Interesterified Fats Market Size, Share, Current Trends, and Forecast by 2033

Other |

2026-06-10 09:09:01

PW Consulting’s latest market briefing on Fully Wrapped Carbon Fiber Composite Cylinders offers a tactical, decision-ready perspective tailored for executive teams preparing strategies in 2026. Built on a 2020–2025 historical base with a 2026–2032 forecast horizon, the report translates robust market momentum — including a compounded annual growth rate (CAGR) of 12.45% — into practical implications for supply-chain, product, and commercial playbooks. The market, measured in Million USD, has progressed rapidly through the past half-decade and is projected to more than double over the forecast window, presenting both scale opportunities and competitive inflection points for OEMs, material suppliers, and system integrators.

Fully Wrapped Carbon Fiber Composite Cylinders Market

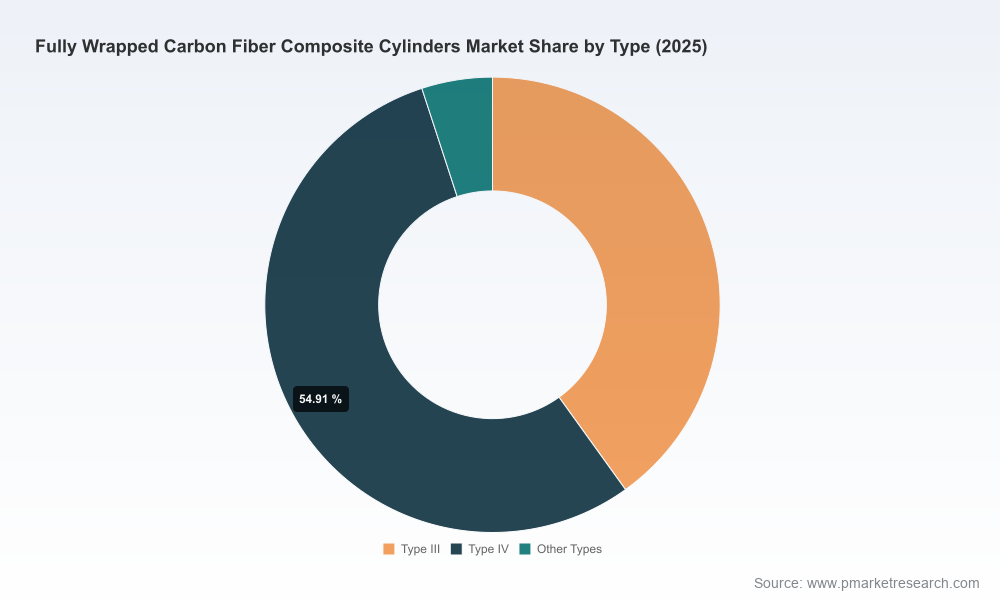

Acceleration of low-carbon mobility and industrial decarbonization is turning high-pressure gas storage from a niche engineering challenge into a strategic platform. Fully wrapped carbon fiber composite cylinders — particularly Type III and Type IV construction — are central to enabling lighter, higher-pressure alternatives for CNG, hydrogen, and specialty gas applications.

Fully Wrapped Carbon Fiber Composite Cylinders Market

From a capital-allocation perspective, the market’s mid-to-high teens structural growth (reflected in the 12.45% CAGR) creates a clear window for capacity investments and vertical partnerships. Firms that secure predictable feedstock, scale manufacturing, and regulatory approvals will capture outsized share as adoption accelerates.

Fully Wrapped Carbon Fiber Composite Cylinders Market

Market consolidation dynamics — where a relatively small number of global players account for a majority share — raise the strategic bar for new entrants and mid-tier suppliers. Competitive moves ranging from facility expansion to aerospace qualification are already shifting the product and customer landscape.

Material and design leverage: Type IV cylinders employing high-density polyethylene (HDPE) liners fully wrapped with aerospace-grade carbon fiber are demonstrating transformative weight advantages versus traditional steel solutions. Independent technical disclosures and product specifications point to structural weight reductions on the order of multiple tens of percent, directly improving vehicle payloads and system efficiencies.

Regulatory authorization as a growth enabler: National approvals and type certifications materially shorten sales cycles for fleet and infrastructure projects. Recent approvals in major markets have opened hydrogen and mobile cascade opportunities that were previously constrained by local certification timelines.

Cross-sector demand migration: Demand is growing not only from passenger and commercial vehicles (CNG, RNG) but also from hydrogen mobility, industrial gas distribution, firefighting/SCBA applications, and emerging aerospace uses. Each vertical imposes distinct reliability, traceability, and testing requirements that influence BOM design and after-sales economics.

Supply-chain sensitivity: Carbon fiber and liner polymers remain the most significant cost and lead-time drivers. Firms with secured long-term supply contracts or in-house prepreg/winding capabilities are better positioned to manage margin volatility during cyclical demand surges.

PW Consulting’s assessment shows a market characterized by moderate concentration — leading suppliers control a meaningful portion of global revenue — yet the landscape remains accessible for specialized and regional producers with differentiated compliance credentials or cost structures. This balance creates three tactical implications for 2026:

Scale and qualification premium: Achieving scale and passing stringent certification gates (e.g., national transport authorities, aerospace integrators) provides pricing power and preferred-bidder status on major infrastructure projects.

Partnerships over greenfield in the short term: For OEMs and system integrators, partnering with established cylinder manufacturers or co-investing in localized production tends to be faster and less capital-intensive than building greenfield capacity, particularly where regulatory approvals are a gating factor.

M&A as a capability play: Expect continued deal activity focused on acquiring certification portfolios, filament-winding expertise, or regional distribution networks rather than pure-volume targets.

The competitive field comprises diversified global manufacturers and regional specialists. PW Consulting’s intelligence highlights the following operator archetypes and what they imply for competitors and buyers:

Global leaders with vertically integrated supply chains: Companies that combine carbon-fiber sourcing, filament winding technology, and broad certification footprints are positioned to win large-scale commercial and infrastructure programs. Recent milestone deliveries and first-time orders into new end-markets illustrate how certification opens premium applications such as aerospace.

European specialists with engineering depth: Manufacturers focused on high-performance Type IV solutions continue to drive product innovation and are frequent partners for premium OEMs and systems integrators where weight and cycle life are mission-critical.

Regional champions and approval-focused players: Local producers that secure national regulator approvals and public-sector contracts can rapidly scale domestically and then expand regionally. Such firms often compete on speed-to-certification and logistics rather than scale alone.

Tech-focused SMEs: Firms that excel in niche segments — e.g., medical, specialty gas, or tactical applications — sustain higher margins per unit by targeting premium, low-volume use cases with stringent testing requirements.

Representative company developments in early 2026 underscore these archetypes: a global supplier marked a milestone by delivering its multi-thousandth cylinder for green-energy distribution and simultaneously secured inaugural aerospace orders to be manufactured in a new facility; a regional manufacturer won a sizable public-sector procurement to supply Type IV CNG cascades; another regional player advanced national certification for hydrogen use, paving the way for domestic market expansion. These moves reinforce a pattern where certification and volume deliveries are mutually reinforcing value drivers.

To translate market growth into executable choices, the full PW Consulting report provides:

Executive decision matrices: action-oriented recommendations for CEOs, Heads of Product, and Head of Supply Chain aligned to 12–36 month investment horizons.

Demand scenario modeling: bottom-up demand runs under multiple adoption paths and macro assumptions, with sensitivity to hydrogen policy, fuel prices, and capital subsidy regimes.

Cost and margin playbooks: component-level cost drivers, normalization of carbon-fiber and liner polymer price inputs, and margin case studies by manufacturing architecture.

Regulatory and certification tracker: a liveable framework showing approval gates, test standards, and time-to-market estimates for major jurisdictions.

Competitive profiles and supplier scorecards: qualitative and quantitative assessments of leading manufacturers, including manufacturing footprints, compliance credentials, and go-to-market strengths.

Risk maps and mitigation levers: practical strategies to de-risk supply chains, manage OEM warranty exposure, and structure long-term offtake agreements.

Prioritize certification pathways. Allocate a discrete tranche of project capital to accelerate regulatory approvals in target markets; this often delivers a faster revenue ramp than incremental capacity expansion alone.

Lock in feedstock flexibility. Negotiate multi-sourced agreements for carbon fiber and liner polymers (HDPE) with price and delivery collars to smooth margin volatility during growth phases.

Pursue targeted partnerships. For OEMs entering hydrogen or aerospace, selective JV or long-term supply contracts with established cylinder manufacturers reduce certification and warranty risk.

Design for circularity and service. Product offerings that include lifecycle services (inspection, recertification, end-of-life recovery) create sticky revenue streams and meet the sustainability demands of fleet customers.

Evaluate M&A as capability acquisition. Prioritize targets that offer certification access, specialized manufacturing know-how, or regional market access rather than chasing headline volume alone.

This briefing outlines the structural drivers, technology inflection points, and competitive behaviors shaping the fully wrapped carbon fiber composite cylinder market as you finalize 2026 plans. For teams building market-entry strategies, supplier negotiation playbooks, or capex frameworks, the full PW Consulting report contains the granular forecasting, segment-level demand curves, supplier matrices, and scenario tools required to convert insight into measurable outcomes. We deliberately limit segment-level numeric disclosure here to preserve the strategic value of the full analysis and to guide stakeholders to the complete dataset and templates available in the comprehensive report.

Contact PW Consulting to request the complete report package, access the interactive forecast model, or commission a tailored briefing aligned to your company’s footprint and strategic objectives.

For detailed analysis of this topic, please visit the official page:Fully Wrapped Carbon Fiber Composite Cylinders Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com