Revealed: Cut Resistant Gloves Market Positioned for Notable Expansion by 2035

Other |

2026-05-27 11:17:34

PW Consulting’s latest market research, Semiconductor Packaging Electroplating Solution Market (base year 2025), delivers a decision-grade briefing for executives shaping strategy in 2026. The market is on a sustained growth trajectory — expanding at a mid-to-high single-digit CAGR (9.5% projected through our forecast horizon) and accelerating from under USD 1.0 billion in 2025 toward a near-term milestone in 2026 and beyond. This study translates that macro momentum into actionable choices for materials suppliers, OSATs, equipment vendors, and financial sponsors who must navigate cost volatility, regulatory shifts, and fast-moving technology adoption tied to advanced packaging formats.

Semiconductor Packaging Electroplating Solution Market

Proven forecasting framework: A transparent historical baseline (2020–2025) plus a scenario-capable projection (2026–2032) that isolates demand drivers, throughput assumptions, and sensitivity to raw material price swings.

Semiconductor Packaging Electroplating Solution Market

Commercial playbooks: Supplier scorecards, go-to-market stratagems for acid and alkaline chemistries, and partner-selection criteria tuned to OSAT and wafer-level packaging dynamics.

Semiconductor Packaging Electroplating Solution Market

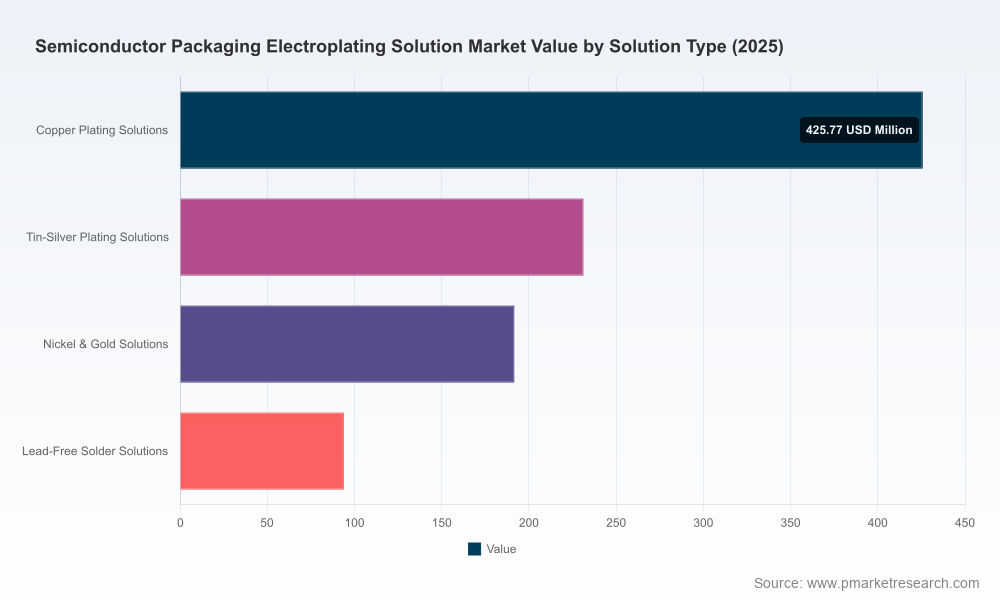

Technology roadmaps: Comparative assessment of copper, tin‑silver, nickel/gold and lead‑free solder electroplating processes, with guidance on where R&D should prioritize additive chemistry, bath stability, and defect reduction for nano-scale interconnects.

Operational models: Capex-to-throughput templates, cost-pass-through modeling for input price shocks (e.g., copper), and fab-to-OSAT transfer pricing examples to support procurement and contract negotiations.

Regulatory & supply resiliency playbook: Compliance checklists keyed to evolving export controls and supply-chain localization strategies for 2026 program planning.

M&A and partnership guidance: Valuation levers, integration risks, and a prioritized list of capability targets for inorganic growth or technology licensing.

Growth underpinned by advanced packaging adoption. Demand for electroplating solutions is being driven by wafer-level packaging, flip-chip interconnects and other advanced 2.5D/3D integration approaches. The market’s projected CAGR of 9.5% reflects both increasing unit volumes and a rising technical premium for high-purity, low-resistivity copper processes.

Raw material and cost pressure. Early-2026 copper price volatility has already fed through to supplier pricing and prompted cost-pass-through measures across the supply chain. Suppliers and buyers must adopt dynamic hedging and contractual mechanisms in 2026 to preserve margins while maintaining supply continuity.

Regulatory tightening. Refinements to export-control regimes and Foreign-Produced Direct Product rules are complicating cross-border supply of certain electroplating equipment and chemicals. Compliance risk now carries program-timing implications; companies should embed regulatory scenario planning into product roadmaps and supply contracts.

Localization and supply resilience. Major foundries and OSATs are accelerating local sourcing for critical additives and chemistries. 2026 will see further investment in regional production lines and qualification programs to reduce single-source exposure.

Technology substitution and cost competition. Domestic suppliers in several markets have achieved breakthroughs that materially reduce cost-per-bump for sub-5nm-capable copper chemistries. These advances create both competitive threats for incumbents and partnership opportunities for OEMs seeking price-competitive qualification paths.

Equipment-materials co-innovation. Recent industry activity — including new electroplating tool orders and dedicated electroplating tool families announced in late 2025 and early 2026, and supplier trade-show co-innovation initiatives — reinforces the need for synchronized tool-and-chemistry roadmaps to accelerate time-to-specification.

DuPont — Broad materials portfolio and deep integration into advanced packaging value chains. Strengths: comprehensive electroplating chemistries and an established qualification footprint. Strategic priority for 2026: defend high-end customer relationships through application engineering and bundled process solutions.

Element Solutions / MacDermid Enthone — Focused acid copper and semi-additive process expertise. Strengths: copper-pillar and RDL processes; play to watch: drive substrate-system partnerships and extend proprietary process steps to lock in design wins.

MKS/Atotech — Integrated electrolytic plating systems and wet-chemistry processes. Strengths: equipment-plus-chemistry integration. For 2026 they will emphasize turnkey solutions enabling faster customer qualification cycles.

Technic Inc. — High-speed plating chemistries tuned for coplanarity and low roughness. Tactical move: expand co-development agreements with OSATs targeting cycle-time reductions and yield improvement guarantees.

Umicore — Additive specialists for high-purity copper applications. Strategic edge: differentiated additive IP for micron-scale interconnects; 2026 action: pursue licensing and OEM bundling to scale adoption.

Uyemura and TANAKA Precious Metals — Niche leaders in high-aspect-ratio via filling and precious-metal processes respectively. Expect targeted collaborations with equipment OEMs and regional fabs to cement specialty process adoption.

Shanghai Sinyang, PhiChem and other domestic players — Rapidly climbing the learning curve on sub-5nm copper chemistries and cost-competitive manufacturing. Their emergence alters pricing dynamics and accelerates decisions around localization for many OSATs; incumbents must evaluate price vs. qualification-risk tradeoffs.

BASF — Diversified chemical capability with the potential to scale additive chemistry offerings for advanced packaging; watch for moves into bundled process solutions or alliances with equipment vendors.

For materials suppliers: prioritize dual-track development — protect premium product lines (high-purity, low-resistivity additives) while incubating cost-engineered alternatives for high-volume OSATs. Embed clear qualification roadmaps and commercial pilots into development plans.

For equipment OEMs and integrators: accelerate platform modularity so that a single tool family can accommodate multiple plating chemistries and panel/wafer formats. Offer integrated qualification services to lower customer adoption friction.

For OSATs and wafer fabs: adopt a segmented sourcing strategy — qualify a Tier-1 global supplier alongside vetted regional vendors to balance cost, resilience and compliance risk. Tighten contractual clauses around price pass-through and delivery SLAs to manage raw-material shocks.

For investors and M&A teams: prioritize targets with proprietary additive IP, demonstrated pilot-to-production transfer capability, and existing OEM partnerships. Valuation upside is strongest where technical differentiation shortens qualification timelines.

For policy and procurement teams: incorporate export-control scenario matrices into program timelines and invest in local qualification capacity for critical chemistries to reduce program schedule risk.

Macro-to-micro linkage: Our study connects a rigorous, audited market-sizing exercise (historical 2020–2025 and forecast 2026–2032) with supplier-level commercial realities so teams can translate top-line projections into procurement, R&D and capex plans.

Competitive crystallization: We combine supplier scorecards with recent industry intelligence — including tool deployments, product launches, and university-to-industry breakthroughs — to surface the practical implications of each development for your opportunity set in 2026.

Risk-forward scenarios: The report’s scenario suite lets decision-makers stress-test outcomes against copper price shocks, export-control permutations, and rapid domesticization of chemistry supply — all essential inputs for robust 2026 budgets and contracting strategies.

Concentration signal: The market exhibits meaningful supplier concentration at the top, creating both vulnerabilities (single-source risk, pricing pressure) and opportunities for challengers who can offer credible, lower-cost alternatives or differentiated technology.

PW Consulting’s Semiconductor Packaging Electroplating Solution Market report is intentionally crafted as a strategic bridge — enough detail to guide 2026 decisions and provoke immediate action, while reserving the granular segmentation tables, supplier benchmarking matrices, and downloadable financial models for the full study. For access to the complete dataset, supplier scorecards, and tailored advisory engagements that translate findings into a 90‑day implementation plan, please visit PW Consulting’s report page.

— PW Consulting, Strategic Advisory & Industry Analysis

For detailed analysis of this topic, please visit the official page:Semiconductor Packaging Electroplating Solution Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com