PW Consulting: Battery Nonwoven Diaphragm Market Set to Expand at a Robust 8.5% CAGR, New Report Reveals

Other |

2026-07-07 07:28:29

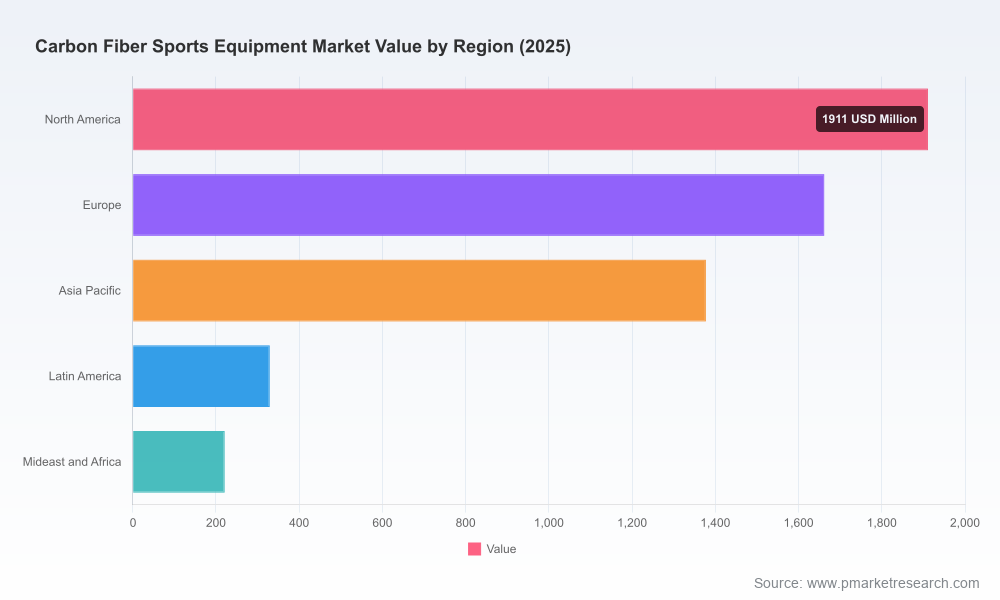

As brands, suppliers and investors prepare strategic plans for 2026, the carbon fiber sports equipment market presents a distinctive blend of steady growth, technology-led differentiation and supply-chain complexity. PW Consulting’s latest market research shows that the global market expanded from approximately USD 4,014.35 Million in 2020 to about USD 5,500 Million in 2025, and is projected to approach USD 8,546.92 Million by 2032 — reflecting a compound annual growth rate of 6.5% across the 2026–2032 forecast period. This briefing explains why that trajectory matters to corporate decision-makers and how our report translates these macro dynamics into executable strategy while intentionally withholding detailed segment-level figures to preserve the full report’s exclusivity.

Carbon Fiber Sports Equipment Market

Transition from product performance to value capture: With carbon fiber already established as the material of choice for high-performance rackets, clubs, bikes and skis, the next wave of competitive advantage will come from controlling value beyond raw material — namely design integration, digital-enabled customization and lifecycle services.

Carbon Fiber Sports Equipment Market

Margin pressure driven by upstream dynamics: Pricing and availability of key precursors and prepregs remain a determinative factor for finished-goods economics. Companies that proactively insulate their cost base through strategic sourcing, vertical integration or long-term off-take agreements will enjoy outsized returns.

Carbon Fiber Sports Equipment Market

Regulatory and circularity inflection: Increasing emphasis on recycling and end-of-life management is creating both compliance obligations and new commercial opportunities (repair, certified remanufacture, take-back programs). Leaders will integrate circular strategies into product roadmaps and commercial propositions.

Proprietary market model and scenarios — top-line trajectory, sensitivity tests and upside/downside cases calibrated to macroeconomic and raw material shocks.

Supply-chain heatmap — visibility on precursor suppliers, composite converters and high-volume OEM partners, including bottleneck risk scoring and mitigation playbooks.

Technology and materials roadmap — assessment of standard vs. advanced modulus fibers, hybrid solutions, prepreg innovations and recycling technologies, with time-to-commercialization estimates.

Commercial playbooks — go-to-market options for premium and mass segments, pricing levers, customization and subscription-style offerings for high-value users.

M&A and partnership matrix — prioritized targets and alliance archetypes designed to accelerate capability acquisition (manufacturing scale, digital integration, circularity) with an execution checklist for 100/200/500-day horizons.

Regulatory & sustainability impact analysis — scenario planning for extended producer responsibility, carbon disclosures and certification frameworks, plus recommended compliance roadmaps.

Operational levers — CAPEX vs. outsourcing trade-offs, NPI (new product introduction) sequencing, and quality-control templates tailored to composite fabrication.

The market remains neither a pure oligopoly nor fully fragmented: concentration metrics indicate meaningful scale among leading material suppliers and a broader set of specialized OEMs. Strategic positioning in 2026 will hinge on three formulae — control of advanced feedstock, capability in composite engineering, and brand-to-technology integration.

Toray Industries (Tokyo) — Toray’s leadership in carbon fiber and composite systems continues to be a strategic anchor for high-performance OEMs. Their focus on material science and recent recognition for bio-circular prepreg applications signals a dual push: preserve technological leadership while addressing lifecycle credentials.

Teijin Limited (Tokyo) — Teijin’s emphasis on recyclable and high-performance fibers positions it as a preferred partner for OEMs that must reconcile performance with sustainability standards. Expect more co-development projects with equipment makers focused on certified materials.

Mitsubishi Chemical (Tokyo) — Strong in prepregs and composite integration, Mitsubishi’s playbook targets premium OEMs seeking consistent quality at scale. Their advantage is in systems-level supply rather than commodity fiber sales.

Hexcel Corporation (USA) — Hexcel’s aerospace pedigree enables transfer of advanced composite technologies into the sports sector, accelerating the adoption of aerospace-grade materials in elite product lines.

HEAD Sports (Austria) — As an OEM innovator, HEAD’s continual product refreshes and adoption of boron-infused carbon technologies demonstrate how equipment brands can extract performance differentials and command premium pricing.

Wilson Sporting Goods (USA) — Wilson leverages brand equity and composite engineering to lead in racquet sports; their challenge is converting performance heritage into new revenue streams (customization, direct-to-consumer services).

Giant Manufacturing (Taiwan) — Vertical integration in carbon weaving and frame manufacture is Giant’s competitive moat, enabling faster NPI cycles and margin control in cycles where volume matters.

Babolat (France) — Niche specialization in racquets with proprietary composite configurations gives Babolat high perceived performance; growth strategies will lean on digital coaching ecosystems and product personalization.

Trek Bicycle Corporation (USA) — Trek’s engineering-first approach and premium positioning make it a bellwether for carbon-fiber adoption curves in bicycles, especially as sport-tracking electronics integrate more tightly with frame designs.

SGL Carbon (Germany) — As a materials supplier with sports applications in their portfolio, SGL is positioned to capture modular opportunities where specialty composites meet sport-specific geometry and damping requirements.

Recent industry moves underscore the dual focus on material innovation and product differentiation: HEAD’s early-2026 racket refresh using boron-carbon constructs demonstrates performance-driven product cadence, and Toray’s recognition for bio-circular prepreg applications highlights sustainability credentials moving from concept to validated use cases. Collaboration between bike OEMs and smart-technology firms shows the market’s appetite for value-added integration beyond raw composites.

Precursor supply and converter capacity are the primary levers for near-term availability and cost. Firms that build strategic supply agreements or secure converting capability will reduce exposure to sudden price swings.

Recycling and reuse initiatives are accelerating; early pilots and consortium work are forming the basis for commercial circularity services. Companies that pilot take-back and certified remanufacture now will enjoy first-mover benefits in certification and customer trust.

Investor interest will cluster around three asset types: upstream precursor and tow capacity to secure feedstock; midstream conversion and prepreg capabilities to capture margin; and downstream OEMs with strong brand or digital ecosystems. Our M&A matrix ranks targets by synergy potential, integration difficulty and near-term cash flow uplift — a practical tool for deal teams and corporate development executives planning 2026 transactions.

Focus on capability buys, not just market share: prioritize acquisitions and partnerships that add composite engineering, digital customization or circular-processing capabilities.

Adopt a two-speed product strategy: maintain a premium, innovation-led line while rolling out cost-engineered versions for broader recreational markets, each with distinct distribution and warranty models.

Embed circularity into product economics: introduce certified take-back pilots tied to loyalty programs, and use recycled-content claims to defend margin in sustainability-conscious channels.

Hedge precursor exposure: develop multi-supplier contracts and evaluate in-house conversion where scale justifies CAPEX to stabilize gross margins.

Invest in data-enabled differentiation: pairing composite design with sensor telemetry and analytics can create recurring revenue through services (e.g., performance analytics, repair alerts).

Our full Carbon Fiber Sports Equipment Market report provides the models, templates and market-access playbooks companies need to operationalize the strategic choices above. It includes customizable financial models, supplier heatmaps, due-diligence checklists and a prioritized M&A shortlist tailored to differing risk appetites. To preserve the strategic value of that proprietary work we have intentionally withheld detailed segment-level splits in this brief — those granular tables and scenario files are available in the full report.

For executive teams: request a tailored 90-minute briefing to map the report’s findings onto your 2026 strategic plan.

For investors and corporate development: access the M&A matrix and valuation comparables in the full dataset to accelerate target screening.

For product and R&D leaders: use the technology roadmap and supplier heatmap to prioritize development sprints and pilot partners for circular solutions.

To review the complete data, segmented forecasts and the decision-ready annexes that underpin these conclusions, please visit the PW Consulting report page. The full report contains the granular market breakdowns, supplier lists and scenario spreadsheets that corporate teams and deal-makers will need to act confidently in 2026.

For detailed analysis of this topic, please visit the official page:Carbon Fiber Sports Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com