Material Handling Robotics 2026: A Strategic Briefing for Decision-Makers

PW Consulting’s latest Material Handling Robotics Market Research provides an indispensable strategic compass for organizations planning capital allocation, automation roadmaps, and partner selection in 2026. Grounded in a multi-year historical analysis (2020–2025) and a robust forecast framework (2026–2032), the study synthesizes macro growth trajectories, industry dynamics, vendor positioning, and practical implementation playbooks to convert opportunity into measurable value.

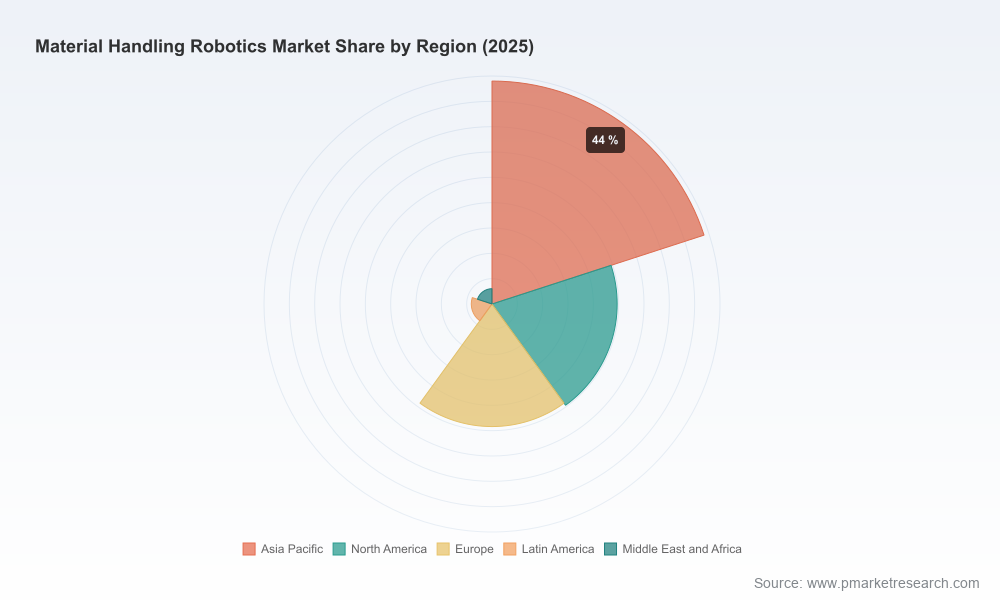

Material Handling Robotics Market Research

Executive snapshot

The global market for material handling robotics has entered a sustained growth phase, with compounded expansion driven by rapid logistics modernization, labor-market pressures, and advances in autonomy and perception. Our base-year analysis (2025) and near-term forecast reflect a high-growth environment characterized by a 15.01% CAGR across the 2026–2032 horizon. The implication is clear: the next 12–18 months are pivotal for embedding automation architectures that will define cost, capacity and competitive positioning through the end of the decade.

Material Handling Robotics Market Research

Why this report matters for 2026 corporate decisions

- Actionable timing intelligence. The study maps the inflection points when pilots should graduate to scale deployments, based on technology maturation, TCO parity thresholds, and supply-chain lead times. For executives evaluating multi-site rollouts, timing is as important as choice of technology.

- Investment prioritization under uncertainty. Using scenario modeling that factors in raw material cost volatility and evolving labor economics, the report identifies resilient investment pathways that preserve optionality while accelerating productivity gains.

- Vendor risk and concentration lens. We quantify market concentration and supplier dynamics to help procurement teams assess supplier lock-in, interoperability risk, and bargaining leverage. The market shows moderate concentration among top-tier players, which has implications for contract structure and long-term service agreements.

- Regulatory and standards readiness. With Industry 4.0 policy thrusts and evolving safety/interoperability standards, our compliance checklists and integration blueprints lower execution risk for 2026 deployments.

- Operational playbooks for rapid ROI. The report’s practical modules—covering pilot design, OEE-linked KPIs, workforce transition plans, and maintenance/ spare-parts strategies—shorten time-to-value and make outcomes measurable and auditable.

What’s inside: practical, deployable intelligence (not just charts)

Beyond topline growth metrics, the report is structured to be a working tool for line-of-business leaders, CIOs, COOs and procurement teams:

Material Handling Robotics Market Research

- Methodology transparency: Data sources, triangulation techniques, sensitivity analyses, and modeling assumptions for the 2026–2032 forecast horizon.

- Scenario planning suite: Upside/downside cases that stress-test capital plans against labor-supply shocks, raw material inflation, and regulatory headwinds.

- Go-to-market and deployment playbooks: Step-by-step guides for pilot-to-scale progression, integration sequencing (controls, WMS/WES, MES), and workforce transition templates.

- TCO and ROI models: Cost calculators that incorporate CapEx/OpEx, downtime exposure, energy and material costs, consumables, and depreciation schedules to produce defensible business cases.

- Vendor scorecards and procurement templates: Comparative criteria, RFP structures, SLAs, and negotiation levers designed to protect long-term uptime and spare-parts availability.

- Integration blueprints: Reference architectures for integrating AMRs, articulated robots, cobots and fixed automation into existing logistics and manufacturing IT stacks without creating brittle dependencies.

- Use-case library and KPIs: Field-proven configurations for order-picking, palletizing, goods-to-person, and internal transport—each mapped to expected productivity and OPEX impacts.

- Regulatory & safety checklist: Actionable compliance steps and certification pathways to reduce field delays and acceptance risk.

Competition and vendor dynamics — who to watch and why

The competitive landscape blends legacy industrial robotics leaders with system integrators and newer AMR specialists. Our qualitative and quantitative analyses reveal distinct supplier archetypes—robot OEMs, intralogistics systems integrators, AMR pure-plays, and industrial vehicle incumbents—each offering different risk/reward trade-offs.

- FANUC Corporation (Japan): A stalwart in articulated robots and end-to-end material handling modules. FANUC’s strengths include deep application know-how in palletizing and automated transfer, broad aftermarket support, and extensive global coverage—making it a strong choice for high-reliability manufacturing environments.

- ABB Robotics (Switzerland): Known for flexible automation stacks and integrated systems for warehousing and intralogistics. ABB’s platform approach favors customers seeking modularity and multi-vendor interoperability.

- KUKA AG (Germany): Offers robotic arms alongside AMRs and transport platforms; the company’s blend of hardware and systems experience suits manufacturers aiming for tight production-logistics integration.

- Yaskawa / Motoman (Japan): Optimized high-speed material handling robots with proven performance in palletizing and transfer tasks—particularly attractive where cycle-time improvement is the primary objective.

- Kawasaki Heavy Industries (Japan): Focus on heavy-payload robotics; a fit for operations that require robust, high-capacity handling for palletized and bulk goods.

- Daifuku Co., Ltd. (Japan): Integrator of conveyors, AGVs/AMRs and robotic modules for warehouses—well positioned for projects that require end-to-end automation rather than point solutions.

- SSI SCHAEFER (Germany), Dematic (KION), Honeywell Intelligrated (USA): Systems integrators with strong intralogistics portfolios. They compete on total solutions—software, AS/RS, conveyors, and robotic picking—and are preferred by large distribution and e-commerce customers.

- Stäubli, Jungheinrich, Toyota Material Handling: Offer differentiated portfolios (precision robots, AMRs, automated forklifts) that appeal to niche needs such as cleanroom environments or fleet automation.

- Geek+, OTTO Motors, Seegrid: AMR-focused players driving innovation in goods-to-person systems and vision-guided navigation—frequently the first port of call for flexible fulfillment centers and production-floor transport modernization.

Our vendor analysis includes capability matrices, service footprint mapping, integration maturity scores and partnership ecosystems—designed to help procurement teams match supplier characteristics to enterprise priorities (speed, uptime, global support, custom integration complexity).

Market dynamics shaping 2026 strategies

- Labor and productivity pressures: Persistent skilled labor shortages are accelerating adoption of robotics to close productivity gaps and reduce reliance on scarce human capital. Companies that integrate automation with reskilling programs capture the greatest long-term value.

- Regulatory and standards evolution: Policy momentum behind Industry 4.0 increases focus on interoperability and safety standards, favoring vendors that publish open APIs and adhere to recognized safety certifications.

- Raw material and component cost exposure: High-grade steel and advanced polymers represent a meaningful share of production cost for robotic hardware—this drives a renewed emphasis on design-for-cost and supply-chain diversification in procurement strategies.

- E-commerce-driven demand: The continuing expansion of fulfillment networks is a structural demand driver for flexible robotic systems like AMRs, goods-to-person solutions, and high-speed sortation robotics.

- Trade-show momentum and product cadence: Recent demonstrations at industry events underscore rapid cadence of feature updates in AMR/AGV autonomy, perception stacks and fleet orchestration software—an important indicator for planners evaluating upgrade cycles versus greenfield deployments.

Strategic recommendations for 2026

- Adopt a portfolio approach to automation: Mix point-solution pilots (AMRs, cobots) with investments in scalable backbone systems (WMS/WES integration, fleet orchestration) to avoid stranded assets.

- Quantify optionality: Use the report’s TCO and scenario models to compare modular rollouts against monolithic build-outs—prioritize solutions that preserve future vendor choice and incremental capacity additions.

- Strengthen supplier governance: Negotiate outcome-based SLAs with clear uptime metrics, spare-parts commitments and migration paths to mitigate concentration risk.

- Plan for workforce transformation: Couple automation with targeted reskilling and cross-training so labor redeployment amplifies, rather than undermines, productivity gains.

- Stress-test supply chains: Incorporate raw-material and component cost sensitivity into procurement hedging strategies and contract terms to limit margin erosion.

How to use this briefing and next steps

This briefing is an executive trailer: it surfaces the strategic contours, vendor dynamics, and operational playbooks that will determine winners in the material handling robotics space through 2026 and beyond. For teams charged with procurement, plant modernization, or digital transformation, the full PW Consulting report supplies the granular segmentation, vendor scoring, scenario data and downloadable TCO models required to execute with confidence.

To preserve the integrity of competitive insight, detailed regional and application-level segmentation is reserved for the full report—this ensures decision-makers receive validated, auditable figures and implementation templates when they engage via our official release channel.

Conclusion

Material handling robotics is moving from opportunity to imperative. With a robust historical foundation and a 15.01% CAGR projected across our forecasting window, firms that align automation strategy with procurement discipline, integration capability, and workforce transformation will secure lasting operational advantage. PW Consulting’s report is designed to move you from strategic intent to executable programs in 2026—delivering the frameworks, vendor intelligence and operational blueprints your teams need to act decisively.

For access to the full dataset, vendor scorecards, and implementation toolkits, please consult the official report landing page or contact PW Consulting’s industry desk.

For detailed analysis of this topic, please visit the official page:Material Handling Robotics Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com