10B Enriched Potassium Fluoroborate Market: Strategic Imperatives for 2026 — PW Consulting

PW Consulting’s 10B Enriched Potassium Fluoroborate Market study frames a near-term inflection for buyers, producers and investors preparing decisions in 2026. After robust recovery from 2020, the market expanded materially through 2025 and — under our base case — continues to scale across 2026–2032 at a compound annual growth rate (CAGR) of 6.41%. By integrating supplier-capacity signals, isotope-enrichment dynamics and end‑use demand matrices, the report delivers the practical analysis executives need to convert market momentum into defensible strategy while safeguarding operational continuity.

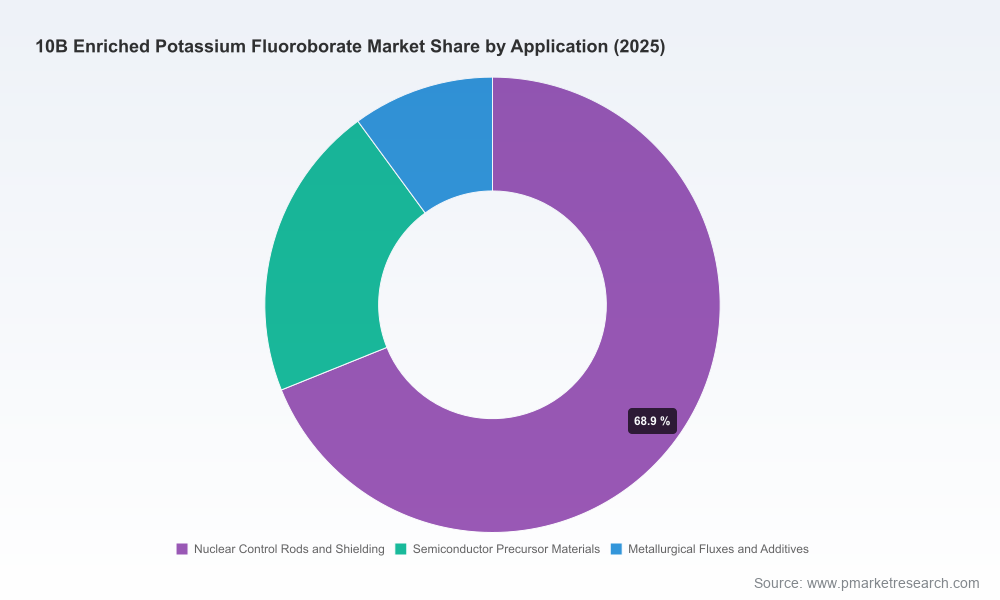

10B Enriched Potassium Fluoroborate Market

High-level market trajectory (what the top-line numbers tell you)

The market has moved from a modest base in the early 2020s into a clear growth phase by 2025. Our model — calibrated to multiple years of shipment, production and commercial disclosures — shows continuous expansion through the 2026–2032 forecast window. That pace of expansion, when viewed alongside concentrated supply structures and the technical specificity of enriched boron chemistry, transforms what might otherwise be a commodity sourcing decision into a strategic priority for nuclear operators, specialty chemical buyers and capital allocators.

10B Enriched Potassium Fluoroborate Market

Why 2026 is a pivotal decision year

- Structural demand: Ongoing life‑extension and decommissioning activity in nuclear fleets, combined with persistent needs for spent fuel pool management and neutron‑control materials, underpin predictable baseline demand.

- Technical scarcity: Boron‑10’s high thermal neutron absorption (thermal cross section ~3,800 barns) makes enriched K10BF4 uniquely effective for several nuclear applications — limiting viable substitutes in many use cases.

- Supply concentration: Market concentration metrics indicate a tightly clustered supplier set, which raises counterparty risk for large-volume buyers and increases the value of validated second-source pathways.

- Supplier capability asymmetry: Leading processors and technology holders report commercially proven enrichment processes and validated high-purity (>95% and higher) product lines, creating meaningful barriers to rapid new entrant scaling.

- Regulatory and logistics complexity: Licensing, transport security and qualification cycles for nuclear‑grade materials lengthen the lead time for changes to sourcing strategies — decisions taken in 2026 will affect operations for years.

What PW Consulting’s report delivers (practical outputs)

The study is designed as a decision‑ready tool for corporate strategy, procurement, investor diligence and M&A teams. Among the actionable deliverables:

10B Enriched Potassium Fluoroborate Market

- Supply‑demand model calibrated to historical shipments and supplier disclosures, with scenario toggles for slower/faster nuclear activity and regional policy shocks.

- Price and availability scenarios across 2026–2032, with sensitivity bands driven by feedstock, enrichment throughput and logistics stress tests.

- Supplier scorecards and vendor due‑diligence templates (technical capability, capacity, regulatory footprint, security posture and commercial terms).

- Procurement playbook: contracting templates, multi‑year volume strategies, hedging and inventory optimization guidance tuned to isotope‑handling realities.

- Manufacturing scale‑up checklists and technology gap analysis for downstream users contemplating vertical integration or joint manufacturing ventures.

- Regulatory risk matrix and stakeholder engagement pathways for jurisdictions with evolving nuclear or export-control regimes.

- M&A and investment screening frameworks, including valuation sensitivities for enrichment technologies and production assets.

Competitive landscape — what you need to know about incumbent players

The competitive set is defined by a mix of technology ownership, manufacturing scale and regional channel strength. Our report profiles the leading commercial actors, synthesizing public disclosures and commercial signals into implications for counterparty risk and partnership value.

- Technology-owners and processors: Firms with proprietary isotope enrichment know‑how and demonstrated high‑purity production lines occupy preferred positions in the qualification steps required by nuclear and defense buyers. These organizations typically command premium pricing and longer contract lead times due to qualification costs.

- Mass producers with strategic capacity: Suppliers that have converted enrichment capability into repeatable, mass‑production flows are positioned to meet bulk needs for spent fuel pool and shielding applications. Reported commercial capacity footprints should be treated as floor capacity for planning, not as unconstrained supply.

- Regional distributors and channel partners: Distribution agreements and regional stocking arrangements affect procurement cadence, regulatory support and the total cost of ownership for buyers — especially where local qualification and traceability are required.

Company notes (directional, for screening purposes)

- Some established processors offer commercial products at enrichment levels commonly used in nuclear applications and possess proprietary routes that can achieve ultra‑high enrichment — this supports both product reliability and the potential for premium product lines targeted at high‑spec applications.

- At least one manufacturer publicly cites mass production capability for enriched boron products and confirms ongoing commercial availability for nuclear applications; such disclosures reduce supply uncertainty but do not eliminate qualification lead times for new buyers.

- Regional distributors play a meaningful role in product placement across East Asian markets, and their channel agreements materially affect speed to market for end users in those geographies.

Strategic playbook for corporate decision-makers in 2026

Executives who treat enriched potassium fluoroborate as a tactical commodity risk missing value and resilience opportunities. Our recommended five‑point playbook:

- Prioritize validated second sources: Develop and qualify at least one alternate supplier to reduce single‑point-of-failure exposure. Qualification timelines should be modeled at 12–24 months depending on application criticality.

- Negotiate structured off‑take agreements: Use stepped volume commitments, option tranches and shared inventory facilities to balance cost efficiency and supply security.

- Explore partnership or minority‑stake arrangements: Where strategic concentration is high, an equity or revenue‑sharing approach with a capacity‑holder can secure access and align incentives for capacity expansion.

- Invest in operational readiness: Strengthen inbound logistics, chain‑of‑custody controls, and in‑house QA to accelerate supplier qualification and reduce acceptance failure rates.

- Run a substitution & R&D hedging program: For non‑mission‑critical applications, accelerate R&D into lower‑enrichment or alternate chemistries to reduce absolute exposure over a multi‑year horizon.

Risks to track and immediate mitigations

- Geopolitical/export controls: Monitor export licensing regimes and trade restrictions that could reduce cross‑border shipments — maintain a mapped universe of supply jurisdictions and contingency logistics routes.

- Enrichment throughput limits: Treat announced capacity as subject to ramp risk; validate vendor ramp plans through technical audits and independent verification.

- Concentration-driven price shocks: Given the market’s concentrated supplier structure, identify hedges and contractual protections to mitigate sudden price jumps.

- Qualification delays: Build realistic timelines for nuclear‑grade qualification into project plans; use staged acceptance criteria to limit project slippage.

Investor and M&A implications

For financial sponsors and strategic buyers, enriched boron assets combine technical defensibility with concentrated supplier economics. The market’s profile supports a premium for assets that provide: (1) demonstrable enrichment capability beyond commodity grades; (2) validated production processes with nuclear‑grade quality systems; and (3) secure feedstock and logistics arrangements. Our investment diligence checklist focuses on technological obsolescence risk, regulatory exposure, customer concentration and the true scalability of declared production capability.

Concluding perspective — why PW Consulting’s report matters for 2026

Decisions made in 2026 about supply contracts, capital allocation and strategic partnerships will reverberate through the 2026–2032 growth window. The combination of steady market expansion (CAGR of 6.41% in our forecast), technical demand characteristics and a concentrated supplier base converts a seemingly narrow materials market into a strategic lever for operational resilience and competitive advantage.

PW Consulting’s full 10B Enriched Potassium Fluoroborate Market report contains the complete, transaction‑ready dataset (regional and application splits, supplier share tables, price curves and downloadable financial models) plus vendor scorecards and playbooks referenced above. To obtain the report, vendor diligence templates or a tailored briefing for your executive team, contact PW Consulting or visit our report page for licensing and access details.

For detailed analysis of this topic, please visit the official page:10B Enriched Potassium Fluoroborate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com