How SOC as a Service Protects U.S. SMEs from Rising ICT Cyber Threats with Smarter Security

Cyber Security |

2026-07-06 06:36:29

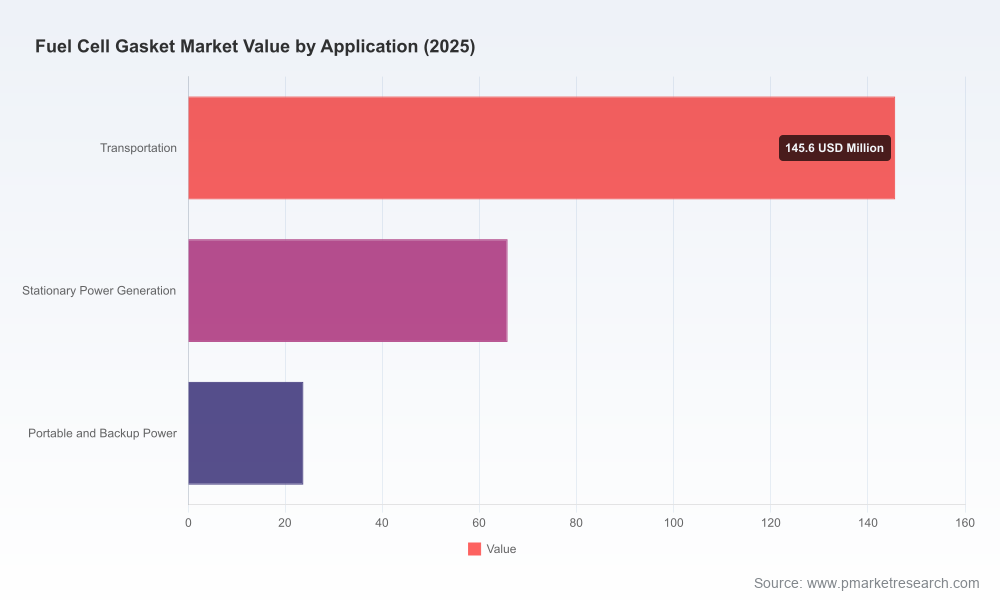

As fuel cell systems move from demonstration fleets to scaled commercial programs, gaskets and elastomeric sealing systems have become a strategic bottleneck — not a commodity line item. Our latest PW Consulting market study positions the global fuel cell gasket market at USD 235.09 Million in the 2025 base year, with a projected compound annual growth rate (CAGR) of 16.5% through the 2026–2032 forecast window. Under the central forecast this trajectory lifts the market into the high hundreds of millions of dollars by 2032, reflecting accelerating stack deployment, higher stack density requirements, and shifting OEM qualification regimes.

Fuel Cell Gasket Market

Investment prioritization: The elasticity of gasket demand relative to stack volume and material mix means capital allocation decisions (R&D, automation, adhesives and curing lines, or strategic inventory) materially affect cost-per-kW and time-to-market for OEMs and suppliers alike.

Fuel Cell Gasket Market

Supplier selection & qualification: Procurement teams face a fragmented supplier base with varying depth in compound science, high‑precision fabrication, and scale capability. Due diligence now must extend to process reproducibility, post-cure protocols, and regulatory traceability for PFAS and other restricted chemistries.

Fuel Cell Gasket Market

Manufacturing footprint & automation: Short-cycle dispensing, UV/dual‑cure chemistries, and thin die‑cutting for high stack compression tolerances are shifting margin pools toward suppliers that invest in process automation and validated assembly lines.

Policy & hydrogen supply linkage: Recent updates expanding recognized hydrogen production pathways are raising the strategic value of vertically integrated supply chains that can respond to clean‑hydrogen procurement incentives.

Designed for executives who must turn insight into executable plans in 90–180 days, the study blends top‑down market sizing with proprietary, operationally focused modules. Key deliverables include:

Scenario model suite — demand scenarios (conservative, central, upside) calibrated to stack deployment, power class, and policy levers; sensitivity levers for raw material cost, cure-cycle time, and warranty claim rates.

Supplier scorecard and shortlist — a practical decision matrix that weights technical competence (compound formulation, permeation resistance, temperature window), production scale, QMS maturity, and manufacturing risk to produce prioritized sourcing lanes.

Manufacturing playbook — step‑by‑step guidance for process scale-up (dispensing, curing, die‑cut/molding throughput), CAPEX sizing, and expected yield improvements from automation and inline metrology.

Cost and margin analytics — BOM-level decomposition, cost-to-serve analysis for contract manufacturing models, and margin waterfalls under alternative materials and process choices.

Technology & materials roadmap — assessment of elastomer classes, trends in PFAS‑alternatives, foil/metal combinations, and recommended qualification plans with test matrices and target KPIs (permeation, compression set, chemical compatibility).

Regulatory & standards impact — interpretation of recent policy shifts and a compliance checklist to accelerate supplier approval and avoid late-stage rework.

Commercial playbook — go-to-market options for incumbent suppliers and new entrants, sample commercial terms, and partner archetypes for JV/co‑development in fast-growing regions.

The market is commercially significant but not monopolistic: leadership is clustered around established sealing and elastomer specialists while an active second tier of materials-focused and regional players pursues niche opportunities. The top three suppliers account for roughly two-fifths of revenues and the top five approach about half the market — enough concentration to reward scale and enough fragmentation to allow fast, focused entrants to win platform business.

Freudenberg Sealing Technologies — A core incumbent with deep elastomer and sealing integration capabilities. Strategic organizational moves in early 2026 have attached hydrogen components into the sealing division and accelerated investment in elastomer mixing capacity at Weinheim. For OEMs, Freudenberg represents a low‑risk partner for systems integration and long‑cycle qualification.

NOK Corporation — Strong in integrated separator/gasket concepts and designs tuned to PEM stack performance. NOK is disciplined on material science and system-level sealing strategies that reduce parasitic leaks and improve stack durability.

Trelleborg Sealing Solutions — Focused on “hydrogen‑ready” materials and validated O‑ring and molded elements. Trelleborg’s materials portfolio and validation protocols are attractive to mobility OEMs concerned with permeation and long‑term stability in H2 environments.

Parker Hannifin — Offers a breadth of fuel‑agnostic sealing technologies and high‑temperature elastomers; relevant where operating envelopes extend toward electrolyzer or high‑temp applications. Parker distinguishes itself on engineered perimeter seals and injection-molded solutions.

ElringKlinger — Brings metal‑elastomer expertise and cross-over experience from battery and e‑mobility sealing, highlighted by product showcases at mobility events. Its system-level perspective is useful for OEMs aligning gaskets with plate and frame designs.

Stockwell Elastomerics and regional specialists (including established Japanese and European manufacturers) — Provide high-performance silicone/HCR, EPDM and FKM formulations tailored for die‑cut and thin‑sheet stack designs; these firms are often preferred for prototype-to-production transitions where material behavior under compression is a gating factor.

Automation and cycle‑time compression: A joint DELO–DATRON system announced in late 2025 integrates fast‑curing liquid gaskets with UV‑curing to shorten dispensing cycle times and improve process repeatability — a clear productivity lever for suppliers aiming to win high‑volume OEM contracts.

Organizational alignment: Freudenberg’s early‑2026 integration underscores a strategic bet on hydrogen components as core to sealing businesses rather than an ancillary activity; expect increased material R&D and vertical coordination with OEMs.

Standards and material substitution: The industry is actively accelerating PFAS‑free formulations and validating alternatives for high‑performance seals; these regulatory and reputational dynamics will shape supplier selection and long‑term material roadmaps.

Policy tailwinds: Expanded recognition of hydrogen production pathways is creating downstream demand certainty for stack makers and, indirectly, for gasket suppliers participating in vertically integrated programs.

Raw material volatility — fluoropolymers and specialty silicones remain cyclic and can create sudden margin pressure if not hedged or mitigated through design changes.

Qualification lead times — OEM qualification processes and long warranty cycles amplify the cost of late design changes; early engagement and shared validation protocols materially reduce time-to-production.

Fragmented standards — inconsistent regional test methods and limited harmonization on PFAS substitutes increase compliance complexity for global suppliers.

For OEMs: institute a two-track qualification program — (A) fast prototype lanes with thin‑sheet suppliers to validate form/fit/function, and (B) concurrent long‑lead qualification with tier‑one sealing specialists focused on production reliability and supply security.

For suppliers: prioritize investments in automation for dispensing and curing, formalize PFAS‑alternative formulations, and standardize test protocols to shorten OEM acceptance cycles.

For investors and M&A teams: target bolt‑on acquisitions that add material science depth (PFAS alternatives, low‑permeation polymers) or automation expertise (inline metrology, fast curing); small strategic acquisitions can materially improve win rates with large OEMs.

For procurement: introduce indexed sourcing for high‑volatility elastomers, lock in multi‑year development alliances rather than single‑project quotes, and require traceability for restricted chemistries.

Quick wins: re‑route R&D spend to curing and process repeatability (highest ROI on stack cost reduction) and implement supplier scorecards that include sustainability and regulatory readiness metrics.

This article is a strategic trailer — it highlights the questions, frameworks, and commercial moves that will define 2026 decision cycles without releasing every granular split. The full PW Consulting Fuel Cell Gasket Market report contains the detailed segmentation matrices, supplier financial benchmarking, regional deployment scenarios, and downloadable spreadsheet models that operational teams use to set budgets, RFPs, and qualification timelines.

If your 2026 plan includes capex for new mixing lines, supplier partnerships for PFAS‑free formulations, or an M&A mandate to buy capabilities instead of building them, the full report provides the data and executable templates to act in weeks rather than quarters.

PW Consulting’s team of materials scientists, manufacturing engineers, and strategy consultants stand ready to brief executive teams on bespoke implications for specific product lines or procurement portfolios. The full report and the scenario model pack are available via our research portal — review the full dataset and download the supplier scorecard to move from insight to procurement action.

For detailed analysis of this topic, please visit the official page:Fuel Cell Gasket Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com