Battery Design And Manufacturing Software Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

As battery-centric industries move from prototyping to high-volume production, 2026 will be a pivotal year for strategic choices that determine competitive position through the next decade. PW Consulting’s new market study — base year 2025, historical coverage 2020–2025, and a forward-looking forecast to 2032 — synthesizes market dynamics, vendor capabilities, regulatory shocks, and implementation playbooks tailored for executives and technology leaders. This preview highlights the report’s strategic value while intentionally withholding granular segment-level figures to guide readers to the full analysis.

Battery Design And Manufacturing Software Market

Executive snapshot: market momentum and concentration

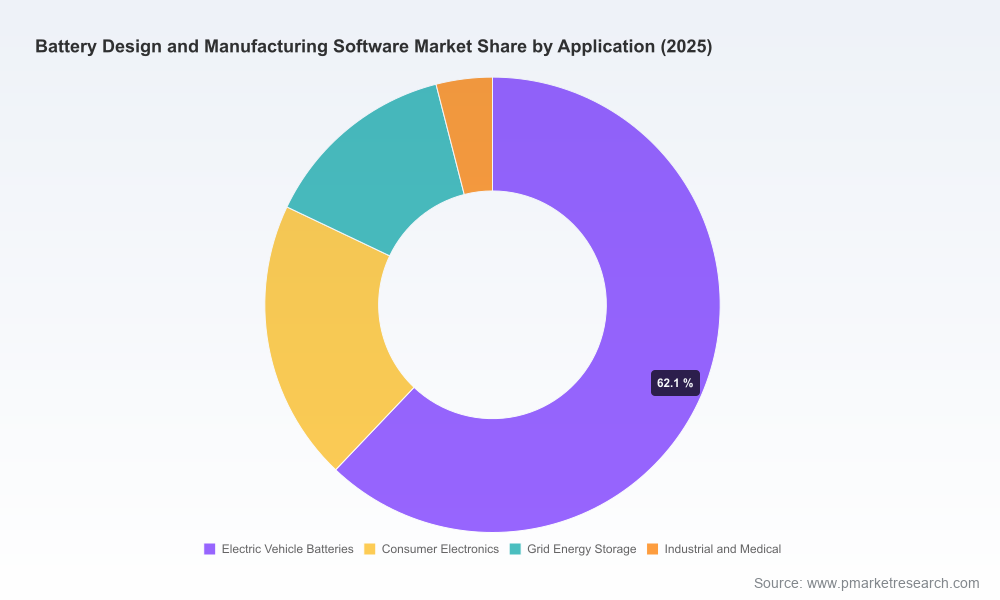

The battery design and manufacturing software market has evolved rapidly: our base-year analysis shows a multi-fold increase in industry revenues across 2020–2025, and the sector is projected to continue expanding robustly through 2032 at a compound annual growth rate (CAGR) of 16.62% over the forecast horizon. Market concentration is moderate: the top three vendors account for a meaningful share of the market, and the top five widen that share substantially, signaling an environment where both global platform providers and specialized disruptors can influence outcomes.

Battery Design And Manufacturing Software Market

Why 2026 is a strategic inflection point

- Regulatory tipping points. New compliance requirements—particularly in the EU and the U.S.—introduce mandatory digital reporting, traceability, and domestic-content screening that will materially affect sourcing, design validation, and software architecture decisions.

- Commercial scale-up. OEMs and cell manufacturers that primarily validated designs in labs are now scaling to production volumes that expose latent manufacturing variability and safety risks. Software investments that once served R&D must now bridge into manufacturing execution, quality, and lifecycle management.

- Technology consolidation. Advances in AI, digital twins, and cloud-enabled simulation are reshaping the vendor landscape, accelerating consolidation among platform providers while creating integration opportunities for best-of-breed tools.

Strategic implications for decision-makers in 2026

For boards, CTOs, and manufacturing leaders, the primary question is not whether to invest in software, but how to sequence investments to balance product performance, regulatory compliance, and manufacturing yield. PW Consulting recommends a three-layered approach:

Battery Design And Manufacturing Software Market

- Architect for traceability and compliance: Prioritize software capabilities that natively support standardized data models and digital reporting to meet EU and other jurisdictional mandates. This reduces retrofitting costs and mitigates supply-chain eligibility risks tied to content rules.

- Invest in hybrid simulation-to-MES workflows: Link cell and pack simulation with manufacturing execution and quality control to shorten time-to-volume and reduce scrap. Emphasis should be on closed-loop feedback between labs and lines—digital twins that carry fidelity from electrode microstructure to pack thermal behavior.

- Leverage AI for differentiation: Deploy AI-enabled analytics to accelerate materials screening, predict manufacturing failures, and optimize BMS control strategies. However, maintain explainability and traceability as non-negotiable design constraints for regulatory acceptance.

Competitive landscape — what leading suppliers bring to the table

The market evidence supports a two-tier competitive dynamic: major simulation and PLM platform providers expanding downstream into manufacturing, and specialist vendors focusing on MES, lab systems, and verification. Key vendors covered in the report include:

- Ansys — known for multiphysics battery simulation that spans electrochemistry, thermal management, and BMS design, enabling faster validation cycles and reduced physical testing.

- Siemens — offers an integrated portfolio that connects cell and pack simulation with digital manufacturing tools. Siemens’ recent portfolio moves strengthen its position as an end-to-end platform provider.

- Altair Engineering — recognized for system-level multiphysics and AI-modeling capabilities; recent product enhancements and strategic alignment with larger platforms have broadened its applicability to safety and manufacturing optimization.

- COMSOL — provides detailed multiphysics modules for electrochemical and thermal modeling across scales, favored by teams requiring highly customizable physics coupling.

- MathWorks — Simulink-based workflows remain central to BMS development, parameterized modeling, and virtual verification in control-centric development streams.

- Dassault Systèmes — leverages platform-level PLM, materials innovation, and virtual twin techniques to connect materials science with manufacturing and lifecycle planning.

- GE Vernova — brings manufacturing execution and smart-factory capabilities targeted at traceability and yield optimization for production lines.

- AVL — focuses on testing lab management and virtual twin solutions aligned with validation and BMS development workflows.

Notable industry moves underscore accelerating consolidation and capability expansion: a high-profile acquisition completed in early 2025 has combined simulation, AI, and HPC capabilities under a single platform; a major vendor released a feature-rich suite in late 2025 emphasizing AI-powered safety and automation workflows; and the industry’s convening bodies are elevating manufacturing-simulation dialogue through dedicated summits in 2026. These dynamics increase the strategic value of vendor selection decisions made this year.

Regulatory and standards dynamics shaping software requirements

- EU Battery Regulation implementation: With digital reporting and IT registration requirements coming into force, software must support standardized formats for technical, chemical, performance, and recycling data submissions. Systems that do not natively map to these formats will face costly integration and compliance delays.

- U.S. content and eligibility rules: Rules tied to tax credits and investment incentives require demonstrable non-foreign content thresholds and supplier reporting. Software that provides immutable traceability from materials to cell and pack will be an operational necessity for eligibility.

- Functional safety and BMS: BMS software must align with functional safety standards and support real-time logging to satisfy lifecycle reporting and the emerging battery passport expectations.

- Technology expectations: Regulators and stakeholders increasingly treat digital twins and AI-based lifecycle calculations as the normative mechanism for carbon accounting and recycling traceability; software roadmaps should reflect this shift.

What PW Consulting’s report delivers (practical, implementation-focused)

The full report is designed to be executable by technology, product, and operations teams. Highlights include:

- Proprietary market-sizing and a seven-year forecast (2026–2032) under alternative adoption scenarios, enabling risk-adjusted investment planning.

- Vendor benchmarking across capability dimensions (simulation fidelity, MES integration, BMS toolchains, AI/analytics readiness, and regulatory-compliance features) with buyer-oriented scoring.

- Operational playbooks for integrating simulation workflows into high-throughput manufacturing, including data governance templates and validation protocols.

- Regulatory mapping and compliance checklists that translate rules into concrete software and data requirements for procurement and vendor contracts.

- Use-case-driven ROI models and a phased migration roadmap to move from proof-of-concept to plant-wide digital twin and MES convergence.

To preserve strategic advantage for our subscribers, the report intentionally refrains from publishing granular subsegment revenue disclosures in this preview. The full report contains those details alongside downloadable decision-support tools and vendor scorecards.

How to use this intelligence in your 2026 planning cycle

- Procurement and vendor strategy: Use the vendor benchmark to structure RFPs around integration risk, simulation fidelity, and compliance readiness rather than price alone.

- R&D and manufacturing alignment: Prioritize pilots that link lab simulation outputs directly into MES and quality systems within the next 12 months to de-risk scale-up.

- M&A and partnerships: Identify capability gaps—AI-enabled materials screening, high-fidelity thermal-electrochemical coupling, or traceability ledgers—that are faster to buy or partner for than to build internally.

- Regulatory readiness: Audit data models today against the EU and U.S. frameworks; automate reporting pipelines to avoid last-minute compliance engineering.

Conclusion — a moment for decisive architecture choices

2026 represents more than incremental change; it is when design, manufacturing, and regulation converge to make software choices strategic assets or existential liabilities. With a market accelerating at a mid-to-high double-digit CAGR and an industry mix that rewards platform interoperability and traceable data, executives must prioritize integrated, compliance-ready software architectures that scale from cell R&D through production. PW Consulting’s full Battery Design And Manufacturing Software Market report provides the granular forecasts, vendor scores, and implementation playbooks required to convert that imperative into executable plans.

For access to the complete analysis, proprietary segment breakouts, and downloadable toolkits referenced in this preview, visit the PW Consulting publications page for the full report and subscription options.

For detailed analysis of this topic, please visit the official page:Battery Design And Manufacturing Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com