Colour Cosmetics Market 2026: Strategic Imperatives for Growth — PW Consulting Preview

As brands, retailers and investors plan for 2026, PW Consulting’s latest Colour Cosmetic Market briefing distils the strategic intelligence executives need to convert momentum into defensible growth. Grounded in our comprehensive base-year assessment (2025) and a forward-looking forecast through 2032, the analysis combines macro market sizing, competitive mapping, regulatory and raw-material risk assessment, and a tactical playbook for market entry, portfolio optimization and channel acceleration.

Colour Cosmetic Market

Executive snapshot

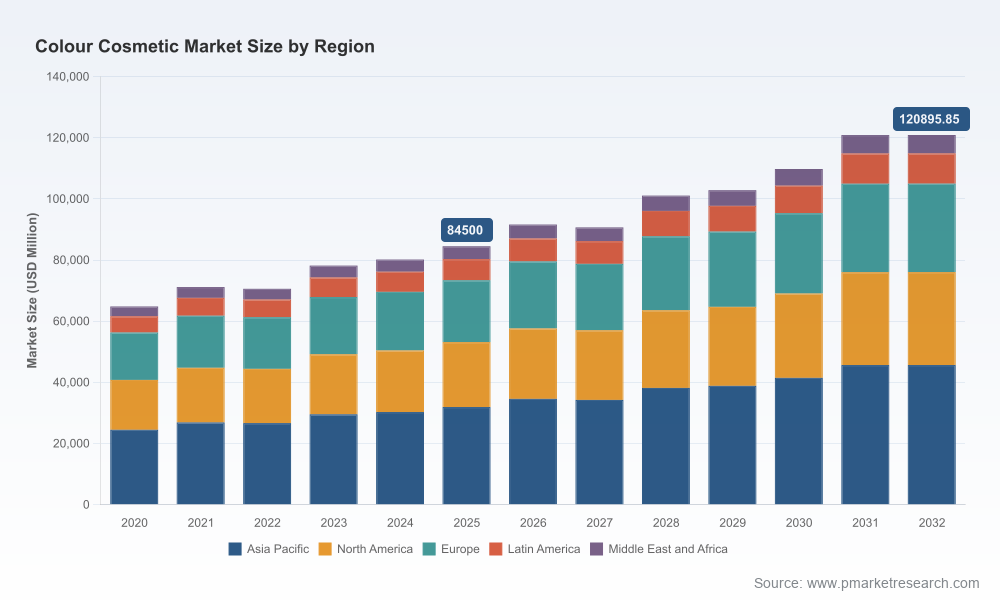

Our model places the global colour cosmetics industry at an advanced scale in 2025 (USD, reporting in Million), with our 2026–2032 forecast projecting a compound annual growth rate (CAGR) of 5.25%. This outlook is calibrated against observed dynamics from 2020–2025 and reconciles near-term volatility (raw-material shocks, regulatory scrutiny, and shifting consumer preferences) with medium-term tailwinds such as digital commerce, premiumisation and sustainability-driven product reformulation.

Colour Cosmetic Market

Why this matters for 2026 decision-makers

- Portfolio prioritization: With steady mid-single-digit growth expected through 2032, executives must shift from broad product proliferation to disciplined SKU rationalization and targeted innovation that maximizes gross margin per square foot (or per digital impression).

- Channel orchestration: The durable coexistence of brick-and-mortar and e‑commerce requires integrated assortment, pricing and fulfillment strategies — not siloed channel plans — to capture conversion across discovery, trial and repeat purchase journeys.

- Regulatory & supply resilience: Ingredient bans, safety assessment regimes and raw-material price shocks are not episodic; they are structural factors that will influence cost curves and product roadmaps. Proactive reformulation and supplier diversification must be treated as strategic investments, not cost centers.

What’s in the full PW Consulting report — practical, operational deliverables

- Forward-looking market size and growth scenarios (base-year 2025, forecast 2026–2032) with sensitivity analyses under alternative macro and commodity-price pathways.

- Go-to-market playbooks for three archetypal players (global prestige house, mass-market CPG, digitally native challenger) covering assortment, pricing architecture, retail economics and campaign calendar optimization.

- Channel blueprints that translate consumer moments into conversion mechanics across offline retail, marketplace platforms, DTC and social commerce.

- Regulatory impact matrix mapping ingredients, regions and recall/notification risk; mitigation templates for reformulation and labeling compliance.

- M&A and partnership heatmaps identifying capability gaps best filled by acquisition vs. alliance (manufacturing scale, clean-beauty formulation, influencer ecosystem access).

- Operational checklists for supply-chain stress testing, raw-material hedging and sustainability-linked procurement strategies.

Key market dynamics shaping 2026 strategy

Several converging forces will define winners and laggards next year. First, the industry’s mid-single-digit CAGR outlook reflects a mature market where incremental growth is earned through innovation that resonates emotionally and functionally. Second, sustainability and “clean beauty” are no longer niche - a strong majority of consumers now expect products free from certain preservatives and endocrine-disrupting ingredients; this preference is rapidly moving from marketing claim to procurement requirement. Third, raw-material volatility has tangible product-cost implications: for example, price disruptions in widely used pigments and white fillers materially compress margin for commodity-driven SKUs unless passed through or absorbed strategically.

Colour Cosmetic Market

Finally, regulatory enforcement is intensifying: established safety frameworks (e.g., EU cosmetic regulation) combined with active national agencies are increasing compliance costs and time-to-market for new formulations. In parallel, digital platforms and social trends continue to be powerful demand multipliers, amplifying product launches that are culturally resonant and visually distinctive.

Competitive landscape — positioning and tactical moves

The competitive map remains populated by a mix of global conglomerates, regional champions and digitally native brands. Market concentration shows meaningful room for independent innovation: the top three players comprise a modest single‑digit share concentration reflective of an industry where brand equity and channel access both matter.

- L'Oréal S.A. (Clichy, France): Continues to combine scale R&D with portfolio breadth — recent product innovation emphasized inclusivity and shade extension, reinforcing the company’s multi-brand, multi-channel playbook.

- Estée Lauder Companies Inc. (New York, USA): Operates with prestige positioning and trade-show-driven demand generation; heritage brands leverage professional artistry and seasonal drops to sustain premium ASPs.

- Procter & Gamble Co. (Cincinnati, USA): Focuses on mass-market accessibility and distribution economics, extracting margin through scale and promotional discipline.

- Coty Inc. (New York, USA): Balances heritage mass-market labels with sustainability messaging, experimenting with recyclable packaging to meet retailer and consumer ESG expectations.

- Shiseido Company Limited (Tokyo, Japan): Plays the premium-innovation card with advanced formulation and regionalized shade strategies, particularly in Asia-Pacific markets.

- LVMH (Paris, France): Commands luxury positioning and selective scarcity to defend high-margin categories and cultivate desirability via experiential retail.

- Revlon, Kao, Oriflame, Natura &Co (Avon) and others: Each pursues distinct routes — mass retail listings, regional direct-sales strength, or niche natural/ethical positioning — creating a vibrant competitive tapestry.

Recent commercial signals corroborate these strategic postures: high-profile product launches and trade-show activations in late 2025 reinforced inclusivity and premiumisation themes; sustainability launches and retail listings indicate portfolio re‑shaping toward circularity and reach. These moves validate our recommendation that 2026 strategies should balance brand-building with operational rigor.

Risks & regulatory watch for 2026

- Ingredient and labelling enforcement: Ongoing restrictions under major safety regimes (for instance, the EU cosmetic regulation framework) mean that compliance programs must be centrally governed and integrated into product development life cycles.

- Supply-side shocks: Raw-material price surges (notably pigments and titanium dioxide) can erode gross margins quickly; adopt hedging, alternative chemistries and supplier redundancy as core defenses.

- Reputational incidents: Regulatory notices and allergen-related warnings in key markets can amplify on social media — rapid-response crisis playbooks and transparent consumer communication are essential.

Strategic recommendations — a tactical playbook for Q1–Q4 2026

- Refine assortment by profitability tiers: Identify and defend high-margin hero SKUs; sunset low-velocity items that consume working capital and shelf space.

- Invest in formulation agility: Shorten reformulation lead times and build modular recipes that allow compliant swaps for restricted ingredients without full product relaunches.

- Double down on digital discovery: Allocate incremental marketing spend to short-form content, creator partnerships and micro-influencer cohorts that demonstrate conversion lift with measurable ROAS.

- Embed sustainability into procurement KPIs: Set supplier scorecards with traceability requirements and recyclable-pack targets linked to commercial incentives.

- Operationalize regulatory intelligence: Create an early-warning dashboard that tracks ingredient listings, agency advisories and cross-border enforcement trends to avoid market access delays.

- Pursue selective inorganic options: Use bolt-on acquisitions to rapidly acquire formulation expertise, manufacturing scale or social-commerce capabilities, prioritizing targets that accelerate time-to-market.

What PW Consulting’s report deliberately withholds — and why

To preserve the commercial value of our full-market intelligence and to encourage direct engagement, this public executive summary omits granular regional and application-level breakouts, detailed segment-by-segment revenue figures and precise channel share tables. The full report contains those resources, including downloadable data tables, scenario models and competitor scorecards designed for board-level decision-making.

How PW Consulting supports your 2026 agenda

Beyond the report, PW Consulting offers accelerated diagnostics, custom benchmarking and implementation sprints: from SKU rationalization workshops to compliance playbooks and M&A diligence. For leadership teams preparing 2026 budgets, we provide rapid-turnaround advisory packages that map our forecast and tactical recommendations to your P&L, inventory plan and marketing calendar.

For access to the complete Colour Cosmetic Market report (full datasets, regional and product segmentation, channel economics and the decision-ready annexes), contact PW Consulting’s industry practice or visit our reports portal. The granular data and executable templates in the full report are designed to convert the strategic signals summarized here into concrete, measurable action plans for 2026 and beyond.

PW Consulting — transforming market intelligence into sustainable competitive advantage.

For detailed analysis of this topic, please visit the official page:Colour Cosmetic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com