Laser Hair Bleaching in Dubai for Fine and Light Facial Hair | Complete Guide

Health |

2026-07-13 05:39:33

PW Consulting’s new Swing Granulator Market report (base year 2025, forecast 2026–2032) provides a focused, decision-ready briefing for executives who must translate machine-level choices into company-level outcomes in 2026 and beyond. The market we model is already substantive — rising from roughly USD 962.3 Million in 2020 to USD 1,300.0 Million in 2025 — and we forecast continued expansion at a compound annual growth rate (CAGR) of 6.2% through 2032, reaching a projected USD 1,980.7 Million by 2032. These macro trajectories matter because capital allocation, supplier selection, product roadmaps, and regulatory compliance plans in 2026 will determine competitive positions across the next business cycle.

Swing Granulator Market

Timing CapEx and retrofits: With the market expansion we expect in 2026, firms that schedule modular upgrades now can capture demand without overcommitting to heavy fixed assets. Our analysis surfaces the "sweet spot" for capital deployment that balances rising demand with inflationary cost pressures on steel and stainless alloys.

Swing Granulator Market

Supplier and design selection under supply-cost volatility: The report translates market growth into procurement scenarios — from single-source certification needs for cGMP pharmaceutical buyers to diversified sourcing plans for food and chemical end-users — helping procurement teams build robust RFQs and evaluation rubrics.

Swing Granulator Market

Aftermarket and service monetization: As installed bases grow, service, spare parts and validation rework become predictable revenue streams. We provide playbooks for turning maintenance into margin, including warranty design, parts kits, and lifecycle analytics.

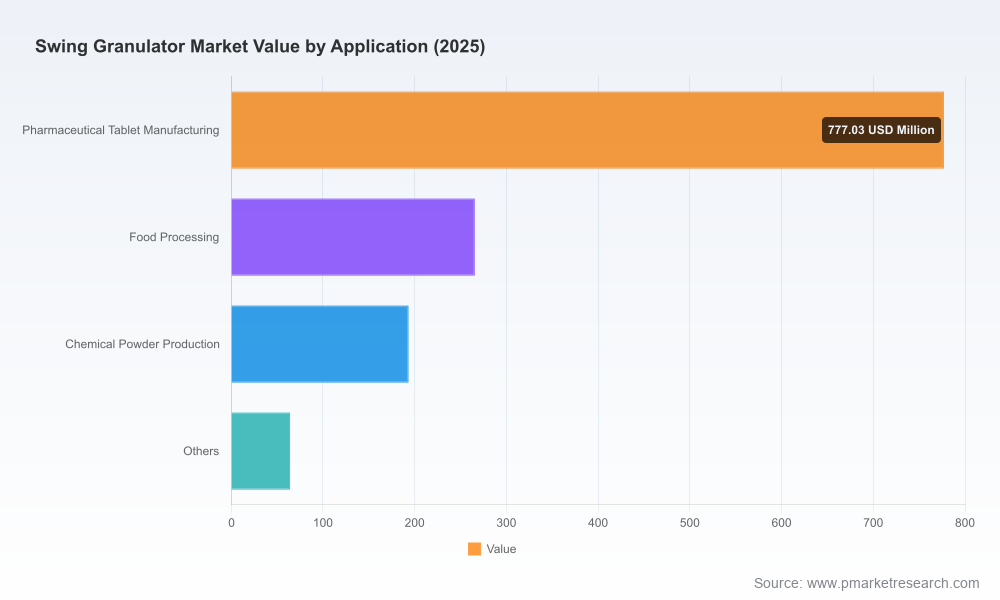

Growth with nuance: The broad market expansion masks heterogeneity by end-use and product architecture. Demand remains anchored in pharmaceutical tablet manufacturing and food/chemical processing, and it continues to favor both wet and dry swing granulation approaches depending on formulation needs. Our report articulates where technology choices drive price realization, regulatory burden, and service intensity.

Regulatory certainty and compliance premiums: Pharmaceutical buyers consistently require cGMP-compliant equipment with hygienic designs, SS316/316L product-contact surfaces, and validation-ready documentation. Machines designed for rapid dismantling, clean-in-place accommodation, and traceable materials command higher ASPs and shorter procurement cycles when accompanied by tested validation packages.

Raw material and input-cost volatility: Early 2026 saw stainless-steel alloy surcharges rise, returning prices to levels last seen in 2024, while hot-rolled coil prices in the U.S. climbed above critical thresholds due to tariff and supply dynamics. These input shocks directly increase manufacturing costs for steel-intensive granulators and shift competitive advantages toward lean designs and alternative-material strategies.

Moderate market concentration: The market is neither atomized nor monopolistic. The top-tier manufacturers command a meaningful share of industry revenue, creating an environment where partnerships, selective differentiation, and aftermarket excellence determine outsized returns. Our competitive heatmaps and CR analyses enable executives to map value-capture opportunities across the ecosystem.

Executive dashboard: A concise view integrating historic performance (2020–2025), our 2026 inflection points, and 2026–2032 scenario bands so leaders can see the range of possible market outcomes and stress-test budget plans.

CapEx decision framework: Quantitative templates that convert forecast demand into machine counts, suggested lead times, and phased procurement calendars. These templates include sensitivity checks for alloy surcharges and tariffs to protect ROI calculations against raw-material swings.

Procurement & validation playbook: Ready-to-adopt RFP language, cGMP validation checklists, supplier audit scorecards, and acceptance test protocols that shorten qualification timelines for pharmaceutical and regulated customers.

Aftermarket monetization model: Practical tactics and KPI templates for turning field service into a high-margin business: preventive-maintenance contracts, parts-bundling strategies, digital remote-monitoring upsells, and retrofitting pathways for legacy machines.

Risk & mitigation matrix: Concrete countermeasures for cost inflation (forward buys, index-linked contracts), supply-chain disruption (dual-sourcing, nearshoring of critical components), and regulatory shifts (modular validation and backward-compatible upgrades).

M&A and partnership playbook: Criteria for target screening, valuation sensitivities for bolt-ons in manufacturing/execution capability, and integration checklists that preserve aftermarket revenues while accelerating product roadmaps.

Our competitive analysis synthesizes public profiles, product portfolios, and observed market activity to produce pragmatic positioning guidance. Seven manufacturers stand out as core participants, each with distinct positioning:

Hywell Machinery (Changzhou, China) — Known for lab-to-industrial YK-series machines, emphasizing stainless construction and broad cross-sector applicability. Their strength lies in product breadth and export-oriented manufacturing, making them a natural partner for distributors seeking scalable platforms.

Lodha International LLP (Ahmedabad, India) — A market-recognized supplier of cGMP-compliant oscillating granulators with SS316 contact parts and high-capacity models. Lodha’s focus on validated equipment and pharma-sector service positions them competitively for regulated buyers and those who value documentation and on-site support.

JUNZHUO Machinery and Tianhe Pharmaceutical Machinery (China) — Both vendors support robust industrial use-cases with established models like YK-160. Tianhe’s recent product catalog updates demonstrate continued investment in thought leadership and portfolio refreshment targeted at lab and production customers.

Wanda Machinery and LK Mixer (China) — These firms are differentiated by integrated equipment suites (mixer, granulator, pulverizer) and vertical value propositions for end-to-end powder processing lines, making them attractive to system integrators and large processors seeking single-vendor responsibility.

Changzhou Yibu Drying Equipment — Active in trade shows and industry forums, Yibu has built visibility with exhibition presence (e.g., ACHEMA) and participation in global supply channels.

Strategic implications for buyers and suppliers:

Buyers should evaluate suppliers for validated documentation and service footprint as much as for unit price — particularly in pharmaceutical use-cases where downtime and revalidation costs dwarf incremental procurement savings.

Suppliers must differentiate beyond commoditized hardware: offering digital condition monitoring, modular retrofit kits, and validation-as-a-service unlock higher lifecycle revenues and protect margins under raw-material inflation.

Global OEMs and regional champions will increasingly partner. For example, show-floor visibility at major trade fairs and product catalog refreshes act as leading indicators of channel focus and geographic ambition.

Lock in critical materials via indexed contracts or supplier-financed hedges and adjust procurement policies to include alloy surcharges in TCO calculations. Our model translates a 10–20% raw-material variance into CAPEX and margin scenarios so CFOs can set funding contingencies.

Prioritize cGMP validation-ready platforms for any pharma-facing pipeline and insist on vendor-provided IQ/OQ/PQ packages to reduce qualification timelines.

Design product roadmaps around modularity: fewer bespoke weldments, more interchangeable subassemblies, and retrofit-friendly control architectures reduce lead times and improve resale value.

Monetize service: introduce tiered maintenance contracts, build a genuine spare-parts availability commitment, and pilot remote diagnostics to increase recurring revenue as installed bases expand.

Use M&A selectively to close capability gaps — focus targets should add manufacturing capacity in low-cost regions with strong service networks or deliver intellectual property (e.g., hygienic seals, low-steel designs) that mitigate input-cost exposure.

PW Consulting’s Swing Granulator Market report is designed as an execution guide for the coming planning cycle. With the market moving from roughly USD 1,300.0 Million in 2025 toward nearly USD 2,000.0 Million by 2032 at a 6.2% CAGR, the choices made in 2026 — about which platforms to standardize on, how to hedge material costs, and where to invest in service — will create multi-year advantages. Our proprietary models, procurement templates, competitive heatmaps, and action checklists reduce uncertainty so leaders can commit capital with confidence.

For a detailed breakdown of segment-level demand, regional flows, supplier scorecards, and the full suite of tools and Excel models referenced above, please consult the full PW Consulting Swing Granulator Market report and companion data pack.

For detailed analysis of this topic, please visit the official page:Swing Granulator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com