PW Consulting Releases Strategic Brief: T Dodecyl Mercaptan (TDM) Market — What 2026 Decision‑Makers Need to Know

PW Consulting today publishes a forward‑looking industry brief accompanying our full T Dodecyl Mercaptan (TDM) market report. The brief synthesizes proprietary modeling, primary market intelligence and scenario analysis to guide procurement, commercial and investment decisions in 2026. It is designed as a “trailer” — demonstrating the analytical depth clients will find in the full report while intentionally withholding the underlying segment‑level tables and price curves that are accessible only through our full deliverable.

T Dodecyl Mercaptan Market

Snapshot — steady growth, concentrated supply

Our market model shows the global TDM market expanding from roughly USD 492 million in 2020 to approximately USD 585.5 million in 2025, reflecting steady demand across polymer and specialty chemical applications. Looking ahead over our forecast window (2026–2032), the market is projected to grow at a compound annual growth rate (CAGR) of 4.21%, reaching just over USD 780 million by 2032. This trajectory signals predictable, commercially meaningful expansion rather than speculative volatility — an important foundation for 2026 planning.

T Dodecyl Mercaptan Market

Supply concentration is a material strategic factor. The top three producers account for roughly two‑thirds of the market by volume, and the leading five suppliers collectively control an even larger share. That degree of concentration creates structural asymmetries favorable to incumbents but also produces discrete windows of opportunity for newcomers and downstream players pursuing differentiated grades or logistics advantages.

T Dodecyl Mercaptan Market

Why this matters for 2026 decisions

- Procurement strategy: With a concentrated supplier base and modest market expansion, 2026 is a pivotal year to renegotiate terms, secure multi‑year volumes or explore inventory‑optimization programs. Buyers who treat 2026 as a renewal inflection point can materially reduce supply risk and control cost exposure.

- Capex and expansion timing: Producers and financial sponsors weighing capacity investments should use 2026 to refine timing and scale. The market’s steady CAGR supports selective brownfield expansions or debottlenecking projects, but returns hinge on feedstock cost assumptions and regulatory compliance costs.

- Product strategy: Demand for specialty/high‑purity grades is growing in coatings, fine chemicals and select polymer streams. Firms that reposition portfolios toward higher‑margin, higher‑value grades — backed by quality controls and traceability — can capture outsized margin improvement.

- M&A and JV opportunities: High concentration and differentiated regional footprints make 2026 an advantageous time for acquirers seeking bolt‑on assets or access to specialty grades. Transaction structures that prioritize off‑take and technology transfer will attract the most attractive valuations.

Key market dynamics shaping 2026

- Feedstock and cost volatility: TDM production is rooted in the addition of hydrogen sulfide to propylene tetramer (dodecene), which links cost of goods to the aromatics and olefins complex. In Q3 2025 market signals showed upward pressure on propylene tetramer production costs driven by naphtha, propane and propylene price moves — a short‑to‑medium term earnings headwind that buyers and producers must model into commercialization and hedging strategies.

- Regulatory pressure and compliance costs: Tighter chemical safety and emissions standards under frameworks such as REACH in Europe and TSCA in the U.S. are increasing compliance obligations for sulfur‑containing intermediates. For producers, this raises operating costs (labeling, handling, emission controls) and creates product differentiation for firms that can certify lower emissions footprints or enhanced monitoring.

- Concentration and bargaining power: High market concentration enhances pricing resiliency for incumbents, but it also means that single‑site outages or strategic capacity changes can quickly ripple through regional supply dynamics. Buyers should prioritize multi‑sourcing strategies and tiered contingency plans.

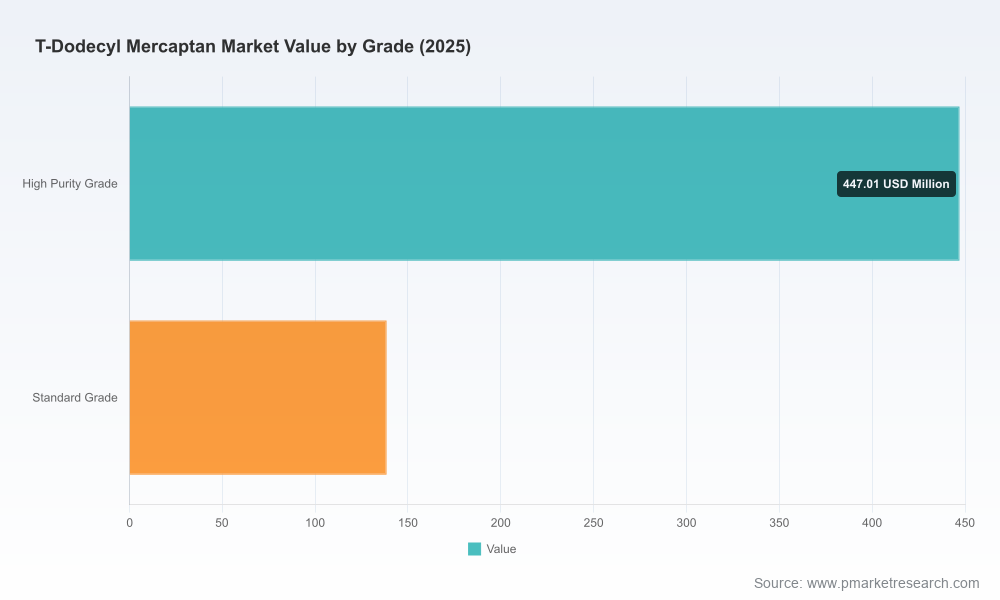

- Quality and grade segmentation: Growth in high‑value applications (e.g., coatings, specialty polymers and lubricant additives) continues to expand demand for high‑purity TDM. This trend rewards manufacturers with strict quality control and dedicated production lines for ultra‑high‑purity grades.

Competitive landscape — what the leading players signal

The market features a mix of large integrated chemical companies and specialized regional producers. Our assessment of core players yields the following strategic takeaways for 2026:

- Chevron Phillips Chemical Company (The Woodlands, Texas): A primary North American producer with established capacity and an industrial brand (Sulfole® 120). The company’s strength is scale and integrated feedstock access — an advantage for buyers seeking volume security in the Americas. For competitors, Chevron Phillips’ position underscores the importance of regional differentiation and service models.

- Arkema S.A. (Colombes, France): Positions TDM within a broader thiochemicals portfolio and serves both polymer and mineral processing applications. Arkema’s capability to cross‑sell into adjacent industrial channels highlights the commercial value of portfolio adjacency when pursuing margin uplift in 2026.

- ISU Chemical Co., Ltd. (Ulsan, South Korea): A specialist in high‑purity TDM with rigorous quality controls — and with a recent plant expansion announced in May 2025 to raise capacity for polymer and specialty chemical demand. ISU’s moves illustrate a viable growth playbook: invest selectively in capacity for premium grades and capture higher profitability while managing compliance rigor.

- Sanshin Chemical (Japan): Focuses on ultra‑high‑purity grades for polymer emulsions and fine chemicals. This niche specialization demonstrates how technical differentiation can create defensible positions against larger commodity producers.

- Palica Chem: A focused supplier with detailed logistics and packaging solutions (e.g., drum and ISO tank offerings) supporting emulsion polymerization customers. Palica exemplifies that operational excellence in handling and logistics is a competitive lever that can win contracts even in a concentrated supplier environment.

What our full report delivers (practical tools for action)

The full PW Consulting TDM market report is structured to support executable decisions in 2026. Key deliverables include:

- Proprietary market model (historical 2020–2025 and forecast 2026–2032) with scenario toggles for feedstock price, regulatory cost and demand elasticity.

- Supply‑demand balance and tightness view by grade tier, including inventory cycle analysis and outage sensitivity scenarios.

- Price forecasting toolkit and supplier risk heat‑map to inform contract negotiations and hedging strategies.

- Buyer playbook: negotiation templates, service‑level KPIs, and recommended contractual clauses for multi‑year off‑takes.

- Producer playbook: CAPEX prioritization framework, ROI calculator under alternative price paths and quality‑grade investment case studies.

- Regulatory compliance checklist and impact assessment for REACH/TSCA updates, emissions control CAPEX and labeling requirements.

- Supplier scorecards and M&A screening matrix that factor in technical capability, geographic footprint and integration synergies.

- Primary research appendices — interviews, plant announcements (including recent capacity moves in 2025), and raw material pricing histories used in our modeling.

Strategic recommendations for 2026

- Buyers: Lock in supply through layered contracting (mix of spot, short‑term and one strategic multi‑year agreement), and build logistical redundancies for regions where supplier concentration is highest. Include price‑adjustment mechanisms tied to a transparent feedstock index to share risk.

- Producers: Target incremental investments in high‑purity and specialty lines rather than large commodity expansions unless feedstock access and long‑term off‑take are secured. Invest in compliance and emissions monitoring now to sidestep retrofitting costs later.

- Investors/M&A: Prioritize assets with high‑purity credentials, secure feedstock linkages or unique logistics channels. Small bolt‑ons that add grade differentiation or last‑mile supply advantages will likely out‑perform undifferentiated scale plays.

- Policy and risk teams: Rebase cost and scenario planning to reflect regulatory tightening under REACH/TSCA and the observed Q3 2025 feedstock price pressures. Develop contingency playbooks for single‑site disruptions among the largest suppliers.

Conclusion — why PW Consulting’s intelligence matters in 2026

For decision‑makers approaching 2026 procurement cycles, capital allocation reviews and M&A screens, TDM is no longer a back‑office commodity: it is a strategically important intermediate whose price, availability and purity profile can determine margin outcomes across polymers, lubricants and specialty chemicals. Our analysis combines granular market sizing, supplier profiling and scenario modeling to convert macro trends into executable commercial actions.

This brief illustrates the analytical rigor of PW Consulting’s full TDM market report and the hands‑on tools it contains. To access the complete dataset, proprietary segment tables, price curves and the interactive model required to run your own scenarios, please visit the full report page or contact PW Consulting’s industrial chemicals practice.

For detailed analysis of this topic, please visit the official page:T Dodecyl Mercaptan Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com