Grass-Fed Beef Market Analysis: Premium Meat Demand Fueling Market Expansion

Food |

2026-03-07 08:30:35

PW Consulting’s latest market research — using 2025 as the base year and a historical window spanning 2020–2025 — reframes how executives should approach clinical analytics investments in 2026. The market for IT spending on clinical analytics has expanded rapidly over the past half-decade and PW’s forecast through 2032, underpinned by a 13.45% compound annual growth rate (CAGR), points to continued acceleration in both provider and life‑science spending. This briefing distills the strategic value of the full report for C-suite leaders, procurement heads, and technology strategists who must decide where to allocate scarce capital in an increasingly complex regulatory and infrastructure environment.

It Spending On Clinical Analytics Market

Our top-line sizing shows a trajectory from early‑decade adoption to an enterprise-grade market by the mid‑2030s. The headline CAGR of 13.45% signals that clinical analytics is no longer a niche adjunct to EHRs or imaging systems — it is shaping operational models, reimbursement levers, and clinical workflows. For decision makers, that pace implies two immediate consequences: (1) first‑mover advantages are measurable but fleeting; (2) total cost of ownership (TCO) and vendor flexibility are now primary determinants of sustained value, not simply feature sets.

It Spending On Clinical Analytics Market

AI infrastructure is scaling: independent forecasts indicate hundreds of billions of dollars being placed into AI‑grade infrastructure in 2026. That shifts bargaining power toward vendors and cloud providers that can deliver validated, secure model hosting at scale.

It Spending On Clinical Analytics Market

Hidden infrastructure costs are surfacing: recent analyses identify significant health and environmental externalities tied to data centers — costs organizations must internalize when modeling TCO and ESG impact.

Regulatory complexity is rising fast: new state-level statutes and federal restrictions on bulk transfers of sensitive health data are changing where and how analytics workloads can be hosted and which vendors can participate in cross‑border collaborations.

Together, those forces mean 2026 will be the year many organizations move from pilot projects to enterprise rollouts — but only if they adopt investment frameworks that explicitly price energy, regulatory, and model‑risk exposures.

Validated market sizing and forward scenarios: base‑year and forecast models (2026–2032) with sensitivity analyses tied to AI infrastructure spend, regulatory shock events, and adoption curves.

Decision frameworks for procurement and architecture: vendor selection scorecards, hybrid cloud vs. on‑premise decision trees, and TCO templates that incorporate energy and compliance pass‑throughs.

Operational playbooks: step‑by‑step roadmaps for transitioning pilots into clinical decision support, quality improvement, and population health programs while maintaining clinical governance.

M&A and partnership playbook: prioritized partnership archetypes, integration risks, and value capture mechanisms for buyers and sellers in a market with meaningful but incomplete consolidation.

Quantitative benchmarking and KPIs: proprietary metrics for ROI, time‑to‑value, and model performance that can be applied to vendor negotiations and vendor‑neutral governance.

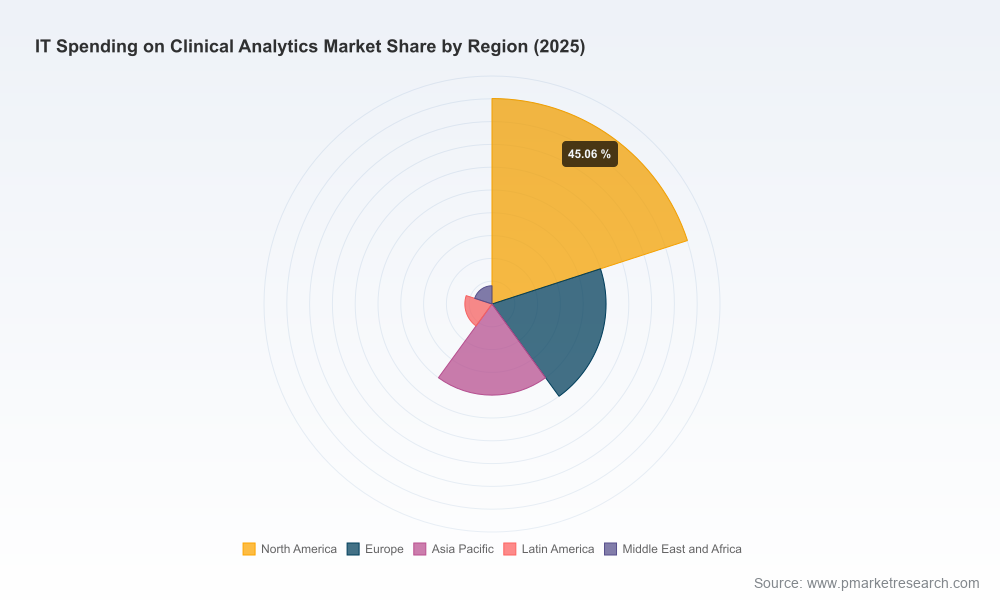

To respect our “trailer” principle, the public briefing above purposefully highlights the types of analytics and tools covered without reproducing the detailed segment‑level dollar sheets and geographic splits — those are reserved for the full report and accompanying data workbook.

The market displays moderate fragmentation — the top three providers account for a meaningful but not dominant share of spend, and the top five extend that concentration modestly. This structure creates an environment where large integrated players compete with focused analytics specialists and services firms. Below are our high‑level assessments of leading participants and what they imply for buyers.

Optum (UnitedHealth Group) — Plays to its strength in claims‑to‑clinical integration. Buyers should expect aggressive platform bundling and deepening value‑based care playbooks; evaluate disaggregation risks if you need vendor neutrality for multi‑payer analytics.

Oracle Health (formerly Cerner) — Continued expansion of analytics capabilities tied to EHR footprints. Their roadmap favors integrated workflows; procurement teams should weigh integration gains against potential lock‑in.

Epic Systems — Enterprise EHR with embedded analytics. Epic’s model favors a cohesive, tightly integrated platform for large health systems, but interoperability demands remain for multi‑system networks.

IQVIA — Strong in real‑world evidence and life‑science analytics; attractive for collaborations between providers and pharma but buyers should confirm data lineage and governance standards for mixed clinical/claims use cases.

SAS Institute — Statistical and AI muscle for complex predictive scoring and fraud detection. Best suited where advanced modeling is a differentiator and in‑house analytics talent exists to operationalize outputs.

Health Catalyst — Focused on integrated data platforms that unify clinical, financial and operational data; appeals to organizations prioritizing quality improvement and cost reduction programs.

GE HealthCare & Siemens Healthineers — These diagnostic and imaging leaders are pushing analytics tied to imaging and monitoring data, extending enterprise analytics into diagnostic pathways and outpatient imaging markets.

Merative (formerly IBM Watson Health), Philips, Veradigm, McKesson — Each offers differentiated propositions — from population health assets to connected care and supply‑chain analytics — and should be evaluated against specific use cases rather than as horizontal substitutes.

Recent market moves validate these dynamics: platform expansions and acquisitions continue to concentrate capability in players that combine clinical data assets with advanced analytics; surveys indicate AI‑centric clinical initiatives are top C‑suite priorities for 2026–2027. Buyers must therefore balance feature‑rich platforms against long‑term vendor flexibility and compliance obligations.

Baseline (most likely): Market follows the modeled 13.45% CAGR with steady enterprise adoption; cloud growth accelerates but hybrid deployments remain common as organizations manage regulatory and energy costs.

Accelerated adoption: Faster uptake driven by breakthrough AI regulatory guidance and demonstrable pilot ROI; platform consolidation increases as large vendors acquire specialized analytics firms.

Constrained growth: Energy policy shocks, restrictive cross‑border data rules, or concentrated vendor pricing pressure slow rollouts; organizations prioritize selective pilots with constrained scope and strict governance.

Each scenario maps to different procurement triggers — from multi‑year enterprise agreements to short‑term modular engagements and focused build‑buy partnerships. The full report includes trigger matrices that translate scenarios into procurement playbooks and investment priorities.

Embed regulatory and energy sensitivity into every financial model — not as footnote inputs but as core assumptions that can flip vendor TCO comparisons.

Prioritize interoperability and data governance in RFPs; demand model‑explainability commitments and data residency assurances for cross‑border analytics work.

Structure procurement as a series of staged commitments (pilot → scale → integration) with clear KPIs and stop/go triggers based on clinical outcomes and cost metrics.

Use vendor scorecards and scenario roadmaps to avoid supplier lock‑in while capturing network effects where scale is genuinely value‑creating (for example, population health registries or payer‑provider analytics pools).

PW Consulting’s market numbers are derived from a bottom‑up view calibrated with primary interviews across providers, payers, vendors and investors, and cross‑checked against public filings and industry forecasts. The report uses a 2025 base year, a 2020–2025 historical window, and models forward to 2032 under multiple sensitivity cases.

In keeping with our “trailer” principle and to protect the commercial integrity of our data assets, this press summary highlights strategic implications and headline market sizing (including the 13.45% CAGR and high‑level forecast trajectory) but intentionally omits detailed segment‑level dollar breakdowns and geographic/application percentages. Subscribers to the full report receive the complete segmentation matrices, vendor scorecards, downloadable financial models, and a proprietary data workbook.

For executives preparing 2026 budgets: use the report to stress‑test your analytics roadmap against regulatory cost shocks, vendor consolidation scenarios, and the true TCO of AI‑grade deployments. PW Consulting’s full market package equips teams with the templates and negotiation playbooks necessary to convert analytics capability into measurable clinical and financial outcomes.

Access to the full report and the supporting analysis is available through PW Consulting’s market research portal. The packaged deliverables include the complete segmentation tables, scenario models, vendor benchmarking spreadsheets, and an executive workshop template to align stakeholders for 2026 execution.

For detailed analysis of this topic, please visit the official page:It Spending On Clinical Analytics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com