Trusted Guide to Stone Paving for Long Lasting and Affordable Builds

Home |

2026-04-07 18:13:06

As commodity markets recalibrate post‑pandemic and regulatory pressure on industrial inputs intensifies, carbonate ores are re-emerging as a critical raw-material battleground. PW Consulting’s Carbonate Ore Market report synthesizes robust historical measurement (2020–2025), a clear 2026–2032 forecast trajectory, and actionable playbooks that will matter to procurement heads, strategy teams, and corporate development groups in 2026. Our modeling shows the global carbonate ore market reached USD 35,349.8 Million in the base year 2025 and is projected to approach USD 50,140.0 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.12% during the 2026–2032 forecast period. This growth profile—combined with a fragmented supplier landscape—creates both opportunity and execution risk for market participants.

Carbonate Ore Market

Market momentum: After steady expansion during 2020–2025, the sector enters a phase of moderate, sustained growth driven by industrial recovery, infrastructure cycles, and specialty applications.

Carbonate Ore Market

Fragmentation advantage: With industry concentration metrics indicating a low top‑tier share, nimble buyers and specialist producers can capture outsized margins through regional consolidation, technical differentiation, or supply‑chain integration.

Carbonate Ore Market

Regulatory and processing inflection points: Environmental and beneficiation mandates—particularly for complex carbonate ores—are reshaping capital allocation and technology choices.

Strategic priority for 2026: optimization of feedstock flexibility, targeted partnerships for beneficiation, and scenario‑driven capex planning to de‑risk supply and meet decarbonization targets.

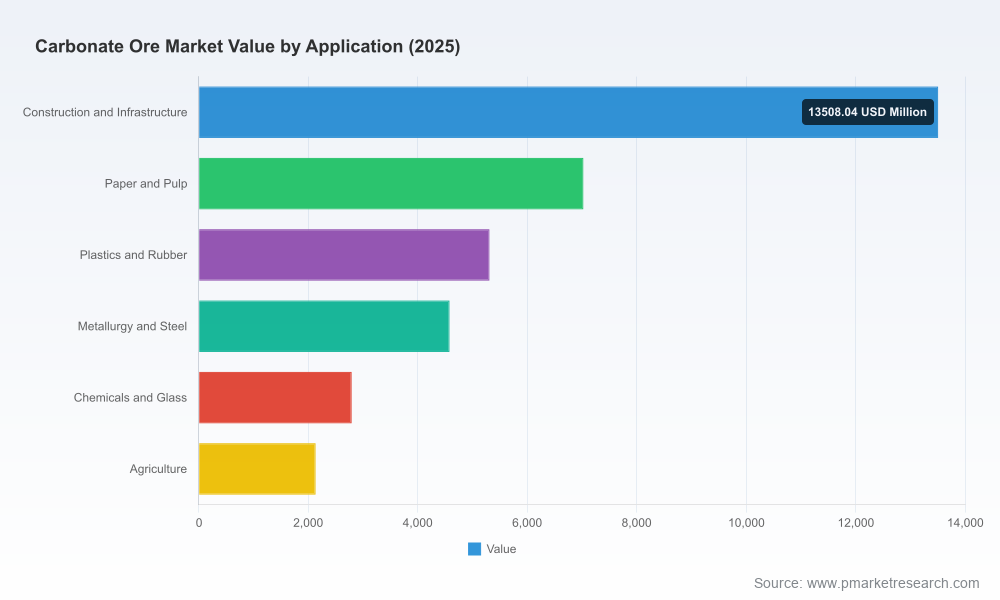

Three structural forces dominate the carbonate ore outlook for the coming planning cycle. First, the baseline demand across construction, industrial processing, and specialty materials continues to underpin steady volume growth. Second, product and processing complexity—ranging from high‑purity precipitated carbonates to magnesite and siderite streams—raise technical barriers that favor players with beneficiation know‑how and process engineering capability. Third, regulatory tightening and environmental scrutiny are elevating the cost of production for lower‑grade deposits, accelerating consolidation of marginal capacities and triggering capex in cleaner processing technology.

Illustrative industry observations included in the report highlight practical implications of these forces: manganese carbonate ores, for example, often require high‑intensity magnetic or gravity separation due to fine intergrowths; talc‑carbonate deposits yield high‑purity talc via specific gravity and liberation characteristics; and siderite, containing substantial iron fractions, commonly undergoes calcination when processed as an iron feedstock. We also integrate reporting that African manganese operations are already facing stricter CO2 and waste‑management requirements—factors that are shifting beneficiation economics and capital allocation.

The carbonate ore sector is populated by diversified industrial miners, specialty mineral processors, and regional aggregates groups. Market concentration indicators point to a fragmented industry structure, creating opportunities for vertically integrated players and technical specialists alike. Key firms analyzed in the report include:

Omya Group (Switzerland) — a global leader in industrial minerals with broad extraction and processing capabilities for calcium carbonate, emphasizing high‑volume filler and coating applications. Their global footprint and application engineering competence make them a bellwether for demand trends.

Carmeuse (Belgium) — a major producer focused on high‑purity limestone and dolomite, with strengths in steel and environmental applications where consistency and regulatory compliance are critical.

Lhoist Group (Belgium) — specializes in lime and dolomite processing with deep exposure to industrial and agricultural markets, and an established presence in lime production value chains.

Imerys (France) — positions carbonate products within a broader performance materials portfolio, targeting engineering and functional applications in plastics, paints, and paper.

Minerals Technologies Inc. (USA) — known for precipitated and ground calcium carbonate solutions tailored for paper, packaging, and specialty chemical applications where particle engineering matters.

Sibelco (Belgium), Graymont (Canada), Mississippi Lime (USA), and J.M. Huber Corporation (USA) — regional leaders that combine resource control with downstream processing and technical service offerings.

CRH plc (Ireland) and Nordkalk (Finland) — building‑materials and regional carbonate suppliers whose integrated aggregates-to-cement capabilities influence local supply balances and project procurement dynamics.

Grecian Magnesite (Greece) and RHI Magnesita (Austria) — specialty magnesite and refractory players serving steel and cement markets where magnesia content and thermal performance drive purchasing decisions.

Our competitive assessment examines each player’s exposure to high‑margin specialty streams versus commoditized feedstock, capital intensity, and likely M&A vectors in a low‑concentration environment. The report also provides directional signals about which firms are best positioned to capitalize on stricter environmental controls and which may be forced into asset rationalization.

Concise market sizing and validated forecasting models (historical 2020–2025; base year 2025; forecast 2026–2032) with scenario envelopes for demand shocks, policy change, and technology adoption.

Supply‑map and asset inventory identifying choke points, trade flows, and logistics cost vectors—presented as interactive maps and downloadable data sheets.

Company profiles and capability heatmaps that compare product portfolios, beneficiation technologies, and downstream partnerships (without disclosing proprietary contract terms).

Cost‑curve and margin analysis across representative carbonate routes to identify potential arbitrage and sourcing targets.

Regulatory & ESG risk matrix covering emissions, waste management, and permitting timelines with recommended mitigation roadmaps for producers and consumers.

Commercial playbooks: procurement strategies, hedging templates, and supply‑assurance KPIs tailored to industrial buyers and specialty manufacturers.

M&A and partnership scanner that prioritizes targets by strategic fit and integration complexity, supported by valuation sensitivities and integration‑risk checklists.

Technology and CAPEX guide detailing beneficiation, calcination, and low‑emissions processing options with payback estimates under multiple carbon‑cost scenarios.

Capital allocation: align brownfield upgrades and greenfield investments with scenario outcomes to avoid stranded asset risk if regulations tighten faster than baseline.

Procurement transformation: shift from transactional sourcing to supplier alliances that embed beneficiation capability and compliance guarantees, reducing exposure to low‑grade feedstock volatility.

Portfolio reshaping: pursue bolt‑on acquisitions focused on specialty carbonates or downstream integration where technical differentiation commands premium margins.

Policy and stakeholder strategy: prioritize early engagement in regions where processing mandates and CO2 constraints are being tightened, turning compliance into a competitive moat.

Our assessment combines primary interviews, proprietary shipment and consumption modeling, and cross‑validation with public filings and third‑party geological databases. Historical base is 2020–2025 with 2025 as the report’s reference year; forecasts extend to 2032 and incorporate sensitivity testing around macroeconomic growth, infrastructure spend, and regulatory tightening. We also integrate domain‑specific technical notes—for example, beneficiation complexity in manganese carbonate streams and calcination requirements for siderite—that materially affect processing cost curves and capex timing.

For 2026, the strategic challenge for firms in the carbonate ore value chain is clear: convert a fragmented market position into resilient, differentiated capability while navigating tightening environmental constraints. PW Consulting’s Carbonate Ore Market report is designed to equip executives with the quantitative models, tactical procurement tools, and M&A prioritization required to make confident decisions. To access the full data tables, interactive maps, and downloadable model workbooks (including the granular segmentation and supplier‑level data withheld in this brief), please visit our report page and download the complete intelligence package.

For detailed analysis of this topic, please visit the official page:Carbonate Ore Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com