DC Motor Governor Market — Strategic Outlook for 2026 Decision‑Makers

As PW Consulting’s senior industry analyst, I present a concentrated preview of our newest market research: the DC Motor Governor Market Report (base year 2025, historical 2020–2025; forecast 2026–2032). This research translates hard market data and emerging technology, regulatory and supply‑chain dynamics into practical strategic guidance for executives planning capital allocation, product roadmaps, channel plays and M&A through 2026 and beyond.

Dc Motor Governor Market

Headline market view

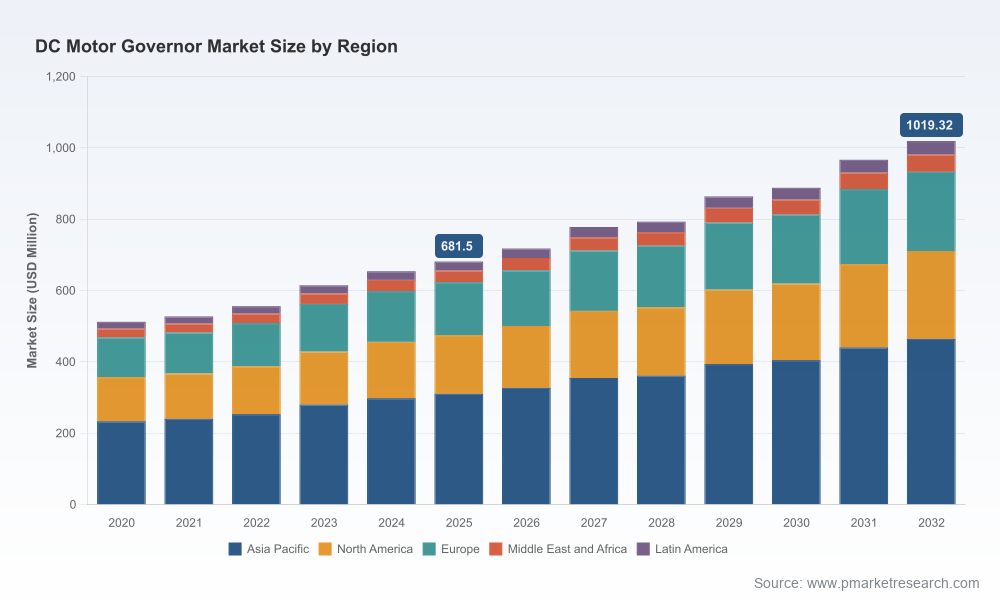

The DC motor governor market demonstrated steady expansion through the first half of this decade and entered 2026 from a position of sustained momentum. In our base year (2025) the market reached a significant scale, and under our central forecast it grows at a compound annual growth rate (CAGR) of approximately 5.92% over the 2026–2032 period, reaching just over USD 1 billion by the end of the forecast horizon. Those topline dynamics reflect both demand-side drivers—industrial automation, energy‑efficiency mandates, and replacement/retrofit cycles—and supply‑side considerations such as power‑electronics availability and component pricing.

Dc Motor Governor Market

Why this report matters for 2026 strategic choices

- Regulatory timing and compliance risk: Recent updates to energy efficiency standards (notably in the U.S. for small electric motors) accelerate deadlines for OEMs and end users to demonstrate compliance. This creates procurement waves for compliant governors and retrofit projects that can be captured with the right product and commercial approach.

- Automation and precision control demand: Manufacturers are specifying more sophisticated speed and torque governance to enable higher productivity and lower energy intensity. This drives premiumization opportunities for governors with digital intelligence and integrated analytics.

- Supply‑chain volatility: The DC governor value chain is sensitive to semiconductor and power‑component availability and pricing. Procurement strategy and supplier diversification will materially affect cost and time‑to‑market in 2026.

- Fragmented supplier landscape: Market concentration remains low-to-moderate, leaving room for focused scale plays, differentiated product launches, and selective consolidation to capture incremental margin.

Practical contents of the full report (what executives will get)

- Proprietary market sizing and validated forecasts (base year 2025; forecast 2026–2032) with scenario variants for conservative, baseline and accelerated adoption paths.

- Demand‑side segmentation by product architecture, application cluster and region (methodology, assumptions and sensitivity analysis included). Note: This preview intentionally omits granular segment figures—these are presented in full in the report to support transaction‑level decisions.

- Commercial playbooks: OEM vs aftermarket GTM strategies, pricing levers, channel margin models and tender‑response templates designed for 2026 procurement cycles.

- Competitive benchmarking and supplier scorecards combining technical performance, service footprint, integration complexity and supply‑risk indicators.

- Scenario modelling tools: EBITDA impact models for product upgrades, retrofit programs and localized manufacturing investments.

- M&A and partnership screening: rule‑based filters to prioritize targets that widen addressable markets, add digital IP, or shore up critical supply components.

- Supply‑chain risk register and mitigation playbook addressing semiconductor exposure, component lead times, and second‑source strategies.

Competitive landscape — strategic implications

The vendor field combines legacy industrial players, specialist drive houses and regional manufacturers. Key firms profiled in our analysis include global systems integrators and drive specialists, each with different advantages and strategic inflection points.

Dc Motor Governor Market

- ABB (Zurich): A leader with deep industrial installed base and advanced DCS800 series drives; strength lies in scale, system integration capability and service networks. Strategic implication: incumbency advantage in heavy industry, but potential exposure to margin pressure in lower‑end retrofit segments—opportunities exist for ABB to monetize advanced features (external field supply options, high current handling) through outcome‑based service contracts.

- Sprint Electric (UK): Known for pragmatic PL/X series products emphasizing reliability and simplicity. Recent trade‑show positioning underscores a focus on accessibility and installation ease—an attractive play for aftermarket channels and machine builders seeking low‑complexity replacements.

- American Control Electronics / Minarik Drives (USA): Focuses on industrial and automation markets with strong North American channel relationships. Their value lies in customizable solutions and responsiveness for retrofit projects; suitable partners for OEMs in regulated markets.

- Parker Hannifin (SSD Drives / Eurotherm legacy): Brings heritage control technology and diversified industrial reach—well placed to bundle governor capability into broader motion‑control systems and services.

- China‑based suppliers (e.g., DZ Gear Motors, C‑lin): Offer cost‑competitive controllers and localized manufacturing scale. They present a meaningful competitive alternative for price‑sensitive end users and are natural partners for volume OEM sourcing or low‑cost retrofit programs.

Recent product and market moves reinforce these strategic themes. Sprint Electric’s emphasis on the PL/X series in 2026 and ABB’s reaffirmation of the DCS800’s field capability signal concurrent market pulls: simplicity and dependable performance on one hand, and high‑current, industrial‑grade governors on the other. For buyers and investors, that bifurcation defines where margin pools are likely to concentrate.

Actionable recommendations for 2026

- Short term (next 6–12 months): Audit existing motor fleets for regulatory compliance gaps and prioritize retrofit candidates with the fastest payback. Negotiate supply agreements with second‑source clauses for key semiconductors and power modules. Pilot digital‑governor trials on high‑value lines to capture energy savings and predictive maintenance data.

- Medium term (12–24 months): Invest in product modularity—develop governor platforms where power electronics, firmware and connectivity modules are interchangeable. Use the report’s supplier scorecards to accelerate supplier consolidation where it improves lead times without sacrificing competitiveness.

- Strategic/long term (24+ months): Consider bolt‑on acquisitions to capture digital control IP or to gain regional manufacturing scale. Explore outcome‑based contracting (energy or uptime guarantees) to monetize performance differentiation.

Risk factors and scenario sensitivities

- Regulatory acceleration: Stricter or faster‑phased energy standards can create demand spikes but also supplier scramble—companies that pre‑certify compliant platforms will win share.

- Component supply and pricing: Semiconductor shortages or price spikes materially affect cost structures for governors; scenario planning should model ±30% swings in key component costs.

- Technology substitution: Migration to brushless DC or integrated motor‑drive systems could change the addressable market; track cross‑industry adoption rates and compatibility standards.

- Competitive intensity: Low to moderate market concentration signals ongoing price competition; margin preservation will rely on product differentiation, service offerings and scale efficiencies.

To quantify competitive positioning, our report includes concentration metrics to help executives evaluate consolidation potential and the feasibility of scale-driven margin improvement. The market today is sufficiently fragmented to enable targeted roll‑ups or regional scale plays.

How to use the report in boardroom and commercial planning

- Embed the forecast scenarios into capex cycles and five‑year strategic plans to align sourcing, product development and service investments.

- Use the vendor scorecards to inform approved‑vendor lists and to structure supplier KPIs tied to lead times, quality and compliance capability.

- Leverage the payback calculators and retrofit prioritization matrix to justify near‑term retrofit budgets under energy‑efficiency programs.

- Apply the M&A screening framework to identify targets that accelerate entry into digital governors or that fill strategic regional gaps.

Closing — why download the full analysis

This preview outlines the tactical and strategic levers executives should consider when acting in 2026. The full PW Consulting report converts these insights into executable plans: downloadable datasets, segmentation tables, supplier scorecards, modelled scenarios and step‑by‑step commercial tools designed for use in procurement negotiations, R&D portfolio prioritization, and M&A diligence. For decision‑makers facing compressed timelines and regulatory pressure, the report is structured to move from insight to action with minimal latency.

To obtain the complete dataset, supplier scorecards and scenario models that underpin these recommendations, please access our full Dc Motor Governor Market report on the PW Consulting report portal.

For detailed analysis of this topic, please visit the official page:Dc Motor Governor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com