The Role of Shift Transitions in High-Risk Work Environments

Other |

2026-04-01 09:43:58

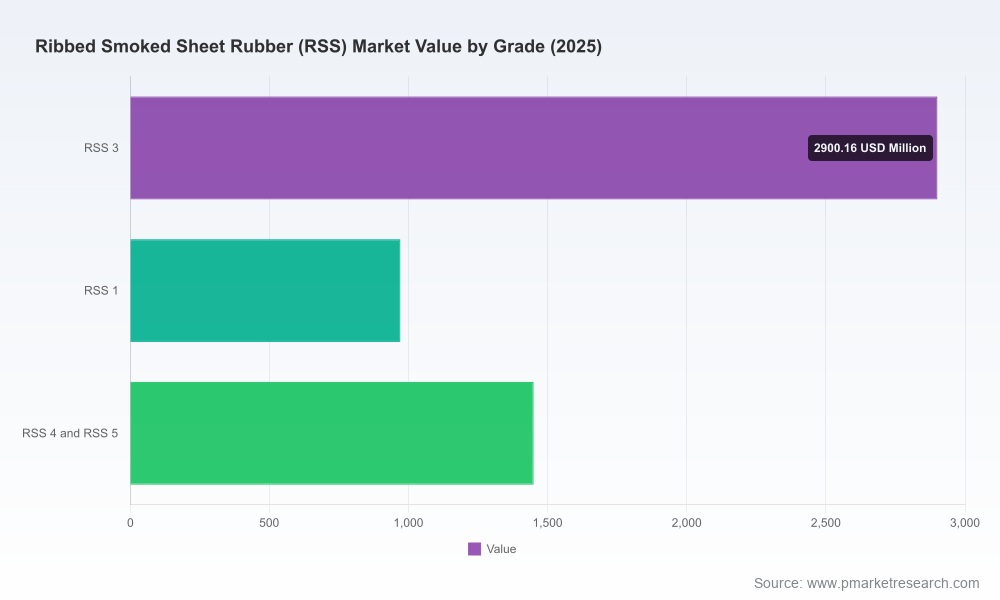

PW Consulting’s latest Ribbed Smoked Sheet Rubber (RSS) Market report — anchored on a 2025 base year and a 2026–2032 forecast window — delivers the market intelligence and decision frameworks executives need to set winning strategies in 2026. Our quantitative model shows the RSS market at USD 5,320.5 Million in 2025, progressing to USD 5,611.1 Million in 2026 and reaching USD 7,168.0 Million by 2032, reflecting a 4.35% compound annual growth rate over the forecast period. These headline metrics mask a complex interplay of supply shocks, regulatory re‑calibration and value‑chain consolidation that will determine winners and losers in the next 18–36 months.

Ribbed Smoked Sheet Rubber Rss Market

Transition from cost arbitrage to compliance arbitrage: From 2025 onward, regulatory enforcement (notably traceability and deforestation rules) is elevating the importance of provenance and documentation. Companies that move early to operationalize geolocation‑based traceability will avoid market access friction and capture premium channels.

Ribbed Smoked Sheet Rubber Rss Market

Demand resilience but margin pressure: Our topline forecasts show steady market expansion, yet input cost volatility—driven by raw latex dynamics and episodic crop disease—will compress margins for producers and converters that do not adopt active hedging and cost‑to‑serve optimisation.

Ribbed Smoked Sheet Rubber Rss Market

Consolidation opportunity window: Concentration metrics indicate a market where top producers hold a material share but fragmentation remains across many local mills. This creates M&A and JV opportunities for firms seeking scale, integration and control of quality‑critical grades.

Supply constraints and natural‑rubber dynamics: Industry sources reported global RSS production in 2024 at approximately 7.2 million tons, while overall natural rubber output fell and leaf disease impacted yields. The immediate implication for 2026 planning is a higher probability of tight short‑term availability for select grades and a need for more diversified sourcing strategies.

Input cost volatility: Natural rubber latex prices climbed materially into late 2024 — an average of roughly USD 1,720 per ton in Q4 — and benchmark grade price benchmarks experienced episodic spikes. Price pass‑through to downstream buyers will be asymmetric; producers with disciplined procurement and dynamic pricing models will preserve margins.

Regulatory acceleration: The EU Deforestation Regulation (EUDR) and revised national standards are moving traceability from “best practice” to a market access requirement. In parallel, import tariffs and trade measures in key markets can create near‑term channel dislocations that require agile commercial responses.

The market remains anchored by several established producers and regionally dominant processors. Leading players combine plantation access, integrated processing and export networks. Key themes emerging from our competitor analysis:

Sri Trang Agro-Industry — a global anchor supplier with substantial processing scale and recent progress on sustainability certification. Their ISCC certification deepens access to sustainability‑sensitive buyers and sets a higher bar for traceability expectations across the industry.

Regional integrated players — firms such as Von Bundit, Southland Rubber and Tongking Rubber Group pair plantation or contract‑farming control with in‑house smoking and grading capabilities. These players are well‑positioned to protect quality and mitigate raw material swings but must continue investing in compliance systems to defend export markets.

Vietnamese and Indian exporters — producers like Halo International, Phuoc Hoa and AVT Natural serve critical demand corridors for Europe, North America and neighbouring Asia. Their strategic choices on grade mix, certification and vertical integration will determine how much value they capture as premium channels expand.

Institutional frameworks — entities such as national rubber boards and licensed mill networks maintain soft governance and standardisation roles that influence market access and specification compliance. Their procedural updates and standard changes can create immediate commercial impacts for supply chains.

Our report is constructed as an operational playbook for decision makers. Highlights include:

Top‑down market sizing and a bottom‑up forecast (2026–2032) with scenario stress‑tests that isolate regulatory, price and supply‑shock outcomes.

Demand driver mapping across major end‑use clusters, and a granular analysis of margin pools by supply‑chain node.

Supply‑side diagnostics: plantation yield modelling, smoking capacity analysis, and a cost curve that ranks mills by delivered cost competitiveness under multiple raw‑material price scenarios.

Compliance and traceability playbook: step‑by‑step requirements to meet EUDR and equivalent regimes, including data templates, verification checkpoints and supplier audit protocols.

Commercial response toolkit: pricing frameworks, indexation clauses, hedging strategies, and inventory policies designed for a market with episodic shortages and policy shocks.

Competitive intelligence dossiers for the top regional and global players, with implications for partnerships, off‑take agreements and acquisition targets.

M&A and partnership screening matrices that prioritise targets by integration value (quality control, traceability, market access) rather than simple capacity metrics.

Practical annexes — contract clause templates, auditing checklists, and recommended KPIs for procurement, sustainability and compliance teams.

Prioritise traceability investments now. Firms that invest in geolocation mapping, mill‑level traceability and third‑party verification will avoid costly market exits and unlock buyers requiring compliant supply chains.

Redesign procurement into a two‑track model: (1) secured core supply through strategic partnerships or minority equity in mills; (2) flexible spot and short‑term contracts for tactical arbitrage. This reduces exposure to correlated crop risks and trade disruptions.

Adopt dynamic price pass‑through mechanisms. Indexation and flexible pricing terms tied to benchmark latex or RSS indices protect both suppliers and buyers while sustaining commercial relationships.

Evaluate targeted vertical integration selectively. Control of upstream processing or dedicated mills can be accretive where quality and traceability premiums are significant; however, integration must be justified by margin enhancement and market access certainty.

Push a sustainability premium strategy. Obtaining recognised sustainability certifications early can be monetised in tendered channels and reduces counterparty due‑diligence friction in EUDR‑sensitive markets.

Maintain liquidity for opportunistic consolidation. Given moderate market concentration (the top three and five producers capture material but not dominant shares), well‑timed acquisitions of reliable mills can fast‑track quality control and compliance capability.

Our scenario analysis highlights three near‑term outcomes that should shape boardroom contingency plans:

Regulatory tightening + certification premium: Accelerated enforcement raises compliance costs for non‑certified suppliers, creating a two‑tier market where certified product commands reliability premiums.

Supply shock (crop disease, weather) + trade restrictions: Simultaneous yield disruptions and tariff measures drive acute shortages for specific grades, prompting re‑routing and substitution decisions in tyre and industrial sectors.

Stable demand + price normalisation: If production recovers and prices stabilise, the market will reward scale players that combined quality, cost and compliance — while putting pressure on smaller mills with limited access to certification and export channels.

Our RSS market offering combines structured data, primary supplier interviews, and scenario modelling into decision‑ready outputs: strategy memos, M&A target shortlists, procurement playbooks, and custom analytics (including a downloadable KPI dashboard). For senior teams planning 2026 initiatives, we provide rapid workshops to translate the report’s findings into capital allocation, sourcing commitments and compliance roadmaps.

This brief highlights the strategic contours of the RSS market ahead of 2026. For the full data tables, grade‑level demand and supply splits, and executable country‑by‑country playbooks — including the segmented scenarios that underpin our forecast — please consult the full PW Consulting Ribbed Smoked Sheet (RSS) Market report or contact your PW Consulting analyst. The full report unlocks the granular segmentation, grade and regional breakouts necessary to operationalise the recommendations summarized here.

PW Consulting — Strategic clarity for a material‑intense, compliance-driven commodity market.

For detailed analysis of this topic, please visit the official page:Ribbed Smoked Sheet Rubber Rss Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com