Aircraft Collision Avoidance System Market — Strategic Outlook for 2026

Executive summary

PW Consulting’s new Aircraft Collision Avoidance System Market report (base year 2025; historical 2020–2025; forecast 2026–2032) equips executives with a concise, action-oriented roadmap for decisions that will determine market positioning through the remainder of this decade. The global market reached USD 16,148.62 Million in 2025 and is projected to expand at a 6.5% CAGR over 2026–2032, approaching roughly USD 25,094.74 Million by 2032. These headline dynamics reflect an industry simultaneously driven by retrofit cycles on legacy platforms, fresh certification pathways for unmanned systems, and software-first product strategies that unlock recurring revenue models.

Aircraft Collision Avoidance System Market

Why this matters for 2026 decision-making

- Market growth at a mid-single-digit CAGR signals steady demand—but the value is concentrated in technology transitions (software upgrades, ACAS X adoption, and sensor fusion) rather than uniform hardware replacement. Companies that treat 2026 as a tipping point for capability and certification investment will capture outsized returns.

- Regulatory momentum and safety advisories (notably new FAA TSO paths for ACAS Xu and recent NTSB recommendations) elevate certification engineering, system integration, and aftermarket services to strategic imperatives. Time-to-certify will be a primary determinant of commercial traction.

- Competitive concentration indicates room for scale advantages: incumbent suppliers maintain advantages in installed base, avionics integration, and certification relationships, while well-funded innovators can disrupt with low-SWaP, software-driven solutions for urban air mobility (UAM) and UAS markets.

Market dynamics and growth drivers

The market’s forecasted expansion is underpinned by four converging forces:

Aircraft Collision Avoidance System Market

- Regulatory pressure and retrofit cycles. Ongoing airworthiness mandates and evolving ACAS requirements push operators toward upgrades (software and hardware), creating predictable aftermarket revenue windows.

- ACAS X and UAS integration. The ACAS X family—engineered to reduce nuisance alerts and enable mixed manned/unmanned operations—represents both a migration path for large transport aircraft and a new product market for UAS Detect-and-Avoid (DAA) systems.

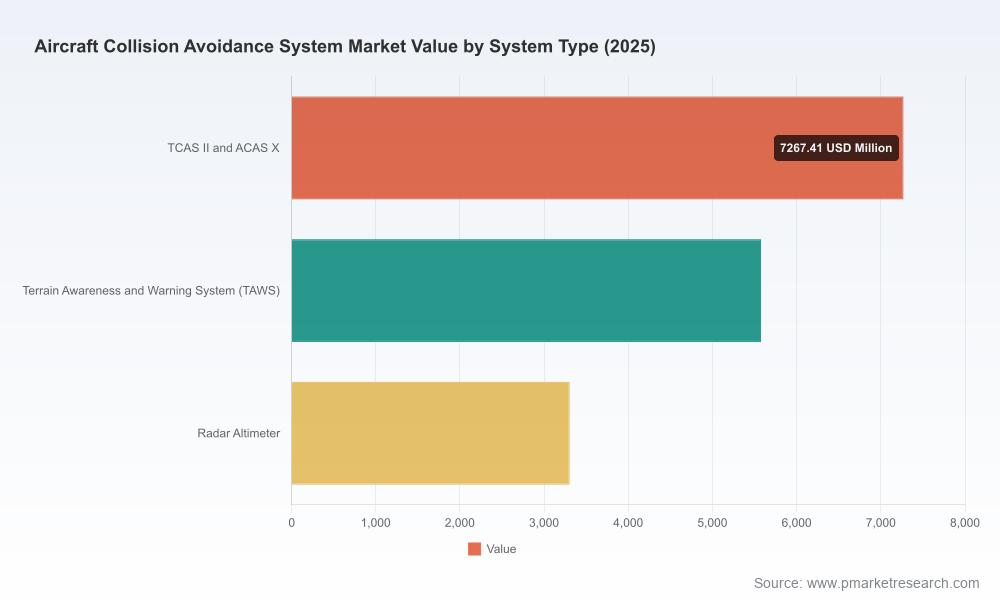

- Sensors and sensor-fusion architectures. Beyond classic TCAS/TAWS/radar altimeters, the winners will be those who deliver robust multi-modal fusion (ADS‑B, radar, EO/IR, onboard sensors) to assure performance in degraded surveillance environments.

- Commercialization of software-centric models. As certification frameworks accept performance-based, probabilistic algorithms, vendors can monetize updates, algorithm licensing, and fleet-level monitoring—changing supplier economics from one-time hardware sales to annuity streams.

Regulatory and standardization environment — implications for strategy

Three regulatory trends will dictate the pace of adoption in 2026:

Aircraft Collision Avoidance System Market

- ICAO and EASA mandates continue to anchor baseline TCAS/ACAS requirements for large, turbine-powered aircraft; compliance remains non‑negotiable for global network access.

- The FAA’s progressive approach—permitting ACAS Xa variants and, as of March 2026, releasing TSOs for ACAS Xu—creates a bifurcated transition window where new certifications and retrofit programs coexist. This window is an opportunity for OEMs and integrators that can offer clear upgrade paths and certification artifacts.

- Recommendations from investigative bodies (e.g., the NTSB) are increasing pressure for faster fleet modernization and broader ACAS X adoption. Operators will require risk- and cost-weighted retrofit plans supported by validated safety cases.

Competitive landscape — what differentiates the leaders

Our report synthesizes supplier strengths, capability gaps, and partnership vectors. Key observations:

- Honeywell International Inc. — Deep avionics integration expertise and broad product families position Honeywell to capture both large transport and business aviation upgrade programs. Its TPA‑100B traffic computer and Change 7.1 compliance-focused products make it a natural choice for operators seeking mature solutions and established support chains.

- Collins Aerospace (RTX) — Long-standing TCAS product lines with software-upgrade pathways lend Collins an advantage in retrofit-heavy segments. Strengths include systems engineered for line-replaceability and avionics-bay friendliness, which reduce downtime for commercial fleets.

- ACSS / Thales — The ACSS joint venture contributes a substantial installed base and proven platform families (including highly integrated T³CAS solutions). This incumbency creates a high barrier to displacement but also makes ACSS/Thales a critical partner for avionics integrators and MRO networks.

- Garmin and Avidyne — Focused on business and general aviation, these suppliers compete on cockpit ergonomics, avionics-suite integration, and cost-optimized TCAS solutions. Their pull-through into retrofit pipelines in the light aircraft segment is significant for market breadth.

- L3Harris — With surveillance and systems integration capabilities, L3Harris is well positioned to deliver solutions that bridge military-derived sensing and commercial ACAS performance requirements.

- Sagetech Avionics — A notable innovator in ACAS X implementations and low-SWaP DAA for unmanned platforms. Sagetech’s work on layered collision avoidance and BVLOS flight research demonstrates the commercialization pathway for ACAS Xu and sXu variants in the UAS market.

Market concentration metrics confirm the presence of strong incumbents: the three largest firms account for a sizable plurality of market revenue, and the top five control a majority. This informs competitive strategy—scale and installed-base services matter—but also highlights niches where focused innovation and regulatory-first offerings can win share.

Recent developments and near-term implications

- FAA TSO Release for ACAS Xu (March 2026): Opens a certification route for unmanned systems. Strategic implication: suppliers should accelerate ACAS Xu productization and pursue early TSO-based approvals to capture first-mover advantages in UAS DAA.

- NTSB Safety Recommendation (early 2026): Increased impetus for ACAS X consideration on currently TCAS-equipped fleets. Strategic implication: operators will seek validated upgrade roadmaps and safety cases—opportunity for consultative retrofit consortia.

- Sagetech collaboration on ACAS X-layered approaches (March 2026): Demonstrates the commercial trajectory for multi-sensor fusion in BVLOS operations. Strategic implication: partnerships between avionics OEMs and sensor/AI specialists will accelerate product readiness for UAM and UAS markets.

- FAA regulatory update (Nov 2025): Signalled phase transition for new TCAS certifications toward ACAS Xa/Xo. Strategic implication: suppliers must map product roadmaps to evolving TSO/AC acceptance timelines to avoid stranded-technology risk.

Strategic imperatives for executive teams in 2026

PW Consulting recommends five pragmatic actions for companies seeking to lead or defend position in 2026:

- Commit to certification-first roadmaps. Allocate engineering resources to ACAS X (Xa/Xu/sXu) certification artifacts, TSO engagement, and interoperability testing. Certification lead-time is now a primary competitive moat.

- Monetize software and services. Build modular upgrade packages—algorithm licensing, fleet monitoring, and OTA update pathways—to convert one-time hardware revenues into recurring streams.

- Form targeted alliances. Pair avionics incumbents with sensor and autonomy specialists to accelerate integrated DAA solutions for UAS and UAM use cases.

- Design retrofit economics. Develop low-downtime swap solutions, financing options, and operator-friendly installation packages to shorten procurement cycles for airlines and large fleet operators.

- Pursue selective M&A to fill capability gaps. Consider tuck-ins that add low-SWaP sensing, algorithm IP, or certification expertise—especially for firms seeking rapid entry into the UAS DAA segment.

What the PW Consulting report delivers (practical, non-redundant content)

Our market study is built for decision-makers and implementation teams. The full report contains:

- Detailed, model-backed market forecasts (2026–2032) with scenario sensitivity to regulatory timelines and retrofit adoption rates.

- An actionable go‑to‑market playbook for OEMs, integrators, and tier‑1 suppliers (pricing archetypes, retrofit packaging, channel strategies).

- Supplier benchmarking and a competitor capability matrix (technical maturity, certification status, installed-base depth, service footprint).

- Regulatory impact assessment with certification timelines, risk heatmaps, and recommended FAA/EASA engagement strategies.

- M&A and partnership playbooks, including valuation lenses for algorithm IP, sensor technologies, and aftermarket platforms.

- Case studies and operational readiness checklists for airlines, MROs, and large unmanned operators pursuing ACAS X/DAA deployments.

- Data annex and methodology: transparent assumptions, growth drivers, and a downloadable forecast model for client use.

Note: This briefing intentionally omits detailed regional and platform-level splits to preserve the report’s role as a strategic gateway. The full dataset and segment-level analytics are available in the paid report package.

Methodology and credibility

The analysis synthesizes primary interviews with OEM and supplier engineering leads, MRO and airline fleet planners, regulatory liaison specialists, and independent flight-safety experts, supplemented by PW Consulting’s proprietary demand-model that reconciles retrofit windows, new-build avionics spec cycles, and UAS commercialization scenarios. Historical data covers 2020–2025 with base-year measurements in USD (revenue unit: Million), and forecasts run to 2032 under multiple regulatory and technology-adoption scenarios.

Conclusion — the practical call to action for 2026

2026 is the year that separates preparatory investments from commercially material adoption in the collision-avoidance ecosystem. The combination of a predictable market growth trajectory (6.5% CAGR through 2032), regulatory catalysts, and nascent UAS certification pathways creates concentrated opportunities for firms that prioritize certification, software monetization, and cross-domain partnerships. PW Consulting’s full report converts these opportunities into executable initiatives—retrofitting programs, alliance roadmaps, and M&A filters—that deliver measurable outcomes for the coming 24 months.

For procurement teams, product leaders, and corporate development executives preparing 2026 budgets and three-year plans, this report is intended to be the operational playbook that turns regulatory and technological change into competitive advantage. Access the full analysis, datasets, and strategic templates at PW Consulting’s report portal.

For detailed analysis of this topic, please visit the official page:Aircraft Collision Avoidance System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com