑oriented sales into providers requires clinical teams and reimbursement expertise; D2C or payer‑partner models demand different sales and marketing investments.

Consider roll‑up opportunities in niche therapeutic content and distribution: with moderate market concentration, targeted M&A can accelerate content library ownership and channel reach.

Prepare procurement checklists and pilot KPIs now: speed matters in 2026 — providers will choose vendors who can deploy, integrate, and demonstrate value within predictable timelines.

How will our 2026 pilots be structured to capture RTM or equivalent reimbursement as it becomes available?

What evidence package do we need to pursue a regulated medical‑device pathway versus a wellness/complementary therapy positioning?

Do we have the data infrastructure and privacy controls to integrate device outputs into provider workflows and payer dashboards?

Which partnership archetypes (health systems, payers, distributors, content creators) will accelerate adoption in our chosen verticals?

What is our M&A or partnership threshold to secure content, clinical credibility, or distribution advantage within the next 12 months?

PW Consulting’s Interactive Therapy Robot Market report is designed as an executive toolkit for 2026 decision‑making: it combines market forecasts, vendor benchmarking, regulatory and reimbursement playbooks, pilot templates, and ROI models to convert strategic intent into executable plans. This briefing intentionally highlights the high‑level market trajectory and strategic implications while reserving the detailed segment-level breakouts, regional and end‑user splits, and full vendor scorecards for the complete report. Visit our report page to access the full dataset, granular segmentation, and the downloadable playbooks that will allow your organization to move from pilot to scale in 2026.

For detailed analysis of this topic, please visit the official page:Interactive Therapy Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com