Global Pearl Rings Market Outlook: Emerging Fashion Trends & Business Growth

Other |

2026-07-11 05:29:09

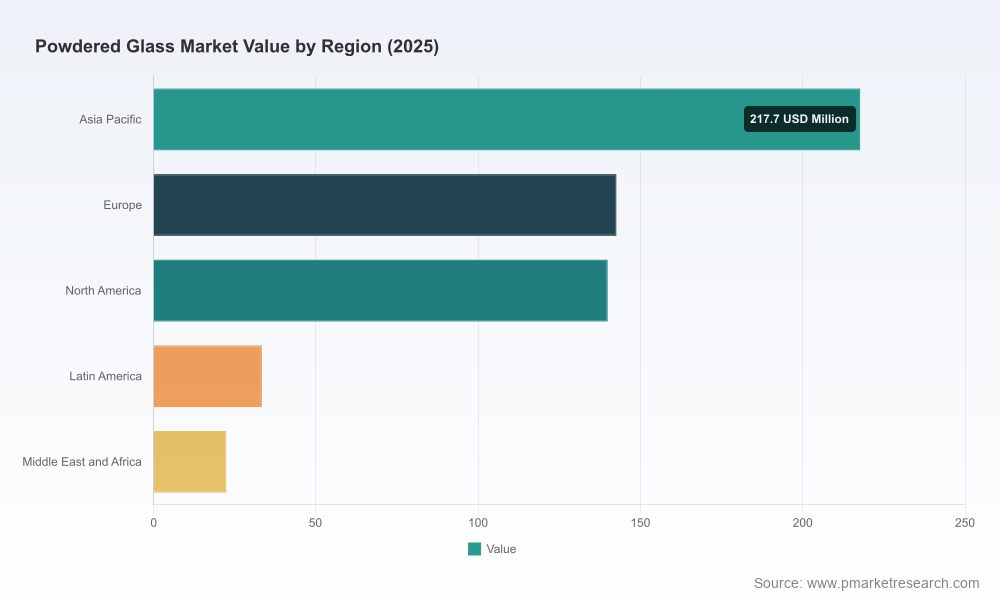

As a convergent material across construction, coatings, electronics and specialty industrial applications, powdered glass is moving from a niche commodity to a strategic input. Our PW Consulting Powdered Glass Market Report (base year 2025) shows a resilient mid-single‑digit compound annual growth rate (CAGR of 5.25%) through the 2026–2032 forecast period. On a macro basis, the market is projected to expand materially beyond its 2025 scale of approximately USD 556 million, reaching roughly USD 796 million by 2032.

Powdered Glass Market

This brief translates those high‑level trajectories into concrete choices for executives planning investments, sourcing strategies, product roadmaps and M&A activity in 2026. It highlights structural forces — supply constraints, regulatory shifts, decarbonization economics, and technology‑driven demand — that will determine which companies win the next wave of margin capture.

Powdered Glass Market

Transition point for scale and specialization: With steady growth forecast, 2026 is when capital allocations toward capacity, ultrafine milling, or recycled feedstock partnerships begin to yield differentiated commercial returns.

Powdered Glass Market

Regulatory inflection: Emerging standards and trade probes are concentrating commercial and compliance risk in specific end‑use pathways — firms that proactively map regulatory scenarios will avoid costly disruptions.

Value chain consolidation opportunity: Moderate market concentration means well‑timed M&A or supply alliances can rapidly shift competitive position without requiring market domination.

Four dynamics will dominate boardroom debates next year:

Feedstock bifurcation — virgin versus cullet: High‑purity virgin formulations continue to command premium margins for electronics and specialty optics, supported by strict upstream material specs (silica sources with >99.5% SiO2). At the same time, recycled cullet is a powerful cost and carbon lever for construction and filler markets because each ton of cullet displaces significant raw material and energy use in glass manufacturing.

Sustainability economics: Lifecycle advantages of recycled glass — including substantial reductions in raw material consumption and energy per ton of glass produced — are rapidly translating into procurement mandates, especially for low‑carbon concrete and specification‑driven construction materials.

Regulatory and trade risk: New standards and investigations are narrowing acceptable composition windows for certain surface products. For example, industry standards have been established to qualify glass pozzolans for concrete, while trade investigations into quartz surface products introduce uncertainty for suppliers selling composite formulations that include glass powder.

Technology differentiation: Ultrafine, highly uniform powders and functionalized bioactive grades are enabling higher‑value applications (medical, dental, advanced electronics). Control of the full milling and particle‑engineering chain — from formulation to patented ultrafine grinding — is now a defensible source of margin.

The powdered glass market is moderately concentrated: the top three suppliers represent a meaningful share of supply and the top five approach a plurality of the market. This structure creates room for both global scale players and focused specialists to thrive. Key strategic archetypes observed in the market:

Vertical‑integrated high‑purity specialists — Firms that control the full process chain from formulation to ultrafine milling are capitalizing on electronics, optics and medical demand. Their competitive play rests on quality, reproducibility and IP in particle engineering.

Circular/feedstock specialists — Producers focused on recycled cullet and post‑consumer streams are winning specification business in construction, polymer fillers and sustainable coatings. Their advantage is cost and embodied carbon reduction, plus compliance with emerging sustainability standards.

Contract manufacturers and toll‑processors — These players service a broad customer base with flexible batch sizes and custom formulations, supporting OEMs and converters that prefer asset‑light supply models.

Representative company cues and strategic takeaways:

SCHOTT AG (Mainz, Germany): Deep competence in specialty high‑purity powders and patented ultrafine grinding positions incumbents to capture premium applications where particle size distribution and functionalization matter. Recent product introductions in bioactive dental powders underscore the value of R&D‑led differentiation.

Corning Incorporated (Corning, NY): Portfolio breadth across formulation types gives scale advantages serving specialty optics and decorative applications. For companies targeting advanced display or optical substrates, securing multi‑year material roadmaps with such suppliers reduces technical risk.

Vitro Minerals & precision recyclers (US): Firms focusing on recycled streams are scaling capacity to meet low‑carbon concrete and filler demand. For construction‑oriented suppliers and specifiers, partnering with established recycled powder processors is the fastest route to meet embodied carbon targets.

Elan Technology, Reade, NEG, AGC and niche suppliers: These players demonstrate the market’s division between specialty, high‑purity supply for electronics and dispensable, volume‑oriented recycled powders for industrial uses. AGC’s multi‑year supply commitments into display supply chains illustrate the commercial premium for ultra‑fine, consistent grades.

Strategic M&A signals: Recent acquisitions and capacity additions by major building‑materials and glass groups reveal a clear intent to secure feedstock and scale recycled processing. Expect deal activity in 2026 around cullet feed access, milling capability and regional logistics footprints.

Below are the primary moves PW Consulting recommends for manufacturers, brand owners and investors preparing to act in 2026.

Source resilience and dual‑sourcing design: Map critical applications to feedstock sensitivity (virgin vs recycled) and design dual‑sourcing contracts that prioritize technical specs and lead times, not just price.

Targeted capacity investments: Prioritize ultrafine milling and particle engineering where technical differentiation yields price premium; prioritize recycled processing lines where volume and sustainability mandates drive adoption.

Regulatory scenario planning: Build a regulatory tracker that models outcomes of trade investigations and product‑specific standards, and stress‑test supply contracts for composition‑related contingencies.

Partnerships over point solutions: For OEMs in electronics and medical sectors, co‑development agreements with high‑purity suppliers reduce qualification cycles and lock in material roadmaps.

M&A and JV focus areas: Targets with proprietary milling IP, reliable cullet sourcing, or specialty formulations for burgeoning bioactive/medical niches will deliver the highest strategic uplift.

Commercial levers: Implement value‑based pricing for engineered powders and total cost of ownership (TCO) models that quantify energy, transport and carbon advantages of recycled alternatives for procurement teams.

The full PW Consulting market study is structured to be immediately actionable for 2026 planning cycles. It contains:

7‑year forecasts (2026–2032) by market tier and end‑use with scenario and sensitivity modules driven by key demand and regulatory variables.

Supplier scorecards and a supplier‑selection toolkit that blend technical capability, capacity, geographic risk and ESG metrics.

Technology roadmaps and a milling/IP landscape that identifies patent clusters and capability gaps across particle engineering domains.

Regulatory tracker summarizing standards, trade investigations and certification pathways that affect product qualification timelines.

M&A target screen and valuation heuristics tuned for the powdered glass value chain (recycled processing, ultrafine milling, and formulation IP).

Raw material sourcing and cost model including silica supply risk, transport elasticity and cradle‑to‑gate carbon accounting for recycled vs virgin routes.

Commercial playbooks (RFP templates, spec language, pilot test protocols) to accelerate qualification and time‑to‑revenue for new material introductions.

2026 is the year powdered glass moves from “commodity management” to “strategic material stewardship.” The market’s steady growth trajectory and the coexistence of premium high‑purity demands with large, sustainability‑driven recycled volumes create distinct playbooks for incumbents and challengers. Companies that align procurement, technical development and M&A activity with scenario‑based regulatory planning will convert a mid‑single‑digit CAGR market into outsized commercial returns.

PW Consulting’s full report provides the proprietary segmentation, supplier analytics and executable tools that senior decision‑makers need to operationalize these recommendations. For organizations planning capital deployment, supplier negotiations or product launches in 2026, the full dataset and targeted annexes are essential. Access to the complete study and the accompanying Excel model is available on our report page.

For detailed analysis of this topic, please visit the official page:Powdered Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com