PVdC Wrap Films Market: Strategic Preview for 2026 — What Senior Leaders Need to Know

As companies prepare budgets and strategic plans for 2026, PVdC wrap films occupy a strategic inflection point driven by steady demand, concentrated supply, and escalating policy pressure on packaging end‑of‑life. PW Consulting’s forthcoming Pvdc Wrap Films Market report synthesizes proprietary modelling and primary research to deliver executive-grade guidance. Below we outline the high‑level market trajectory, competitive dynamics, regulatory pressure points, and the near‑term decisions that will determine winners and laggards — while reserving detailed segment tables and granular forecasts for subscribers to the full report.

Pvdc Wrap Films Market

Market trajectory at a glance

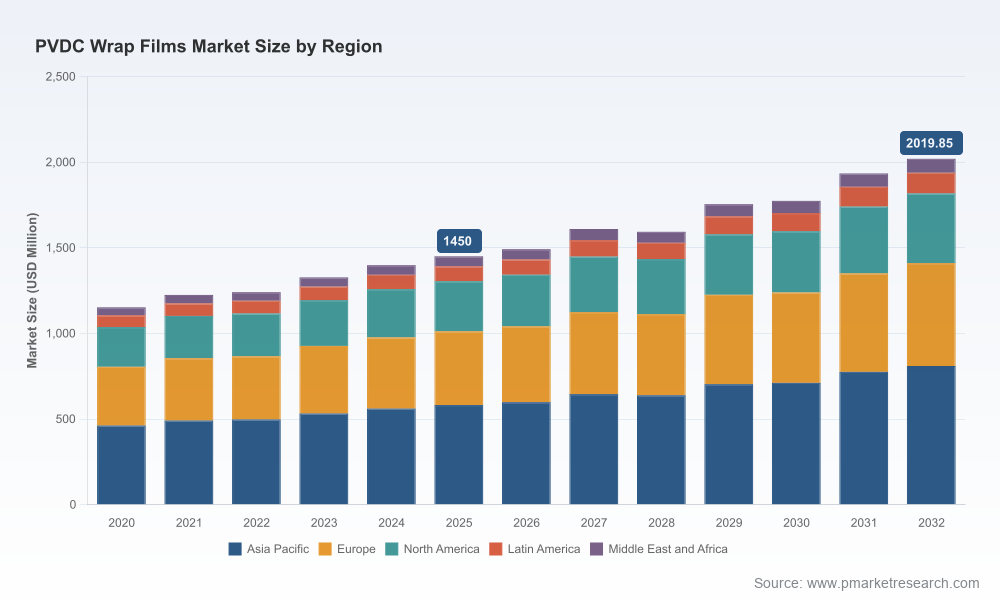

PVdC wrap films experienced consistent growth through the early 2020s and reached a clear commercialization scale by our 2025 base year, with global revenues reported at approximately USD 1,450 million. Our modelling shows the market accelerating at an aggregate CAGR of about 4.85% across the 2026–2032 forecast window, reflecting resilient food‑packaging demand, continued adoption for high‑barrier applications, and selective premiumisation of formats and formulations. By the end of our forecast horizon, the market is projected to surpass two billion USD in annual revenues.

Pvdc Wrap Films Market

From a strategic standpoint, this trajectory signals a growth market that is nonetheless bounded by material complexity and regulatory friction. In short: opportunities exist, but execution risk is material and concentrated.

Pvdc Wrap Films Market

Why this matters for 2026 decisions

- Capital allocation: The mid‑single‑digit CAGR profile supports targeted capacity investments and R&D commitments rather than broadscale greenfield builds. Firms must calibrate spend toward technology and circularity rather than volume alone.

- Portfolio prioritization: High‑barrier applications will continue to justify premium formulations, but evolving EPR and recyclability requirements will force tradeoffs between barrier performance and end‑of‑life impact.

- M&A and partnerships: Market concentration persists; the top-tier suppliers hold a substantial share of revenue and technological know‑how. Acquisitions and joint ventures focused on resin supply, recycling enablement, or formulation IP will accelerate strategic moats.

Segmentation and supply dynamics — what to watch

The market is segmented by film type, application and region; these sub‑markets display materially different drivers (e.g., meat casings vs. dairy wrap, mono‑layer vs. multi‑layer constructions). Our full report contains the granular split tables and a dynamic supply‑demand model. In this preview we highlight three cross‑cutting dynamics that should shape 2026 playbooks:

- Feedstock volatility: PVdC feedstock has shown notable price variability recently, with regional differentials and spikes that have altered margin profiles for converters. Procurement strategies should include indexed contracts, strategic stocking, and supplier diversification.

- Layer engineering versus mono solutions: Multi‑layer PVdC constructions remain the default where ultimate barrier performance is required; mono‑layer solutions have improved but are not universally substitutable. The choice between these architectures affects recyclability, cycle times and co‑extrusion complexity.

- Concentration and switching costs: Market concentration among a handful of technology‑led suppliers means switching involves both technical validation and commercial negotiation. Buyers must quantify switching costs and certification timelines before committing to alternative suppliers.

Competitive landscape — profiles and implications

Our company reviews focus on firms that combine formulation IP, scale manufacturing and market access. Key players profiled in the report include established resin suppliers and specialized film manufacturers — each pursues a different route to commercial advantage:

- Specialist converters (e.g., Dongguan Lingyang Packaging): These players leverage application‑specific knowledge — such as sausage casings and microwave‑safe formats — to lock in food processors. Their advantage is application intimacy; their challenge is upstream resin security and margin pressure from rising feedstock costs.

- Technology‑led resin producers (e.g., Syensqo/Ixan): Resin incumbents control formulation IP and are investing in circularity. Recent mechanical‑recycling trials for multilayer films show potential to materially change end‑of‑life options for PVdC‑containing laminates — a development with broad implications for specifiers and regulators.

- Integrated film manufacturers (e.g., Kureha, Flexopack): These firms combine R&D and manufacturing scale for drop‑in food packaging solutions. Kureha’s recent multi‑billion yen investment in next‑generation PVdC R&D underlines a strategic bet on sustained demand for high‑barrier films despite sustainability headwinds.

- Raw material specialists (e.g., Shandong Aosen): Suppliers of PVdC resins and intermediates are critical nodes; their capacity and pricing behavior influence converter margins and contractual structures.

Collectively, the top tier of suppliers captures a significant portion of market revenue, creating both predictable supply channels and potential bottlenecks for new entrants. Our competitive scoring matrix (in the full report) quantifies technology breadth, geographic footprint, sustainability readiness and commercial flexibility — the four axes that will determine commercial wins through 2026.

Regulatory and sustainability dynamics shaping the market

Policy changes in North America and Europe are the single most important non‑commercial risk for PVdC value chains. Several US states have introduced or expanded Extended Producer Responsibility (EPR) schemes and packaging legislation, with rolling implementation through 2025–2027. Meanwhile, some jurisdictions are moving beyond traditional EPR to include source‑reduction targets and recyclability criteria that could disfavor non‑recyclable or chlorine‑containing chemistries.

At the same time, industry players are responding: recent recycling trials and formulation investments indicate a multi‑pronged response — technical fixes to enable mechanical recycling of multilayer films, investment in next‑generation PVdC chemistries, and reformulations toward less contentious polymers where economically feasible. Historically notable product reformulations (for example, earlier consumer‑packaging shifts away from PVdC) illustrate that market leaders can be proactive — but only when alternatives meet performance and cost thresholds.

Operational and commercial playbook for 2026

Based on our analysis, we recommend a prioritized set of actions tailored to different types of market participants. These are practical, time‑phased steps that can be executed in 2026, with ROI horizons varying by initiative:

- Manufacturers / Converters: Re‑baseline procurement to include feedstock‑price collars and dual‑sourcing; invest modestly in pilot recycling or reclaim partnerships; accelerate qualification programs for alternative chemistries where regulatory risk is highest.

- Brand owners / Retailers: Fund specification roadmaps that map barrier needs to recyclable alternatives; pilot closed‑loop programs in priority SKUs; engage suppliers on EPR scenarios and cost passthroughs.

- Resin producers: Prioritize R&D with recyclability metrics, and secure long‑term offtake or licensing models with converters; consider targeted investments in mechanical recycling validation and scale‑up.

- Private equity / M&A teams: Screen targets for three attributes: proprietary barrier IP, contractual customer stickiness in food processing verticals, and demonstrable pathways to improved end‑of‑life outcomes.

What PW Consulting’s full report contains (actionable highlights)

Our Pvdc Wrap Films Market report is built as a decision‑support toolkit for 2026 planning. Key deliverables include:

- Dynamic market model (2020–2032) with scenario toggles for EPR stringency, feedstock price shocks, and substitution rates.

- Regional and application split tables, plus a supply‑chain heatmap identifying single‑point failures and near‑term pinch points.

- Competitive benchmarking with capability scores, recent transaction summaries, and partnership playbooks.

- Regulatory scenario library mapping state and national EPR rules to potential compliance costs and specification impacts.

- Commercial playbooks: procurement templates, pilot design briefs for recycling initiatives, and go‑to‑market guidance for launching reformulated products.

- M&A diligence checklist and valuation sensitivities driven by resin pricing and regulatory exposure.

To preserve the strategic value of the research for paying clients, we have omitted full segment tables and granular regional/application allocations from this preview. Those datasets, access to our interactive model, and the primary interview annex are available in the full report.

Final strategic recommendations for leaders planning 2026

- Adopt a mid‑path investment stance: prioritize R&D for recyclability and selective capacity upgrades rather than broad capacity expansion.

- Lock in resilient supply arrangements and embed price‑index hedges to protect margins against feedstock volatility.

- Engage proactively on regulatory trajectories — model EPR impact under multiple jurisdiction scenarios and allocate budget now for compliance and design changes.

- Use targeted pilots to validate mechanical‑recycling pathways or alternative chemistries before scaling — incremental data will unlock larger commercial commitments.

- Evaluate strategic M&A or JV options focusing on resin IP, recycling assets, or high‑value application know‑how to accelerate time‑to‑market.

PW Consulting’s Pvdc Wrap Films Market report equips senior leaders with the evidence and decision tools necessary to navigate a market that is growing, technically complex, and policy‑sensitive. For the full data tables, model access, and the complete competitive annex (including transaction models and supplier scorecards), please consult the full report on our website or contact your PW Consulting account lead.

For detailed analysis of this topic, please visit the official page:Pvdc Wrap Films Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com