Which Certifications Define a Professional Trichologist in Dubai?

Health |

2026-05-06 07:29:11

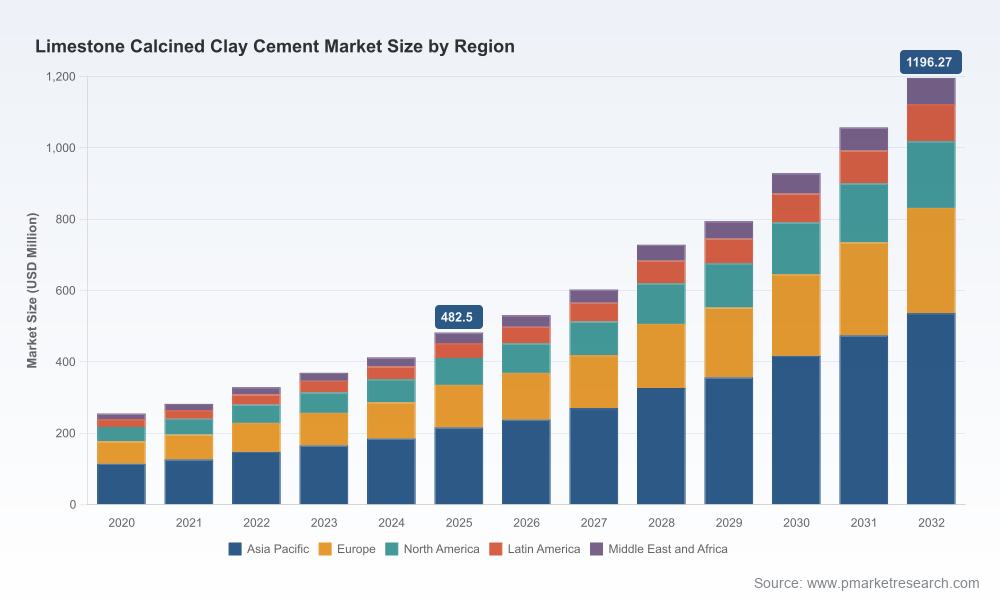

PW Consulting’s latest market research on Limestone Calcined Clay Cement (LC3) frames 2026 as a decisive inflection point for cement producers, infrastructure owners, investors and policy teams. Our base‑year analysis (2025) shows the LC3 market at USD 482.5 Million (reporting unit: USD Million). Under a set of techno‑commercial and policy assumptions, the market is modeled to expand at a compound annual growth rate (CAGR) of 13.85% through our forecast window, reaching USD 1,196.27 Million by 2032. This trajectory encapsulates both a rapid commercialization phase and an accelerating shift toward lower‑carbon binders across multiple construction value chains.

Limestone Calcined Clay Cement Market

Standards and regulatory alignment: LC3 has moved from research curiosity to recognized commercial product in multiple jurisdictions. Key standards bodies and national standards authorities have issued formal recognition or pathway guidance that materially lowers market entry barriers and accelerates adoption in public procurement.

Limestone Calcined Clay Cement Market

Industrialization of calcined clay: Recent commissioning and plant completions demonstrate that LC3 is now being deployed at true industrial scale rather than in isolated pilots. Technology variants such as flash calcination are maturing, and first movers are validating retrofit and greenfield strategies.

Limestone Calcined Clay Cement Market

Cost and carbon economics: LC3’s feedstock and thermal profile—calcination in the 750–850°C range versus 1,450°C for clinker—yields substantial energy and operating‑cost advantages in many jurisdictions. Independent modelling and project disclosures indicate material energy savings (up to ~33% on the thermal side) and operating expense improvements (reported up to ~25% vs ordinary Portland cement in comparable configurations), with selected projects reporting very large carbon intensity reductions when production is optimized.

Public finance and de‑risking instruments: Targeted public funding and industrial demonstration grants in major markets are derisking early investments and tilting the economics in favor of capital deployment for calcined clay lines and retrofits.

Market sizing & scenarios: End‑to‑end market models spanning 2020–2032 with base, upside and downside adoption pathways keyed to policy, energy price and construction demand variables.

Commercial viability playbooks: Detailed techno‑economic models for greenfield and retrofit calcined clay capacity, including capex/opex breakouts, sensitivity analyses and commercial pricing ladders.

Supply‑chain and feedstock playbooks: Sourcing strategies for kaolin/argillaceous clays, logistics modelling, beneficiation recommendations and vendor scorecards.

Regulatory & standards mapping: Practical guidance for achieving compliance with blended cement standards, certification test protocols, and procurement clauses that de‑risk large projects.

Go‑to‑market and commercial roll‑out templates: Offtake structuring, specification drafting, pilot‑to‑scale timelines, and contractor/owner engagement tactics to accelerate specification acceptance.

Competitive and M&A playbook: Screening framework to identify acquisition targets, JV partners and technology licensers—plus valuations calibrated to LC3 economics and carbon pricing scenarios.

Operational readiness & process design: Kiln integration options, flash‑calciner technical assessment, quality control protocols and OPEX optimisation checklists derived from plant case studies.

Risk, compliance and ESG matrices: Carbon accounting templates, supply‑chain ESG due diligence checklists, and policy engagement roadmaps for 2026 corporates.

The LC3 competitive map is evolving from early‑adopter leadership to a mixed landscape of industrial incumbents, regional champions and technology specialists. Market concentration is moderate: the top three firms account for roughly one‑third of the market while the top five approach just under half—creating room for both scale players and agile regional entrants.

Global multinationals (scale + brand): Leaders with global footprints are using LC3 to complement broader low‑carbon portfolios and to meet corporate decarbonization targets. Their advantages include multi‑plant deployment capability, established route‑to‑market and ability to mobilize R&D and capital across regions.

Regional powerhouses (first‑mover advantages): Several large regional producers have moved early on commercial LC3 launches and targeted infrastructure projects—gaining specification wins, local regulatory familiarity and procurement relationships that can be decisive in national construction markets.

Technology and project specialists: JVs and firms deploying flash‑calciner technology and large‑scale calcination capacities are emerging as enablers of high substitution rates and lower carbon intensity. These actors are attractive partners for companies seeking to accelerate scale while defraying R&D and execution risk.

New market entrants and pilots: A cohort of smaller cement producers and regional groups are conducting pilots, converting kilns, or pursuing demonstration funding—creating a patchwork of proof points across geographies that will inform procurement standards in 2026–2028.

Large industrial launches and plant commissioning confirm the technology pathway and provide real‑world benchmarks for capex, operational performance and product acceptance in major construction projects.

Standards recognitions and national standards entries materially reduce technical risk and accelerate inclusion in public procurement and infrastructure specifications.

Targeted public funding for demonstration projects lowers the effective capital hurdle for early movers and creates a window to capture long‑term contractual advantages in regulated markets.

Feedstock unit cost benchmarks and thermal‑efficiency data provide a credible basis for financial modelling and investment committees to evaluate payback under conservative price assumptions.

90 days — Decide and de‑risk: Run a rapid assessment using our standardized techno‑economic template to determine whether to pilot, retrofit or partner. Secure data access to local clay reserves, energy costs and potential public incentives.

6 months — Pilot and validate: Execute an in‑market pilot (or join a regional consortium) with quality control regimes aligned to accepted standards. Use pilot data to refine cost curves and CO2 accounting.

12 months — Scale and finance: Finalize technology pathway (retrofit vs greenfield), secure conditional financing or grant support, and lock offtake or preferential procurement agreements with anchor customers.

18 months — Commercial roll‑out and partnership consolidation: Bring first commercial line(s) online, integrate LC3 into product portfolio, and mobilize sales & specification campaigns targeting infrastructure owners and large developers.

Levelized production cost per ton and sensitivity to energy and clay price movements.

CO2 intensity per ton (scope 1 & 2) and marginal abatement cost relative to alternative decarbonization pathways.

Specification acceptance rate within target procurement channels (public tenders, major developers).

Payback period and IRR under conservative demand scenarios; break‑even on retrofit vs greenfield CAPEX choices.

Supply‑chain resilience metrics: secured clay reserves, alternative sourcing options and logistics lead times.

For boardrooms and strategy teams, LC3 is not merely a sustainability play — it is a strategic option that can reshape cost curves, product portfolios and market access in a decarbonizing construction sector. Our report combines rigorous market modelling (2020–2032), operational benchmarking, regulatory pathway analysis and competitor intelligence to convert market signals into executable steps for 2026. The work is structured to equip investment committees, plant managers and commercial teams with the templates, risk models and vendor screening tools required to move from pilot to profitable scale.

To maintain decision‑advantage, PW Consulting intentionally structures the publicly available summary as a high‑signal overview. The full report contains the granular financial models, detailed regional adoption scenarios, plant‑level case studies and the segmented go‑to‑market playbooks that corporate and investor clients need to actuate strategy in 2026. Access to those proprietary appendices is available through our report portal.

For rapid advisory support: PW Consulting offers an expedited LC3 readiness workshop (2–4 weeks) that uses your plant and market inputs to produce a tailored investment case.

For procurement or M&A teams: we provide target screening and valuation overlays calibrated to LC3 economics and carbon scenario planning.

Full report access: detailed segment analytics, plant‑level models, and vendor scorecards are contained in the full report available through our website.

In a market expanding from a mid‑hundreds million base in 2025 toward a multi‑hundred percent growth path by 2032, decisions made in 2026—on pilots, partnerships, standards engagement and plant investments—will determine who leads the LC3 transition and who follows. PW Consulting is prepared to help you translate those decisions into measurable value.

For detailed analysis of this topic, please visit the official page:Limestone Calcined Clay Cement Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com