Space Lithium‑Ion Batteries Market: Strategic Imperatives for 2026 — PW Consulting Preview

Executive snapshot

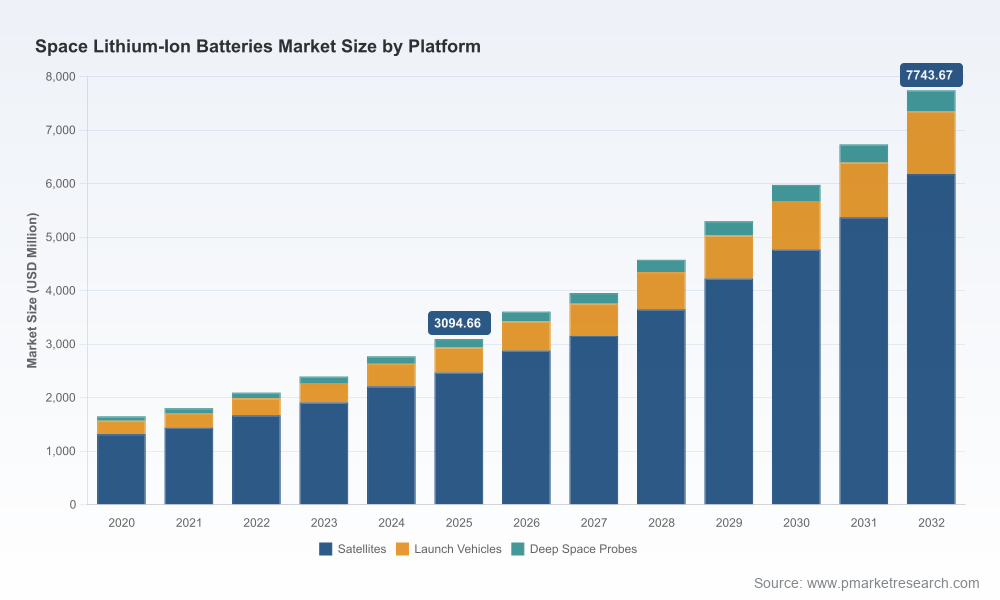

The global space lithium‑ion battery market is at an inflection point. Our base-year analysis (2025) places total market revenues at approximately USD 3,094.7 Million, with a strong compound annual growth rate (CAGR) of 14.0% projected over the 2026–2032 forecast window. By 2032 the market is expected to exceed USD 7.7 Billion under our central scenario, reflecting accelerating demand across telecommunications constellations, government programs (lunar, deep‑space and defense), and a proliferation of enhanced small‑sat platforms. The 2026 juncture is decisive: program timelines, procurement strategies and supply‑chain design established now will determine competitive positions for this entire growth phase.

Space Lithium Ion Batteries Market

Why this report matters to 2026 decision‑makers

- Translate growth into action: connect headline market scale to procurement, engineering and budget decisions that will be executed in 2026–2027.

- De‑risk supplier selection: balance flight heritage, vertical integration and qualification pathway timelines when awarding multi‑year battery contracts.

- Align technology bets and partnerships: prioritize investments in cell chemistries, thermal management and low‑temperature performance most relevant to planned missions.

- Prepare for regulatory and material shocks: embed scenarios for export controls, tariffs and raw‑material price volatility into contractual and sourcing strategies.

What the PW Consulting report delivers (practical, action‑oriented content)

This report is structured to support near‑term program decisions while preserving the tactical detail that procurement, engineering and strategy teams need to act. Key deliverables include:

Space Lithium Ion Batteries Market

- Market sizing and demand model (historical 2020–2025; forecast 2026–2032) with scenario overlays for high/low adoption pathways.

- Topical modules: qualification timelines and test matrices mapped to NASA and major agency standards; lifecycle cost models; and total cost of ownership (TCO) templates for platform integrators.

- Supply‑chain heatmap: critical raw materials, choke points, and supplier dependency indices with supplier‑level exposure scoring.

- Competitive playbooks: supplier capability matrices, flight‑heritage dossiers, manufacturing footprints and technology roadmaps for leading vendors.

- Procurement and contracting strategies: recommended contract constructs (fixed‑price, milestone, performance‑based), dual‑sourcing templates and inventory buffer policies calibrated to project risk tolerances.

- Investment and M&A framework: valuation drivers, integration checklists and target archetypes for strategic acquisition or JV activity.

Note: This preview intentionally withholds the full segment‑level revenue tables and regional/application breakdowns—these granular datasets and the interactive model are available only in the full report.

Space Lithium Ion Batteries Market

Competitive landscape — who matters and why

The market shows a measurable degree of concentration: the top three vendors account for a significant share of revenues (CR3 ≈ 42.5%), while the top five raise that to just under 60% (CR5 ≈ 58.8%). This structure yields both opportunity and risk for new entrants and integrators alike.

- EaglePicher Technologies LLC (United States, https://www.eaglepicher.com) — A long‑standing space battery specialist with deep flight heritage and capabilities in designing large Li‑ion cells for high energy density, long cycle life and mass savings. Strengths: established systems engineering, integration with satellite prime workflows and trusted risk‑reduction practices for critical missions.

- Saft Groupe SA (TotalEnergies) (France, https://saftbatteries.com) — End‑to‑end manufacturer able to control electrodes through system assembly. Strengths: system‑level integration, mature rechargeable Li‑ion flight products and embedded safety electronics suited to extreme environments.

- GS Yuasa Corporation (Japan, https://gsyuasa.com) — Deep cell‑level expertise with substantial in‑orbit energy deployed. Strengths: cell engineering, production scale and proven use by major integrators; recent operational milestones reinforce credibility for large programs.

- EnerSys / ABSL Space Products (United States, https://www.enersys.com) — Pioneer in space Li‑ion and supplier to a broad range of mission sizes, including flagship science missions. Strengths: heritage on long‑duration programs and operational track record under demanding mission profiles.

- Mitsubishi Electric Corporation (MELCO) (Japan, https://www.mitsubishielectric.com) — Focused on spacecraft‑grade cells with long‑term supply relationships to major OEMs. Strengths: reliability, long‑term contracting and cell chemistries designed for sustained mission duty cycles.

- Airbus (Europe, https://www.airbus.com) — Provides module‑level solutions (COSMO‑BATT, STELLAR‑BATT) leveraging qualified commercial cells to achieve competitive cost points with demonstrated flight heritage. Strengths: systems integration at OEM scale, competitive pricing and access to European programs.

- Arotech Corporation and Bren‑Tronics Inc. — Niche and defense‑focused suppliers that act as important alternatives for specialized missions and bespoke engineering requirements.

Recent industry developments and their strategic implications

- GS Yuasa passed a 5.0 MWh in‑orbit milestone with recent launches — reinforcing cell‑level reliability and providing reference performance data for large programs. Implication: primes and agencies will increasingly benchmark suppliers by cumulative in‑orbit energy and mission types.

- KULR Technology Group awarded funding to advance cryogenic/–60°C Li‑ion chemistries for lunar and Mars missions. Implication: mission planners should prioritize flight demonstration pathways for low‑temperature chemistries and budget for extended qualification sequences.

- Lyten selected for an on‑orbit Li‑S demonstration on the ISS — indicating that higher‑energy alternatives are progressing into flight validation. Implication: roadmaps should accommodate parallel technology trials; procurement teams must evaluate migration/refit strategies over program lifecycles.

- Airbus qualified COTS Li‑ion cells for moduleized space battery products — underscoring the commercial advantage of leveraging qualified commercial cells to reduce cost and speed time‑to‑market. Implication: OEMs and new constellations can access lower‑cost module solutions, but must weigh long‑term performance and qualification trade‑offs.

- Macro policy and raw‑material shifts: lithium carbonate prices rebounded materially in 2025, and regulatory actions (notably export controls enacted in late‑2025 on certain high‑energy‑density batteries and precursor materials) have altered supply‑chain dynamics. Concurrent US policy emphasis on tariffs and reshoring adds further complexity. Implication: organizations must quantify exposure to raw‑material price volatility and regulatory dependency when modeling lifecycle costs and sourcing strategies.

- Qualification and safety: NASA’s stringent cell and battery standards continue to drive automated testing, redundant safety systems and extended qualification timelines for crewed and sensitive science missions. Implication: calendar and cost contingencies must include qualification‑driven iterations that frequently exceed traditional commercial schedules.

Strategic implications and recommended actions for 2026

Based on our integrated market, technology and policy assessment, PW Consulting recommends the following priority actions for organizations making 2026 decisions:

- Supply‑chain resiliency: implement a tiered sourcing strategy that mixes a primary flight‑heritage supplier with at least one qualified secondary supplier or module vendor. Negotiate material pass‑throughs and long‑lead contracts for critical cathode/anode materials while evaluating regional sourcing alternatives to mitigate export control risk.

- Qualification‑first program planning: build qualification gates into program schedules as deliverables backed by supplier milestones and reserve windows for rework. For government partnerships, align early with agency standards to avoid late re‑qualification exposure.

- Technology staging and hedging: allocate a portion of R&D and flight‑test budgets to near‑term Li‑ion optimization (low‑temp performance, safety electronics) while pursuing on‑orbit demonstrations for higher‑risk/high‑reward chemistries (Li‑S, solid‑state). Use staged demonstrations to derisk adoption pathways.

- Commercial models and contracting: favor performance‑based contracting with incentives for mass, cycle life and demonstrated in‑orbit performance. For long‑running constellation programs, consider capacity reservation agreements tied to production ramp metrics.

- M&A and partnerships: evaluate bolt‑on acquisitions that provide cell manufacturing control or proprietary material access if strategic roadmaps depend on guaranteed supply or differentiated chemistries.

Immediate 0–12 month next steps: run a supplier exposure audit, model three procurement scenarios (conservative, central, aggressive) using our TCO templates, and initiate at least one flight‑demonstration contract clause for alternative chemistries or thermal‑management innovations.

Closing — how to access the full intelligence

This preview outlines the strategic frame and executive actions our full Space Lithium‑Ion Batteries Market report provides in operational detail. The complete report contains the proprietary segment‑level forecasts, regional and application breakouts, supplier scorecards, interactive financial models and procurement templates necessary to convert 2026 strategy into executable programs. To obtain the full report and our custom advisory services to apply it to your portfolio or program, please visit the PW Consulting report page or contact our space systems practice through the corporate site.

PW Consulting — enabling evidence‑based strategy across the space energy economy.

For detailed analysis of this topic, please visit the official page:Space Lithium Ion Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com