PW Consulting: Polymer Capacitor Market Poised for 8.2% CAGR Through 2032

Technology |

2026-07-08 08:10:31

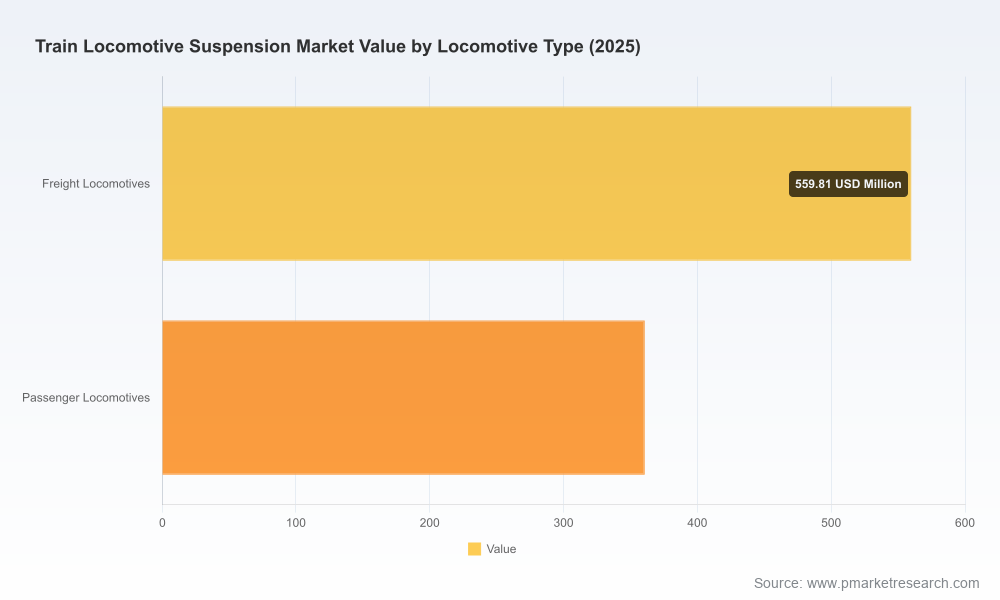

PW Consulting's latest market research report on the Train Locomotive Suspension Market (base year 2025; historical 2020–2025; forecast 2026–2032) equips executives with the evidence and decision levers they need to shape strategy in 2026. Our analysis shows the global market continuing its steady expansion with a compound annual growth rate (CAGR) of 4.62% across the 2026–2032 forecast window. From an estimated industry value in 2025 to a robust projection by 2032, the market trajectory signals durable demand driven by fleet modernization, emissions-driven fuel shifts, and an accelerating aftermarket opportunity tied to lifecycle servicing and refurbishment.

Train Locomotive Suspension Market

Timing: 2026 is a pivotal year for capital allocation decisions across rail OEMs, tier-1 suppliers, and rolling-stock operators. Our report translates macro momentum into actionable near-term choices—what to invest in now versus what to monitor.

Train Locomotive Suspension Market

Risk-adjusted foresight: We combine demand modeling with supply‑chain sensitivity analysis (steel, elastomers, hydraulic fluids) so planners can stress-test procurement and pricing scenarios under raw-material volatility.

Train Locomotive Suspension Market

Competitive clarity: The study maps competitive positioning and capability stacks of the leading suppliers—helping buyers and investors prioritize partner, supplier and M&A targets.

Regulatory alignment: With tighter inspection and safety standards (including updated FRA LSS guidance and contemporary ISO/EN certification expectations), the report indicates where product validation and compliance investment are non-negotiable for market access.

PW Consulting’s topline estimates show a market that has grown steadily through the 2020–2025 historical window and continues to expand through the forecast period. The 4.62% CAGR we model reflects a combination of ongoing new-build activity, large-scale fleet modernization programs, and a growing aftermarket driven by predictive maintenance and component refurbishment. For decision-makers, this balanced growth implies:

Room for premiumization: Suppliers that can demonstrate durability, lower life-cycle cost, and serviceability will capture outsized margins as operators trade up to lower‑total‑cost‑of‑ownership solutions.

Aftermarket leverage: Increasing installed base combined with longer asset lives and refurbishment cycles creates recurring revenue potential for service providers, remanufacturers, and digital monitoring vendors.

Selective regional investment: Demand pockets and procurement programs will justify targeted local presence and partner networks rather than blanket global expansion—precision beats scale for many suppliers in 2026.

The train suspension ecosystem remains a mix of global engineering leaders, specialist component manufacturers, and regional spring houses. Market concentration metrics show a moderate consolidation trend among leading players, leaving meaningful room for specialized entrants and M&A-driven scale plays. Key capability clusters to watch are primary/secondary suspension systems, proprietary damper technology, rebuild/refurbishment competencies, and systems integration for bogies and car-body interfaces.

Continental AG (ContiTech) — strength in integrated primary and secondary springing solutions and OEM-grade refurbishment. Their combination of product breadth and refurbishment services positions them as a systems supplier for operators seeking life‑cycle partnerships.

Enidine (ITT Enidine) — niche expertise in friction snubbers, sealed and rebuildable dampers, and rotary hydraulic solutions. Their focus on harsh-environment durability and rebuildability aligns with heavy-haul and freight modernization needs.

Amsted Rail — scale in coil springs, bogie assembly systems and heavy-haul applications. Their systems approach and deep rail OEM relationships make them a primary-tier partner for freight platforms.

KONI (ITT KONI) — market-leading damper line-up with long-duration products and bespoke engineering services for vertical and horizontal bogie suspension. Durability claims and tailored solutions support premium positioning.

Hutchinson (TotalEnergies group) — legacy strength in air spring assemblies and a broad portfolio across primary and secondary components; dual benefits in design expertise and supply security.

Lesjöfors, Dendoff Springs, Sumitomo Electric, Delkor Rail — these specialist suppliers provide critical spring and component capacity, enabling both OEM platforms and aftermarket remanufacture initiatives through custom engineering and localized support.

Recent market events reinforce these competitive dynamics. Large locomotive contracts and fleet modernization deals announced in 2025 underscore continuing investment in advanced bogie and suspension solutions. At the same time, development pauses on some alternative‑fuel rolling‑stock programs illustrate funding and technology risk that can influence suspension optimization pathways.

Material science and systems integration are the primary vectors of technical differentiation in 2026. Suppliers investing in improved rubber‑metal composites for air springs, advanced elastomers for extended fatigue life, and low‑leakage hydraulic fluids for dampers will reduce whole‑life costs for operators. Equally important is the rise of service-enabling technologies: condition monitoring sensors mounted to bogies and dampers, digital twins for fatigue forecasting, and modular designs that simplify field refurbishment.

Certification and testing regimes (ISO/EN and national inspection standards) significantly affect time-to-market and procurement eligibility; early investment in validated test programs reduces commercial friction.

Raw material exposure—particularly steel, elastomers and hydraulic fluids—remains a cost and continuity risk. Suppliers with diversified sourcing, hedging strategies, or material‑substitution roadmaps will preserve margins.

Executives responsible for procurement and supply-chain resilience should prioritize three actions in 2026:

Operationalize tier‑2 mapping: Understand where key materials and subcomponents concentrate and secure alternative sources or contractual assurances for prioritized platforms.

Shift from price-only sourcing to total‑cost‑of‑ownership contracts that reward serviceability, spare-part availability and refurbishment capability.

Accelerate supplier qualification against updated safety standards and certification requirements to avoid project delays during procurement cycles.

For 2026 decision-making we recommend a focused, risk-aware playbook:

OEMs and fleet operators: Prioritize retrofit paths that improve ride quality, reduce maintenance downtime, and lower fuel penalties. Lock in long‑term service agreements with suppliers that can offer remanufacturing and predictive maintenance capabilities.

Tier‑1 suppliers: Move from component-only models to system-plus-service bundles. Invest selectively in digital condition monitoring and modular designs that enable premium aftermarket revenues.

Specialist component makers: Scale by specialization—develop deep capabilities in high‑fatigue materials, rebuildable damper designs, or regional MRO networks to capture steady aftermarket demand.

Private equity and strategic investors: Target consolidation in fragmented niches where scale unlocks R&D investment and procurement leverage; prioritize assets with validated refurbishment and aftermarket cashflows.

The published report is constructed to move stakeholders from insight to execution. Highlights include:

Topline market sizing, historical trends (2020–2025) and a detailed forecast (2026–2032) with scenario sensitivity to raw-material and demand shocks.

A competitive intelligence module profiling incumbent leaders and specialist suppliers, mapped against capability, service portfolio, and aftermarket readiness.

Regulatory and standards tracker outlining inspection, testing and compliance obligations affecting suspension components and bogie systems.

Supply‑chain vulnerability assessment with mitigation playbooks, supplier scorecards and recommended procurement contract terms tailored for 2026 negotiations.

Strategy and M&A toolkit: acquisition target attributes, integration risks, valuation levers specific to suspension component and service businesses.

Note: this release purposefully refrains from reproducing detailed regional or component-level breakdowns. The report contains full segmentation tables and granular scenario outputs intended for subscribers and qualified purchasers.

The 2026 planning horizon rewards operators and suppliers who calibrate capital allocation to both near-term modernization opportunities and the structural aftermarket shift. PW Consulting’s analysis indicates that disciplined investments in durability, serviceability and digital monitoring will translate into defensible margins and recurring revenue streams. For procurement teams, tightening supplier qualification against new standards and securing raw-material continuity are immediate priorities. And for investors, the most attractive targets combine engineering IP with an established refurbishment or aftermarket footprint.

To access the comprehensive dataset, chapter-by-chapter findings, and the proprietary segmentation models that underpin our conclusions, consult the full Train Locomotive Suspension Market report on PW Consulting’s website. The detailed annexes—including certified standards mapping, scenario matrices, and supplier scorecards—are available to report subscribers and enterprise clients.

For detailed analysis of this topic, please visit the official page:Train Locomotive Suspension Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com