Hair Transplant in Dubai: Your Guide to Fuller Hair

Health |

2026-05-20 06:04:12

PW Consulting’s latest market research brief on Automatic Water Control Valves (base year: 2025; historical window: 2020–2025; forecast: 2026–2032) delivers a forward-looking, actionable perspective designed to inform capital allocation, product strategy, procurement and M&A decisions in 2026. The global market reached approximately USD 1,209.0 Million in 2025 and is projected to continue expanding to roughly USD 1,758.7 Million by 2032 under a base‑case compound annual growth rate of 5.5% across the forecast period. These headline figures frame a steady, investment‑grade growth runway—but the value for corporate decision‑makers lies in the granular, operational levers the report translates from that macro trajectory.

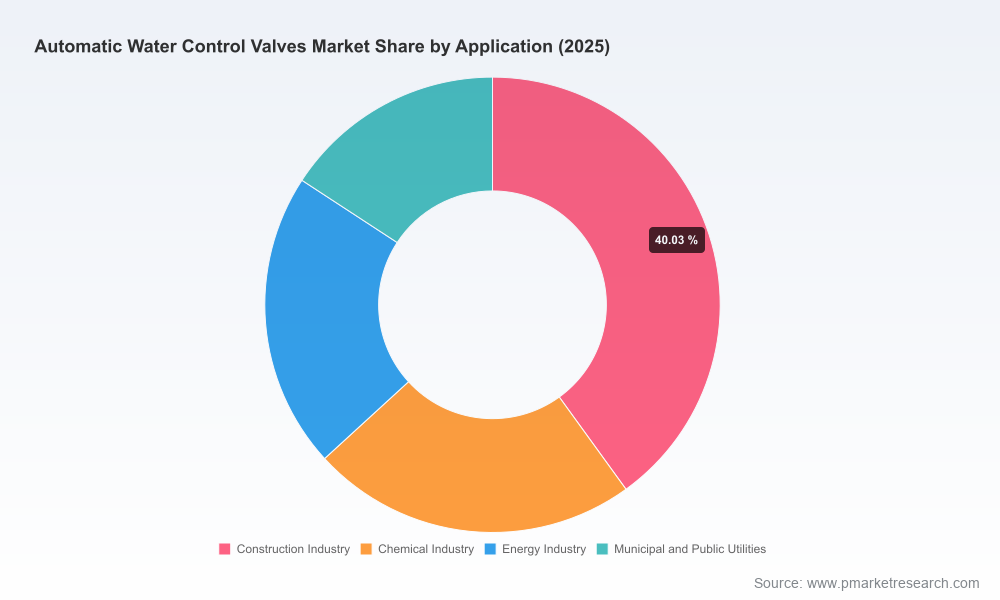

Automatic Water Control Valves Market

It translates aggregate growth into decisions: which product platforms to scale, where to prioritize R&D, and how to stage geographic entry or channel investment to secure payback within typical planning horizons.

Automatic Water Control Valves Market

It aligns technical compliance with commercial strategy: municipal procurement increasingly ties awardability to standards compliance (NSF/ANSI 61, AWWA C530) and domestic content rules such as AIS/BABA; the report maps how compliance timelines affect tender eligibility across major procurement markets.

Automatic Water Control Valves Market

It stress‑tests supply chains: an integrated cost model links metal‑valve manufacturing input pressure to product cost curves—key for pricing, hedging and supplier diversification decisions given recent PPI movements.

It offers transaction intelligence: valuation sensitivity analyses, buyer/seller fit matrices, and consolidation scenarios to support strategic M&A or carve‑out choices.

Market sizing & forecasting engine — transparent methodology, scenario variants (base, upside, downside) and sensitivity to raw material cost and regulatory shifts.

Demand driver diagnostics — technology adoption curves (actuation electrification, smart control integration), end‑market investment cycles, and retrofit vs greenfield opportunity mapping.

Cost and pricing toolkit — bill‑of‑material benchmarks, manufacturing cost stacks, distributor margins and list‑to‑win pricing guidance for competitive tenders.

Supply‑chain risk register — supplier concentration, lead‑time stress testing, and a hedging playbook that quantifies exposure to metal price moves (note: US Producer Price Index for Metal Valve Manufacturing reached 287.312 in April 2026).

Regulatory and standards compendium — compliance checklists for potable water approvals (NSF/ANSI 61), pilot‑operated valve standards (AWWA C530), and domestic content (AIS/BABA) requirements for municipal projects.

Competitive intelligence & procurement playbooks — detailed provider profiles, product positioning matrices, channel economics, and tender‑level win strategies (reverse bidding playbooks, evaluation criteria mapping).

Commercial execution templates — go‑to‑market roadmaps, distributor contract templates, and a project pipeline conversion model for municipal and industrial sales teams.

Case studies and buyer decision trees — real project examples with decision points distilled for quick internal use in commercial reviews and board decks.

Standards and procurement are moving in lockstep. Increasing insistence on NSF/ANSI 61 for potable systems, and the spread of AIS/BABA conditions on US municipal funding, mean product certification timelines must be factored into go‑to‑market schedules and bid eligibility analyses.

Electrification and digital actuation trends are accelerating product differentiation. Buyers are looking beyond basic hydraulic/pneumatic functionality to integrated control, remote diagnostics and energy efficiency—creating a premium tier and aftermarket service opportunities.

Raw material and manufacturing cost volatility materially affect margins. The April 2026 PPI datapoint for metal valve manufacturing (287.312) underlines the need for dynamic pricing models and supplier hedges to protect margin during procurement cycles that can stretch multiple quarters.

Municipal retrofit programs and infrastructure renewals remain durable demand engines. Procurement complexity—specifically certification and domestic content rules—creates windows of advantage for suppliers who align early with compliance requirements.

Cla‑Val (Costa Mesa, CA) — a long‑established technical leader in pilot‑operated solutions. Strengths: deep OEM product breadth and engineering IP for pressure reducing, relief and specialized pilot controls. Strategic implication: strong platform for high‑margin, specification‑driven tenders where engineering differentiation matters.

Flomatic Valves (Glens Falls, NY) — US‑based manufacturer with an emphasis on municipal and wastewater valves, recently refreshing its catalog and certifications. Recent developments include an updated 2026 automatic control valves catalog (effective Jan 5, 2026) and a sequence of product launches and NSF certification updates through 2025–2026 (including AIS/BABA‑compliant models and expanded NSF/ANSI 61 coverage). Strategic implication: a supplier to watch where US domestic content and certified product availability determine tender outcomes.

Singer Valve (Surrey, BC) — focused on water distribution and surge control. Strengths: regional municipal relationships and expertise in pressure management systems. Strategic implication: attractive partner or acquisition target for firms seeking Canadian and specific utility footholds.

Watts Water Technologies (North Andover, MA) — broad commercial and industrial plumbing portfolio, with depth in pressure reduction, level and emergency service products. Strategic implication: scale player with extensive channel access, useful for rapid go‑to‑market and cross‑sell strategies.

Zurn (Milwaukee, WI) — notable for epoxy coated and corrosion‑resistant valve offerings for commercial and industrial settings. Strategic implication: product differentiation in harsh environments and specialty coatings.

BERMAD (Evron, Israel; global operations) — global supplier of hydraulic control valves, irrigation solutions and building systems. Strategic implication: strong position in irrigation and waterworks with global OEM and project credentials.

Immediate (0–90 days): run a compliance gap analysis for your product portfolio against NSF/ANSI 61, AWWA C530 and AIS/BABA rules; fast‑track certification where necessary to preserve tender eligibility in key accounts.

Near term (90–180 days): implement a supply‑chain hedging and dual‑sourcing plan focused on critical metal components; negotiate price‑protection clauses with core suppliers and model the PPI sensitivity scenarios provided in the report.

Commercial: prioritize pilot projects that demonstrate digital actuation and remote diagnostics—use retrofit pilots to create referenceable performance and establish aftermarket service revenue streams.

M&A / Partnerships: use the report’s valuation and strategic fit matrices to shortlist acquisition targets that close capability gaps (e.g., smart controls, certified product lines, regional channel access) and to size integration investment.

This release intentionally omits certain proprietary segment tables, regional share breakdowns and deal‑level financials—material that the full report provides to subscribers and clients. The preview is designed to demonstrate methodological rigor and actionable thought leadership while directing readers to the full deliverable for transaction‑grade inputs.

For executives planning budgets, R&D programs, or acquisition activity in 2026, the market presents a stable growth profile with targeted windows of higher return for actors who move early on compliance and digital productization. The report shows that managing procurement exposure (metal costs, manufacturing lead times), accelerating certifications for potable and domestic‑content markets, and investing in differentiated, serviceable electro‑mechanical platforms will be the primary drivers of outperformance over the 2026–2032 horizon.

PW Consulting stands ready to support tailored strategy workstreams, from rapid commercial due diligence to integration playbooks and procurement optimization sprints. For full dataset access, segment breakdowns, tender‑level win rates and the proprietary valuation models that support the recommendations summarized here, please visit PW Consulting’s report page or contact our industry team to request the complete Automatic Water Control Valves Market report and bespoke advisory engagement options.

For detailed analysis of this topic, please visit the official page:Automatic Water Control Valves Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com