Laser Distance Measuring Devices Market — Strategic Briefing for 2026 Decisions

Executive summary

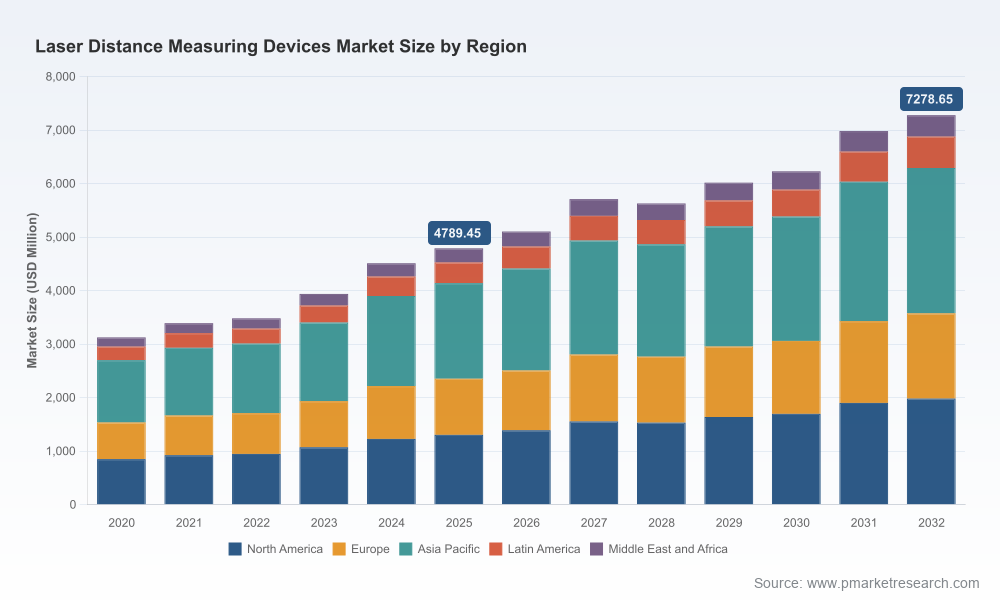

PW Consulting’s latest market research on Laser Distance Measuring Devices delivers an actionable intelligence package designed to inform high-stakes commercial and investment decisions in 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study quantifies a global market that reached approximately USD 4,789.45 Million in the base year (2025) and is modeled to expand at a compound annual growth rate (CAGR) of 6.15% over the forecast period. This briefing summarizes the strategic implications we draw from the analysis while deliberately omitting granular segment and regional tables — those proprietary insights are retained in the full report to encourage direct engagement.

Laser Distance Measuring Devices Market

Why this report matters for 2026 planning

Procurement, product, and M&A teams face converging pressures going into 2026: accelerating digitalization of field workflows, tightening laser safety regulations, and intensifying consolidation among established vendors. Our report synthesizes primary interviews, device-level performance benchmarking, channel and supply-chain mapping, and scenario-based forecasts to support three core decisions executives will need to make next year:

Laser Distance Measuring Devices Market

- Where to prioritize R&D and feature investment to defend or extend device ASP and margins;

- Which go-to-market models (direct vs. channel-led vs. platform partnerships) will yield the fastest customer uptake for smart-distance solutions; and

- Which acquisition targets and alliance partners offer the most accretive paths to scale or to fill capability gaps (e.g., Bluetooth/IoT integration, green-laser range extension, ruggedized industrial ratings).

What the full report contains — practical, transaction-ready deliverables

PW Consulting’s deliverables are crafted for immediate operational use by product leaders, corporate development teams, and commercial executives. Highlights include:

Laser Distance Measuring Devices Market

- Device-level benchmarking: comparative performance matrices covering accuracy, range envelope, battery life, wireless integration, and durability for leading models. This section supports product roadmaps and warranty/risk modeling.

- Pricing and channel playbook: observed ASP bands by value tier, dealer margin structures, and recommended promotional levers for professional vs. DIY segments to optimize sell-through without eroding long-term price integrity.

- Go-to-market decision trees: scenario analyses for direct online channels, specialist distributors, and OEM bundling with power tools or surveying platforms, including estimated time-to-scale and capex/Opex considerations.

- M&A and partnership pipeline: discreet candidate profiling using capability gap mapping, integration risk scoring, and indicative valuation multiples drawn from recent comparable transactions.

- Supply chain and component risk analysis: critical component sourcing maps (laser diode suppliers, CMOS sensors, microcontrollers), single-source risks, and alternative sourcing strategies to mitigate near-term shortages.

- Regulatory and compliance playbook: adoption timetable, cost-to-compliance estimates, and labelling/packaging recommendations in response to recent standard changes.

To retain its role as a decision-support instrument, the full report includes the underlying segment-level revenue tables, country-level volumes, and downloadable model files for client-tailored sensitivity testing.

Competitive landscape — who matters and why

The market exhibits moderate concentration: the top three firms account for a significant share of the market, and the top five increase that concentration materially. This structure has three practical consequences: competitive pricing discipline at the high end, aggressive feature parity in mid-tiers, and healthy opportunity for nimble entrants on specialized use cases.

- Robert Bosch GmbH (Gerlingen, Germany) — Known for the GLM series, Bosch combines hardware reliability with app ecosystems and Bluetooth integration. Recent product introductions — notably a green-laser long-range model launched in mid-2025 — signal continued investment in optical performance to capture professional workflows. Expect Bosch to leverage its distribution networks and brand trust to defend professional segments while selectively expanding into connected services.

- Hexagon AB (Leica Geosystems) (Stockholm, Sweden) — Leica's DISTO line remains the benchmark for construction and surveying-grade accuracy. Their value proposition is premium instrumentation with integrated surveying workflows. Hexagon’s strength in geospatial platforms positions them to commercialize higher-margin software subscriptions associated with device data.

- Fluke Corporation (Everett, Washington, USA) — Fluke’s ruggedized meters are optimized for industrial environments. Their emphasis on durability, calibration services, and enterprise procurement channels makes them a go-to for industrial buyers prioritizing uptime and service agreements.

- Stanley Black & Decker (New Britain, Connecticut, USA) — With the TLM series, Stanley Black & Decker targets both professionals and DIY buyers through broad retail channels. Their advantage lies in cross-selling to tool purchasers and leveraging retail footprint for mass-market adoption.

- Makita Corporation (Anjo, Japan) — Makita positions compact meters within its power-tool ecosystem, enabling bundled offers and field convenience for tradespeople who prefer one-brand toolsets.

- Hilti Corporation (Schaan, Liechtenstein) — Hilti’s PD series focuses on construction sites where service contracts and tool fleet management are prioritized. Their direct-sales model and strong service orientation sustain higher retention and accessory revenues.

Competitor moves to watch in 2026 include continued feature convergence (wireless connectivity, integrated apps), aftermarket service bundling, and selective verticalization (e.g., meters optimized for façade inspection, interior fit-out, or precision manufacturing). The market’s CR3 and CR5 concentration metrics underline that mid-sized acquisitions and differentiated software plays could meaningfully shift competitive dynamics.

Regulatory and standards dynamics

Regulatory shifts are shaping product requirements and packaging costs. Notably, the IEC 60825-1 laser safety standard was updated in early 2025 to require enhanced labelling for Class 2 devices sold in Europe. This change has direct implications for labeling workflows, packaging redesign, and retailer compliance checks. The report quantifies the incremental cost impact across device tiers, estimates the compliance time window for incumbent manufacturers, and presents mitigation strategies (e.g., phased labelling updates, consumer education campaigns, and redistribution of compliance costs across SKU lifecycles).

Strategic recommendations for 2026

- Product leaders: prioritize integration of wireless telemetry and app-based data capture into new models while protecting margin via feature-tiering. Consider a “connectivity-as-a-service” subscription for high-frequency professional users.

- Commercial teams: rebalance channel investment toward specialist distributors and trade-focused e-commerce, with differentiated incentives for pro vs. consumer channels. Pilot bundled offers with tool OEMs where ecosystem affinity can be demonstrated.

- M&A and corporate development: focus on targets that deliver either immediate distribution access in underpenetrated professional channels or proprietary sensing/algorithms that accelerate time-to-market for “smart” distance modules.

- Compliance and operations: accelerate labelling and documentation updates to align with the IEC revisions; lock in alternate laser-diode suppliers to mitigate component concentration risk.

How to use PW Consulting’s report in 90 days

We recommend a rapid, three-step program for 2026 execution:

- Week 1–4: Deliverables distribution — circulate tailored benchmarking extracts to product, marketing, and legal teams; convene cross-functional “war room” to calibrate immediate priorities.

- Month 2: Scenario workshops — use the report’s financial model to stress-test pricing and channel scenarios; prioritize one proof-of-concept for connected-device monetization.

- Month 3: Transaction readiness — begin discreet outreach to top M&A targets identified in the pipeline and prepare compliance roadmap for updated laser labelling.

Final note — what is intentionally withheld here

This briefing is designed as a strategic trailer: it highlights the report’s analytical architecture and the decisions it supports without disclosing the granular regional, application, and SKU-level revenue tables that provide competitive and tactical advantage. For detailed segmentation schedules, country-level volumes, channel-level margin matrices, and the full device benchmarking spreadsheets, please consult the complete PW Consulting Laser Distance Measuring Devices Market report (base year 2025; forecast 2026–2032, figures in USD Million).

To request access to the full report, data models, or an executive briefing tailored to your organization’s strategic priorities, contact PW Consulting’s Industry Team.

For detailed analysis of this topic, please visit the official page:Laser Distance Measuring Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com