Skin Pigmentation in Dubai Natural Remedies That Work

Health |

2026-06-05 07:41:24

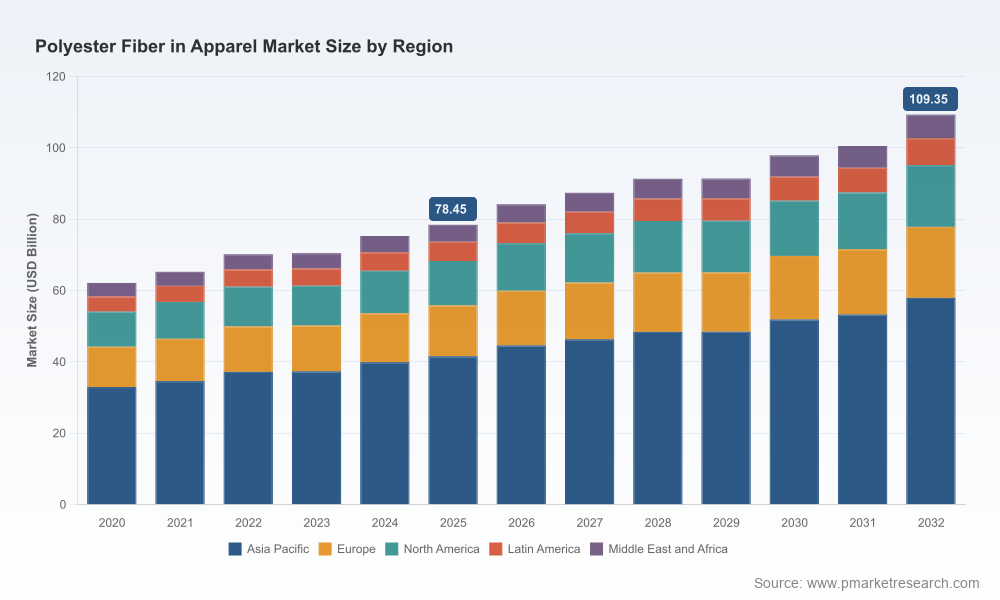

As global apparel markets enter a new cycle of product premiumization and supply‑chain resilience planning, polyester fiber remains the single largest manufactured input shaping apparel cost, performance and sustainability narratives. Our 2026 strategic briefing draws on PW Consulting’s Polyester Fiber in Apparel Market study (base year 2025; historical 2020–2025; forecast 2026–2032) to translate industry dynamics into practical choices for commercial, procurement and investment teams. The market remains on an expansion trajectory—the study’s topline shows steady growth underpinned by an expected compound annual growth rate (CAGR) of 4.86% across the forecast window—pointing to both a scale opportunity and intensifying competitive pressure among differentiated suppliers.

Polyester Fiber In Apparel Market

Timing and trajectories: By 2026 many organizations will finalize capital spend and strategic partnerships that lock in supply profiles for the next five to ten years. Our forecast framework demonstrates how a market that measured in the high‑tens of billions (USD) in 2025 is projected to continue expanding through 2032, creating windows for capacity investments, vertical integration and recycling scale‑ups.

Polyester Fiber In Apparel Market

Margin and mix sensitivity: Polyester remains cost‑exposed to PTA/MEG and crude dynamics. Volatility in feedstock pricing in major supply centers has shown the ability to compress downstream margins rapidly; our report models multiple feedstock‑price scenarios and the implied pass‑through mechanics for producers and apparel brands.

Polyester Fiber In Apparel Market

Regulatory and trade inflection points: From chemical restrictions that affect manufacturing inputs to shifting tariff regimes on man‑made fiber apparel, regulation and trade policy are re‑shaping sourcing economics. The report aligns regulatory timelines with procurement decisions to avoid stranded inventory and non‑compliant specifications.

Sustainability as a commercial vector: Recycled and traceable polyester grades are moving from niche sustainability SKUs to commercial must‑haves. The market’s trajectory signals premium capture for verified recycled products and for brands that can substantiate closed‑loop claims. Our benchmarking of sustainability claims versus cost impact provides practical thresholds for decision makers.

PW Consulting’s market model quantifies total market revenue over the historical period and through the forecast horizon and identifies the macro growth rate cited above (CAGR 4.86% for 2026–2032). The overall market base and projected trajectory make clear that polyester will continue to be the dominant fiber choice for mass and performance apparel segments. For readers who require the granular sub‑segment tables (by region, product type and application) and the sensitivity matrices used to produce these topline numbers, the complete dataset and model are available in the full report.

Feedstock volatility: Recent months have shown rapid PTA and MEG price swings in major production geographies; these movements compress producer margins and create short windows of cost transfer to converters and brands. Effective 2026 procurement requires live feedstock hedging strategies and flexible contracting (indexation + collars) rather than fixed long‑term pricing alone.

Regulatory compliance and process risk: New chemical restrictions that become effective in late‑2026 will force equipment and formula changes across manufacturing and finishing lines—brands and manufacturers must audit spec sheets and supply agreements now to prevent late compliance costs.

Tariff and sourcing pressure: Elevated average tariff exposure for man‑made fiber apparel in some key markets is driving sourcing re‑optimization. The trade landscape favors nimble supply bases with multi‑jurisdictional footprints and vertically integrated value chains that can mitigate duty burdens through origin planning.

Consumer segmentation: Demand for sportswear and athleisure continues to outpace slower categories; functionality (moisture management, thermal regulation) and circularity claims are increasingly purchase drivers. Product innovation that combines performance with verifiable recycled content unlocks higher price points and stronger brand loyalty.

Topline market sizing and probabilistic forecasts (2026–2032) with scenario toggles for feedstock, trade and policy shocks.

Segmental demand models by product type and application, plus a downloadable Excel model for sensitivity testing and internal scenario planning.

Cost‑curve analysis for polyester filament and staple production, showing margin breakevens under alternative feedstock paths and carbon cost assumptions.

Practical go‑to‑market playbooks for buyers, brands and converters: supplier selection criteria, total cost of ownership calculators, and prototype traceability contracts.

Regulatory impact matrix mapping key rules to operational levers and compliance timelines to prioritize capital or process interventions.

Investment and M&A heatmaps highlighting submarkets where scale, integration and sustainability credentials most improve exit multiples.

The supplier universe is a mix of vertically integrated petrochemical‑to‑fiber conglomerates, regional specialists and innovators in recycled and specialty grades. Below are high‑level strategic positions of the most influential players covered in the study.

Reliance Industries Limited (Mumbai, India) — A global integrated polyester producer with one of the largest scale footprints and a clear push into traceable recycled offerings. Recent product launches and specialty fiber innovations position Reliance to capture both volume and premium performance segments. Strategic strengths include backward integration and rapid commercialization of differentiated grades suitable for cold‑weather and performance apparel.

Indorama Ventures (Bangkok, Thailand) — A leading global supplier across staple and filament formats; aggressive moves into chemical recycling and joint ventures to scale textile‑recycled PET show an intention to lead on circularity while protecting market share in commodity PSF and yarns. Their JV activity underscores where industrial capacity and textile circularity intersect.

Toray Industries (Tokyo, Japan) — Focused on high‑value, high‑performance polyester technologies. Toray’s R&D and specialty fiber capability make it a preferred partner for brands seeking functional differentiation (moisture, thermal, durability) beyond commodity pricing pressures.

Chinese integrated groups (Tongkun, Zhejiang Hengyi, Hengli, Sinopec Yizheng) — These players combine large domestic production scale with stepped integration into PTA and downstream spinning. Their cost competitiveness and proximity to major apparel manufacturing hubs make them central to global sourcing strategies; however, sustainability credentials and traceability claims are increasingly the differentiators.

Regional and recycled specialists (FENC, Nan Ya, Alpek, Thai Polyester, Rashni, Everra, William Barnet, Stein Fibers) — This cohort includes firms that provide regional supply security and recycled or specialty products. Several have certifications and process architectures that map well to brand sustainability programs and fast‑moving replenishment cycles.

Partnerships to scale textile‑recycled capacity: Recent joint ventures and capacity commitments from major producers signal that recycled polyester will transition from niche to baseline supply in several large apparel markets. Executives should model the timing of recycled supply into season cycles and forward procurement contracts.

Product launches around traceable recycled polyester and specialty fibers: Offerings that combine verified recycled content with performance claims are shortening the path to commercial adoption by brands; these SKUs carry a price premium but also protect margin in premium apparel segments.

Biodegradable polyester innovations and microplastic mitigation technologies: Emerging technologies may alter the long‑run value chain and regulatory exposure; early commercial pilots will determine which pathways scale at apparel volumes.

Procurement: Shift to blended contracting (indexation + volume collars + sustainability premiums) to balance cost visibility and supply continuity. Shorten lead times where possible and monitor feedstock indicators daily during contract negotiation windows.

Product: Prioritize two product roadmaps—one focused on performance differentiation (sportswear/athleisure) and another on sustainable basics (traceable recycled polyester). Align R&D, certification and marketing timelines so product claims are production‑ready by seasonal launches.

Investment: Target bolt‑on M&A or partnerships in recycled feedstock and chemical recycling where feedstock security can materially improve margin and ESG positioning. Use the report’s investment heatmaps to shortlist targets.

Risk: Build regulatory compliance checklists tied to product SKUs and manufacturing equipment before October 2026 deadlines for chemical restrictions. Factor potential tariff impacts into landed cost models and origin diversification plans.

PW Consulting’s full Polyester Fiber in Apparel Market report contains the granular tables, supplier scorecards, Excel forecasting model and implementation playbooks that procurement, product and corporate strategy teams need to operationalize the recommendations above. This briefing intentionally omits the core sub‑segment tables and breakouts to preserve the commercial value of the full dataset—clients seeking the segment‑level numbers, regional breakdowns and application‑specific forecasts can access them through the PW Consulting report package and model license.

For 2026 planning cycles, stakeholders should: (1) request the PW Consulting Excel model to run organization‑specific scenarios; (2) commission a short supplier due diligence package against shortlisted partners in your supply network; and (3) convene cross‑functional “supply risk and product premium” workshops to reconcile product roadmaps with sourcing and regulatory timelines. Contact PW Consulting’s Textile & Fibers Practice to schedule a strategy session and obtain the full report and data bundle.

For detailed analysis of this topic, please visit the official page:Polyester Fiber In Apparel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com